|

SOLE PROPRIETORSHIP |

| << DIFFERENT BUSINESS ENTITIES: Commercial, Non-commercial organizations |

| Financial Statements Of Manufacturing Concern >> |

Financial

Accounting (Mgt-101)

VU

Lesson-32

SOLE

PROPRIETORSHIP

ILLUSTRATION

# 1

Prepare

profit & loss account

and balance sheet for

the year ending June 30,

2002 from the following

trial

balance

of Naseem Trading

Company.

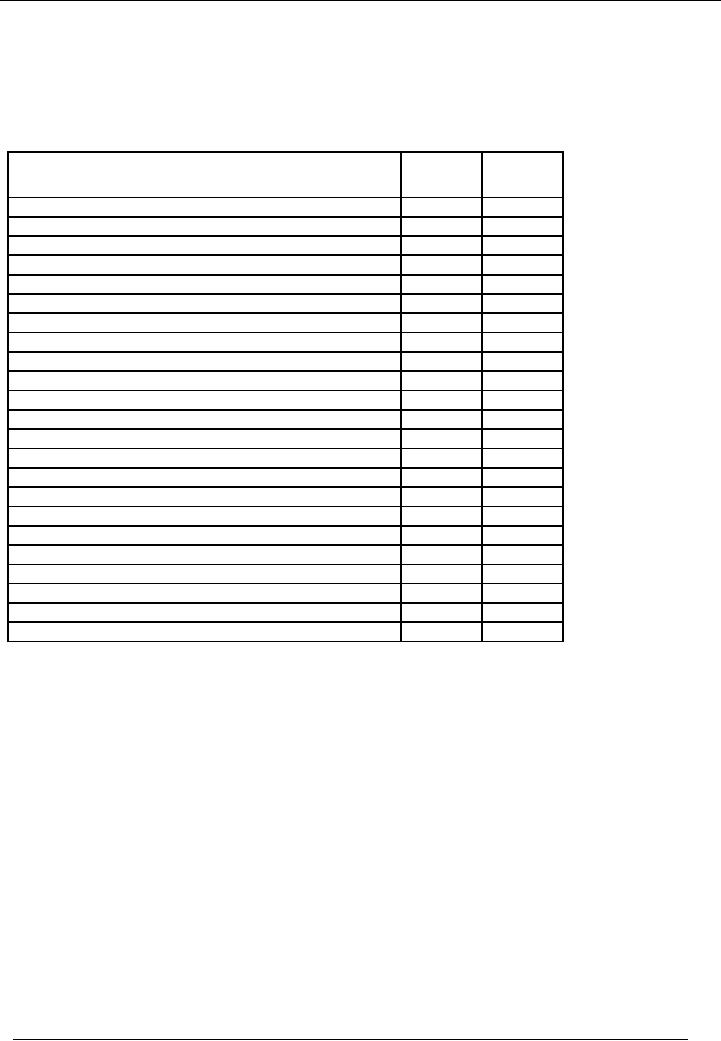

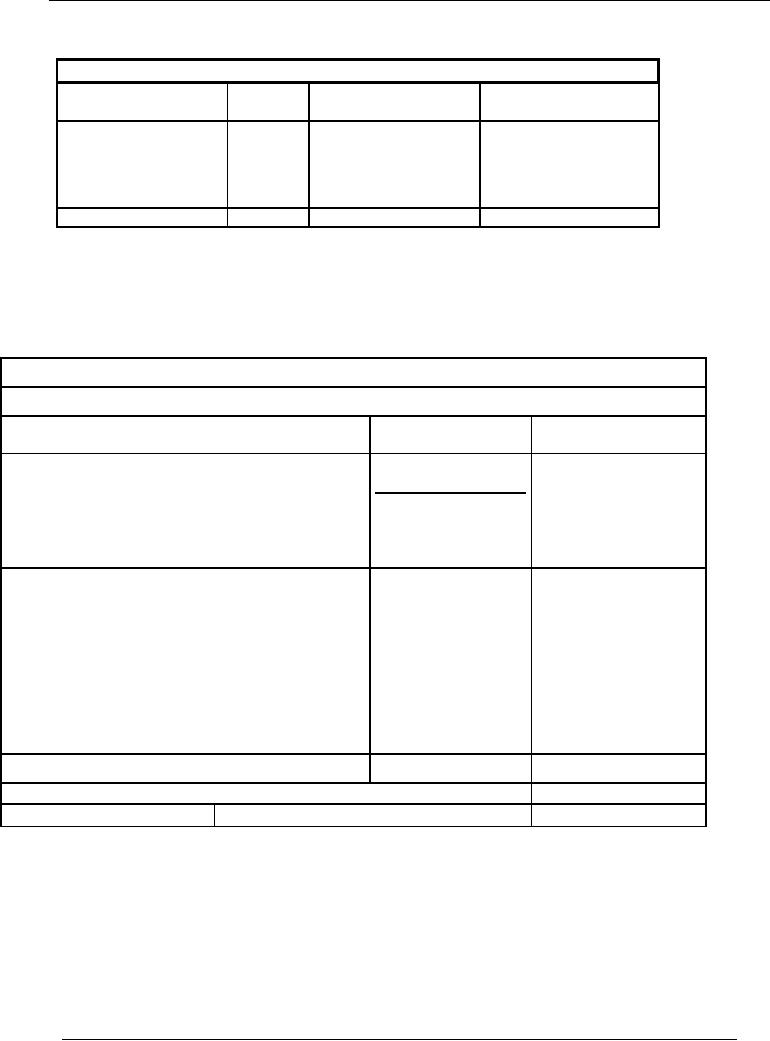

Particulars

Debit

Credit

Rs.

Rs.

Opening

Stock

115,200

Cash

in hand

10,800

Cash

at bank

52,600

Purchases

813,500

Returns

inward (Sales return)

13,600

Wages

169,600

Fuel &

power

94,600

Carriage

on sales

64,000

Carriage

on purchases

40,800

Building

640,000

Land

200,000

Machinery

400,000

Salaries

300,000

General

expenses

60,000

Drawings

12,000

Insurance

104,900

Sundry

Debtors

290,000

Sales

1,975,600

Returns

outwards (Purchase

returns)

10,000

Capital

1,090,000

Sundry

Creditors

126,000

Rent

received

180,000

Total

3,381,600

3,381,600

Following

additional information is supplied to

you:

· Closing

stock is valued at Rs.

136,000

· Machinery

& Building are to be depreciated @

10%

· Salaries

for the month of June, 2002

amounting to Rs. 30,000 are

unpaid

· Insurance

is paid in advance to the extent of Rs.

13,000

· Rent

receivable is Rs.

20,000

206

Financial

Accounting (Mgt-101)

VU

SOLUTION

When

additional information is given at the

end of the question, which

means these entries are

still to be

recorded

in the books of accounts. So, we shall

pass the entries

first:

