|

Financial

Management MGT201

VU

Lesson

11

SOME

SPECIAL AREAS OF CAPITAL

BUDGETING

Learning

Objectives:

In

this lecture, we will

discuss some special areas of

capital budgeting in which the

calculation

of

NPV & IRR is a bit more

difficult. These concepts

will be explained to you

with help of

numerical

example.

As

it is mentioned in the previous lectures

that we are studying the

area of capital budgeting

as

it

relates to projects, which means

investments in real assets (land,

property etc.) The major

difficulty in

the

NPV calculation is your

ability to forecast the cash

flows. Therefore, it is necessary

that one should

spent

time on this so that the

cash flow forecast is

accurate.

We,

have a simple formula to calculate the

cash flows. The way we

define the net

Incremental

after

tax cash flows for the

purposes of this course

is

Net

After-tax Cash Flows = Net

Operating Income + Depreciation +

Tax Savings from Depreciation

+

Net

Working Capital required for

this project + Other Cash

Flows

The

things we left out from the

formula given above are

certain incidental cash

flows (Include

Opportunity

Costs and Externalities but

Exclude Sunken Costs.)

Two

Major Criteria of Capital

Budgeting:

1.

Net Present Value

(NPV)

2.

Internal Rate of Return

(IRR)

a.

Combined View: NPV Profile

(NPV vs i Graph)

The

NPV is the most important

because it has a direct link

with shareholders wealth

maximization.

Let

us discuss in detail about the

difficulties faced in NPV & IRR

with the help of

certain

numerical

examples and explanations.

First,

we would discuss the case of

Multiple IRRs.

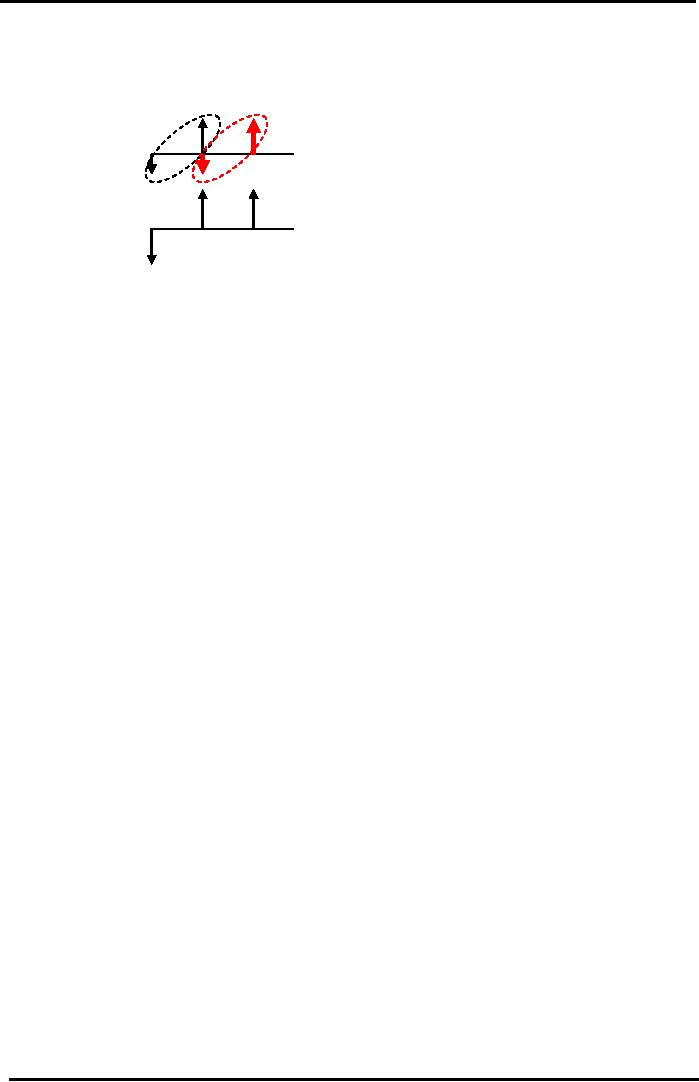

Multiple

IRR:

In

this case, you have a

project with certain cash

flows that are not

normal and when

you

try to calculate IRR you

obtain more than one IRR answer.

This is the case where you have

more

than

one sign change taking place

in your cash flow diagram.

Sign change means that

you have two

adjacent

arrows one of them is downward pointing & the

other one is upward pointing. In general,

our

cash

flow diagram starts with

down ward pointing arrow

(Investment) and it is followed

with series of

upward

pointing arrows (net incoming

cash) during the life of

project. However, during the

life of

project

if you have any net cash

outflow or downward pointing

arrow then that would be

second sign

change

and you can expect to have multiple

answer for IRR.

In

this particular case,

calculating the NPV and

setting it equal to zero to calculate

IRR will give

you

two answers & both of them

would be wrong.

The

alternative is to use Modified

IRR or MIRR approach.

MIRR

Approach:

The

logic behind MIRR is that

instead of looking at net cash flows

you look at cash inflows

and

outflows

separately for each point in

time. Discount all the

Outflows during the life to the

present and

Compound

all the Inflows to the termination date.

Assume reinvestment at a Cost of

Capital or Discount

Factor

(or Required Return) such as

the risk free interest rate.

The

MIRR represents the discount rate,

which will equate the Future

Value of cash inflows

to

Present

Value of cash

outflows.

Formula:

(1+MIRR)

n

=

CF

in *

(1+k) n-t

CF

out

/(1+k)

t

Modified

Internal Rate of Return

(MIRR) would provide us with

an answer, which is entirely

different

from

our previous IRR

calculations

Example:

A

project with the following

cash flows: Initial

Investment = -Rs100, Year 1 = +Rs500,

Year 2 = -

Rs500

If

we use standard NPV equation

to calculate the IRR

IRR

Equation: NPV = 0 = -100 +

500/ (1+IRR) - 500/ (1+IRR)

2

You

would come up with 2

answers

55

Financial

Management MGT201

VU

IRR

= 38% and 260%

Both

of these answers are

incorrect. Therefore, we will

use the modified IRR approach to

calculate the

actual

IRR for this

project.

MIRR

Approach (Assume Cost of Capital k =

10%):

(1+MIRR)

n

=

CF

in *

(1+k) n-t

CF

out

/

(1+k)

t

We

use 1.1 as compound factor

because we assume "i"=10% =

Risk free rate return.

Here`t' refers to

the

time in which a particular

cash flow occurs, while

`n' is the total life span

of the project.

(1+MIRR)

2

= 500

* (1+0.1)2-1

(100

/ 1.1) + (500 /

(1+0.1)2

(1+MIRR)

2

= 550

/ 513 = 1.07

MIRR

= 0.0344 = 3.44%

This

answer is entirely different

from the previous answers

that we got from calculating

the IRR.

However,

MIRR gives you the best

possible answer and the most realistic

too.

Now,

let us talk about the case

of comparing projects with different

lives.

NPV

of Projects with Different

Lives:

Suppose

that you have two projects

having different life spans.

It is not entirely accurate

to

calculate

NPV's in simple manner and

to compare them and pick the project

with higher NPV.

Because

you

are comparing a certain

project that is generating

cash flows for a short

period of time with

another

project

that is yielding cash flows

over a longer time. We use

following two approaches to

rank these

kinds

of projects.

1.

Common

Life Approach:

In

this approach, the idea is quite

simple. You need to bring

all the projects to the

same

length

in time. In other words, you

are required to convert all

the projects to the identical life

span.

You can do that by finding

least common multiple for common

life. For example, if

you

are

comparing two projects one

has life of 4 years and the

other, which has a life of 5

years, the

least

common multiple is 20 years. Sketch out

the cash flow diagram and

repeat the cash flow

for

each of the project such

that they fit in exact number of

time in 20 years. In case of

project

with

a life of 4 years, you can

replicate the cash flows 5 times in a

period of 20 years. . In

case

of

project with a life of 5

years, you can replicate the

cash flows 4 times in a period of 20

years.