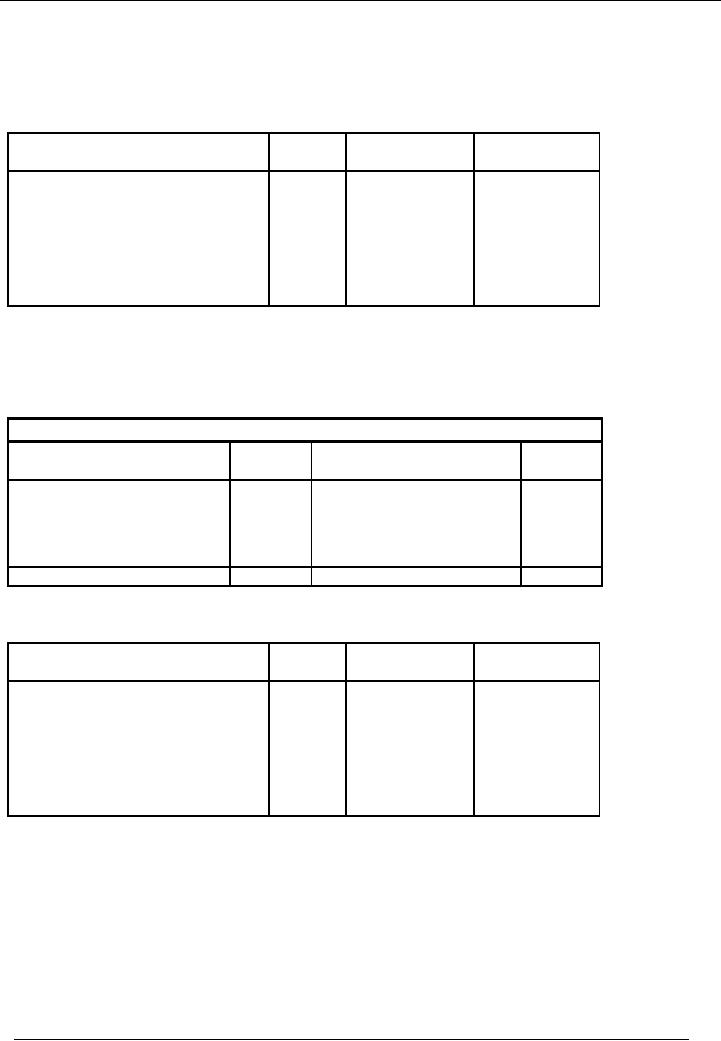

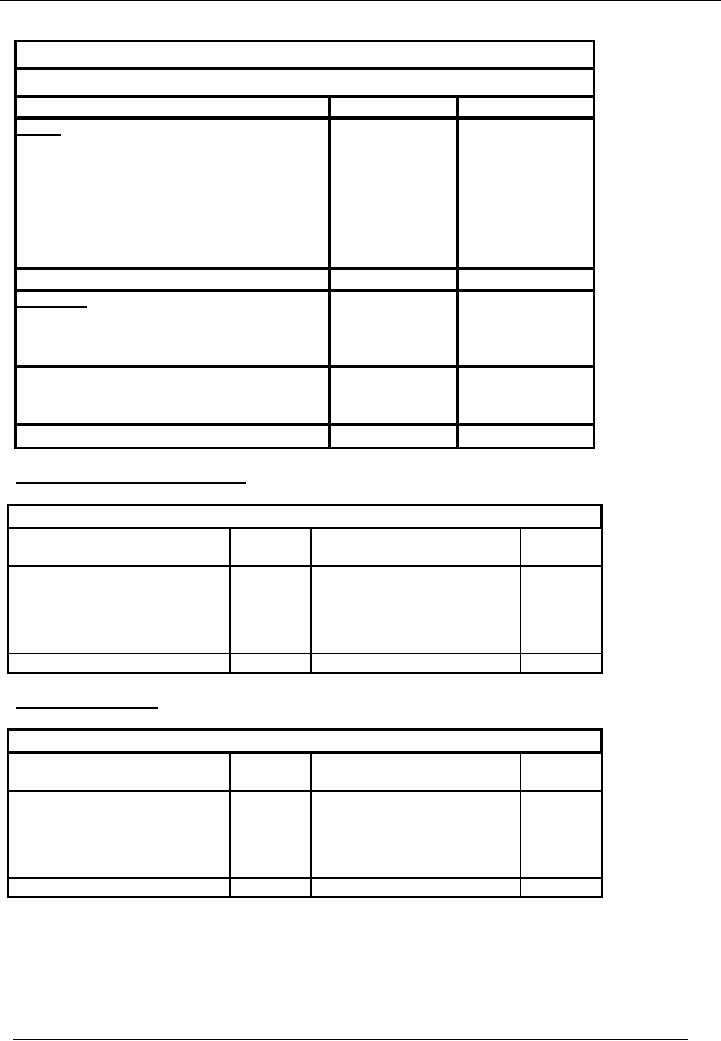

ENTRY

# 1

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Closing

stock account

136,000

Profit

& Loss account

136,000

Closing

stock is recorded

Closing

stock is presented in the profit &

loss account, credited in the

cost of goods sold and is

shown in the

balance

sheet under the heading of Current

Assets.

The

ledger account of closing

stock will be as

follows:

Stock

Account

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Closing

Stock

136,000

136,000

Balance

b/d

Total

136,000

Total

136,000

ENTRY

# 2

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Depreciation

account

40,000

Machinery

account

40,000

Depreciation

on machinery is

charged.

Depreciation

of machinery will be shown in the

profit & loss account under the

heading of Administrative

Expenses

and will be deducted from

the value of machinery account in the

balance sheet.

207

Financial

Accounting (Mgt-101)

VU

ENTRY

# 2

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Depreciation

account

64,000

Building

account

64,000

Depreciation

on building is charged.

Depreciation

of building will be shown in the

profit & loss account under the

heading of Administrative

Expenses

and will be deducted from

the value of building account in the

balance sheet.

The

ledger account of depreciation will be as

follows:

Depreciation

Account

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Dep.

of Machinery

40,000

Dep.