Compute

the NPV of each project over

the common life and choose the

project with the highest

NPV.

2.

Equivalent

Annual ANNUITY (EAA)

Approach:

In

this case, our logic is to

find out that for a

particular project of limited

life giving you

the

certain net present value calculated in a

simple way, what kind of

yearly annuity gives the

same

NPV.

You can then compare annual

annuity of each project and

choose the highest. You are

comparing

cash

flow of two projects both of

which are taking place in a

period of one year only. You

can also

convert

the cash flows of the project to the

perpetuity, which is infinite,

and then you can compare

the

NPV's

like of different projects. That is

also correct since life

spans are identically

infinite.

Example:

We

have 2 Projects with following

Cash Flows:

Project

A: Io= - Rs100, Yr 1 =

+Rs200

Project

B: Io= - Rs200, Yr1= +Rs200,

Yr2= +Rs200

Simple

NPV Computation (assuming

i=10%):

NPV

Project A = -100 + 200/1.1 =

+Rs 82

NPV

Project B = -200 + 200/1.1 +

200/ (1.1)2

= +Rs

147

Conclusion

from Simple (or Normal)

NPV Calculation is that

Project B is better. It is incorrect

because

here

we are comparing apples to the

oranges since the project

lives are different!

Common

Life Approach:

Common

Life Span=Least common multiple = 2

Years (because this is the

shortest cycle in which

both

project

lives can exactly be

replicated back to back).

56

Financial

Management MGT201

VU

Project

A:

+200

+200

Yr

0

Yr

1

Yr

2

-100

-100

+200

+200

Project

B:

Yr

0

Yr

1

Yr

2

-200

In

this Cash Flow Pattern of A is

repeated exactly 2 times to cover the

life of the longer

Project

B.

The project A's outflow

100 & inflow of 200 then

we replicate it with down

ward pointing arrow

with

100 and upward pointing

arrow with 200 amount in the

2nd year. Project B remains

unchanged

Common

Life (C.L.)

NPV's:

Project

A C.L. NPV = -100 +

[(200-100)/1.1] + 200/

(1.1)2

= +Rs

156

Project

B C.L. NPV = Same as before

= +Rs 147

Now

our conclusion has changed!

After doing the Common Life

NPV, Project A looks better.

The

Simple

NPV of Project A was + Rs 82

but after increasing its

life to match Project B's,

the NPV of

Project

A increased. It is the correct answer. Also,

note that how the NPV of A

increased from 82 to

156

(almost

double) because you double

the life of the project.

Now

we solve this problem with

Equivalent Annual Annuity

Approach

Equivalent

Annual Annuity

Approach:

In

this we are explaining that

how we can achieve same NPV

value from an annuity

stream.

Here,

we are doing a back calculation

that we knew the NPV's but

which annuity stream they

are

representing

with in the life span of the

project. Then we compare the

annual annuity of both

projects.

The

life span remains

same

Example:

Start

with the Simple (or Normal)

NPV's calculated earlier (at i =

10%):

Project A Simple NPV = + Rs

82

Project B Simple NPV = + Rs

147

To

find EAA

Multiply

the Simple NPV of each

project by the EAA Factor

EAA

FACTOR = (1+

i) n

/

[(1+i) n

-1] where n =

life of project & i=discount

rate

Project

A's EAA Factor = 1.1 / (1.1-1) =

11

Project

B's EAA Factor = 1.12

/

(1.12-1) =

5.76

EAA

for each project

Project

A's EAA = Simple NPV * EAA Factor =

82*11= + Rs 902

Project

B's EAA = 147*5.76 = + Rs

847

Conclusion:

Project

A is better. Same conclusion as Common

Life Approach but of course

the

numbers

for EAA and NPV are

different.

Practical

view:

Companies

and individuals running different types

of businesses have to make the choice of the

asset

according

to the life span of the project.

For instance, a tailor shop

owner would have to decide

whether

to

invest in a sewing machine that

has a useful life of ten

years or to invest in another machine

with a

57

Financial

Management MGT201

VU

useful

life of three years. These decisions

are important since they

involve major cash outflows

of the

business.

There are advantages &

disadvantages associated with

different life span.

Different

Lives & Budget

Constraint:

Companies

and individuals running different types

of businesses have to make the choice of

the

asset

according to the life span of the

project.

Advantages

of asset with a long

life:

The

advantage of a longer asset life is

that the cash flows from the

project become more

predictable,

since there are lesser cash

outflows occurring during the

life of the project.

Disadvantage

of asset with very long

life:

It

does not give you the

opportunity (or option) to

extract full value of asset

and replace the

equipment

quickly in order to keep pace

with technology, better

quality, and lower

costs.

Advantages

of asset with short life

The

advantage of a short life asset is that

the investor, by making reinvestment in

the asset of a

superior

quality, lowers down the

costs and updates the project to the

new technological requirements.

Disadvantage

of assets with very short

life:

The

disadvantage is that the money will have

to be reinvested in some other project

with an

uncertain

NPV and return so it is risky. If a

good project is not

available, the money will

earn only a

minimal

return at the risk free interest

rate.

While

exercising the option of different

project timing, the projects can be

compared by applying

Common

Life and EAA Techniques to

quantitatively.

Budget

Constraint

We

have been addressing the issue of

capital budgeting with very

idealistic assumptions. In

practical

life, individuals and companies have a

limited amount of money and

limited human resources

in

terms of either skill or

numbers. It can be argued that the

firm can also meet

their requirements by

borrowing.

IN real life, managers may

avoid borrowing to limit

their risk exposure. This prevents

them

from

undertaking projects with high

positive NPVs that would

have added to the firm's value

and

maximized

shareholder wealth!

58

Table of Contents:

- INTRODUCTION TO FINANCIAL MANAGEMENT:Corporate Financing & Capital Structure,

- OBJECTIVES OF FINANCIAL MANAGEMENT, FINANCIAL ASSETS AND FINANCIAL MARKETS:Real Assets, Bond

- ANALYSIS OF FINANCIAL STATEMENTS:Basic Financial Statements, Profit & Loss account or Income Statement

- TIME VALUE OF MONEY:Discounting & Net Present Value (NPV), Interest Theory

- FINANCIAL FORECASTING AND FINANCIAL PLANNING:Planning Documents, Drawback of Percent of Sales Method

- PRESENT VALUE AND DISCOUNTING:Interest Rates for Discounting Calculations

- DISCOUNTING CASH FLOW ANALYSIS, ANNUITIES AND PERPETUITIES:Multiple Compounding

- CAPITAL BUDGETING AND CAPITAL BUDGETING TECHNIQUES:Techniques of capital budgeting, Pay back period

- NET PRESENT VALUE (NPV) AND INTERNAL RATE OF RETURN (IRR):RANKING TWO DIFFERENT INVESTMENTS

- PROJECT CASH FLOWS, PROJECT TIMING, COMPARING PROJECTS, AND MODIFIED INTERNAL RATE OF RETURN (MIRR)

- SOME SPECIAL AREAS OF CAPITAL BUDGETING:SOME SPECIAL AREAS OF CAPITAL BUDGETING, SOME SPECIAL AREAS OF CAPITAL BUDGETING

- CAPITAL RATIONING AND INTERPRETATION OF IRR AND NPV WITH LIMITED CAPITAL.:Types of Problems in Capital Rationing

- BONDS AND CLASSIFICATION OF BONDS:Textile Weaving Factory Case Study, Characteristics of bonds, Convertible Bonds

- BONDS VALUATION:Long Bond - Risk Theory, Bond Portfolio Theory, Interest Rate Tradeoff

- BONDS VALUATION AND YIELD ON BONDS:Present Value formula for the bond

- INTRODUCTION TO STOCKS AND STOCK VALUATION:Share Concept, Finite Investment

- COMMON STOCK PRICING AND DIVIDEND GROWTH MODELS:Preferred Stock, Perpetual Investment

- COMMON STOCKS RATE OF RETURN AND EPS PRICING MODEL:Earnings per Share (EPS) Pricing Model

- INTRODUCTION TO RISK, RISK AND RETURN FOR A SINGLE STOCK INVESTMENT:Diversifiable Risk, Diversification

- RISK FOR A SINGLE STOCK INVESTMENT, PROBABILITY GRAPHS AND COEFFICIENT OF VARIATION

- 2- STOCK PORTFOLIO THEORY, RISK AND EXPECTED RETURN:Diversification, Definition of Terms

- PORTFOLIO RISK ANALYSIS AND EFFICIENT PORTFOLIO MAPS

- EFFICIENT PORTFOLIOS, MARKET RISK AND CAPITAL MARKET LINE (CML):Market Risk & Portfolio Theory

- STOCK BETA, PORTFOLIO BETA AND INTRODUCTION TO SECURITY MARKET LINE:MARKET, Calculating Portfolio Beta

- STOCK BETAS &RISK, SML& RETURN AND STOCK PRICES IN EFFICIENT MARKS:Interpretation of Result

- SML GRAPH AND CAPITAL ASSET PRICING MODEL:NPV Calculations & Capital Budgeting

- RISK AND PORTFOLIO THEORY, CAPM, CRITICISM OF CAPM AND APPLICATION OF RISK THEORY:Think Out of the Box

- INTRODUCTION TO DEBT, EFFICIENT MARKETS AND COST OF CAPITAL:Real Assets Markets, Debt vs. Equity

- WEIGHTED AVERAGE COST OF CAPITAL (WACC):Summary of Formulas

- BUSINESS RISK FACED BY FIRM, OPERATING LEVERAGE, BREAK EVEN POINT& RETURN ON EQUITY

- OPERATING LEVERAGE, FINANCIAL LEVERAGE, ROE, BREAK EVEN POINT AND BUSINESS RISK

- FINANCIAL LEVERAGE AND CAPITAL STRUCTURE:Capital Structure Theory

- MODIFICATIONS IN MILLAR MODIGLIANI CAPITAL STRUCTURE THEORY:Modified MM - With Bankruptcy Cost

- APPLICATION OF MILLER MODIGLIANI AND OTHER CAPITAL STRUCTURE THEORIES:Problem of the theory

- NET INCOME AND TAX SHIELD APPROACHES TO WACC:Traditionalists -Real Markets Example

- MANAGEMENT OF CAPITAL STRUCTURE:Practical Capital Structure Management

- DIVIDEND PAYOUT:Other Factors Affecting Dividend Policy, Residual Dividend Model

- APPLICATION OF RESIDUAL DIVIDEND MODEL:Dividend Payout Procedure, Dividend Schemes for Optimizing Share Price

- WORKING CAPITAL MANAGEMENT:Impact of working capital on Firm Value, Monthly Cash Budget

- CASH MANAGEMENT AND WORKING CAPITAL FINANCING:Inventory Management, Accounts Receivables Management:

- SHORT TERM FINANCING, LONG TERM FINANCING AND LEASE FINANCING:

- LEASE FINANCING AND TYPES OF LEASE FINANCING:Sale & Lease-Back, Lease Analyses & Calculations

- MERGERS AND ACQUISITIONS:Leveraged Buy-Outs (LBOs), Mergers - Good or Bad?

- INTERNATIONAL FINANCE (MULTINATIONAL FINANCE):Major Issues Faced by Multinationals

- FINAL REVIEW OF ENTIRE COURSE ON FINANCIAL MANAGEMENT:Financial Statements and Ratios