of building

64,000

Balance

b/d

104,000

Total

104,000

Total

104,000

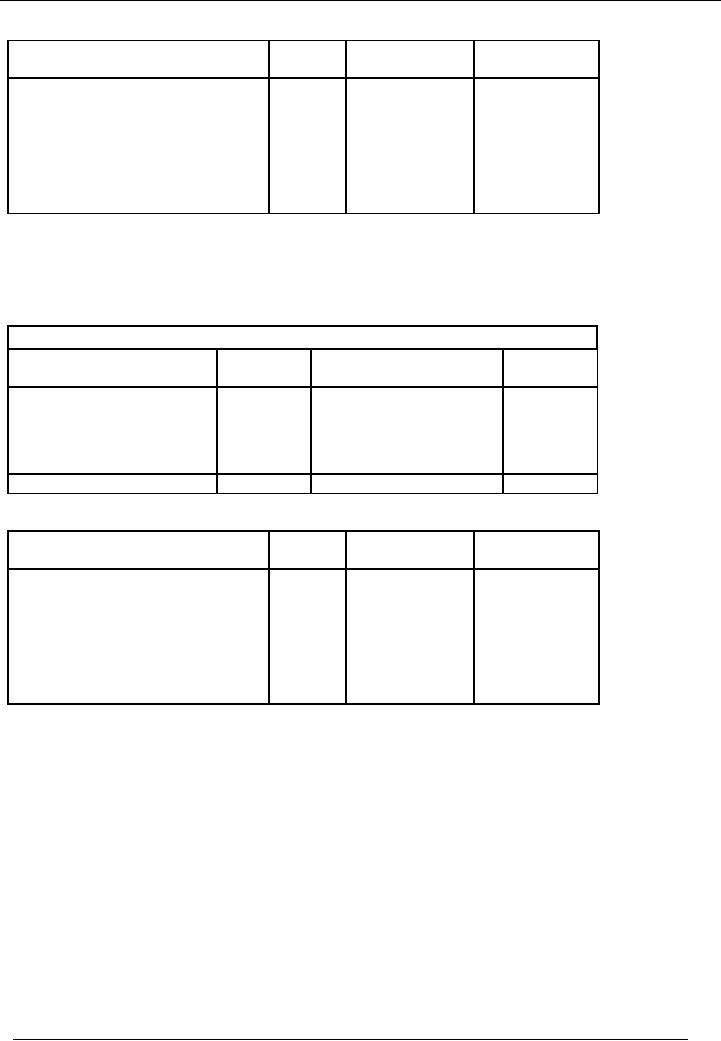

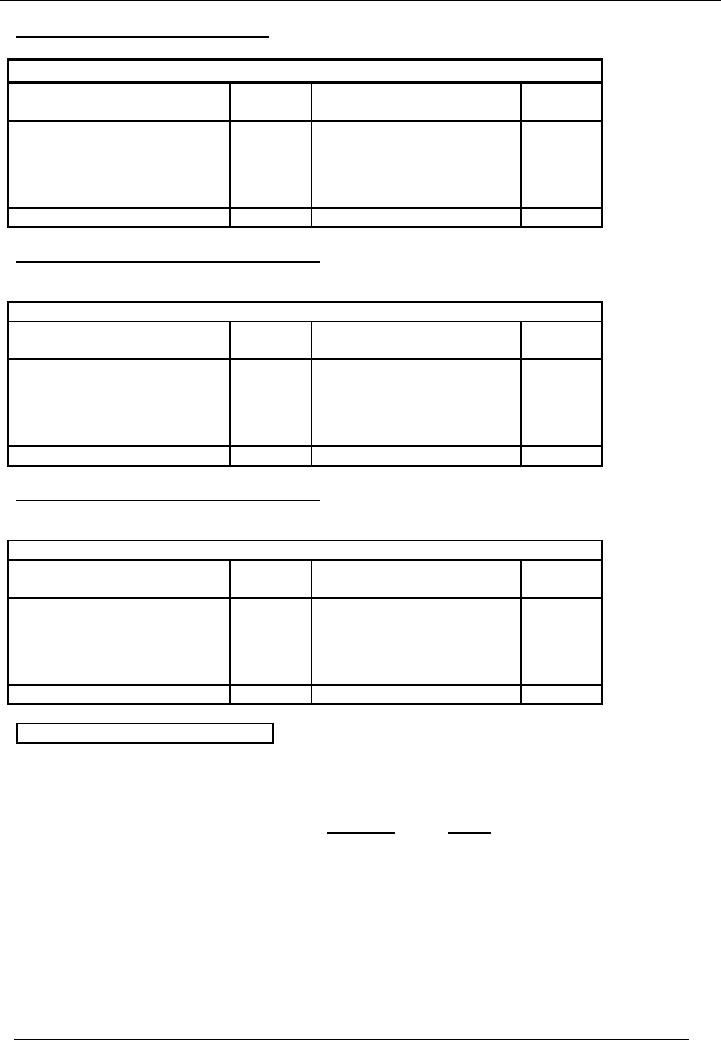

ENTRY

# 3

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Salaries

account

30,000

Salaries

payable account

30,000

Salaries

for the month of June

are

unpaid.

Salaries

account will be presented in the

profit & loss account under the

heading of Administrative

Expenses

and

salaries payable will be

presented in the balance sheet under the

heading of Current

Liabilities.

208

Financial

Accounting (Mgt-101)

VU

The

ledger account of salaries

will be as follows:

Salaries

Account

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Balance

c/d

300,000

Salaries

payable

30,000

Balance

b/d

330,000

Total

330,000

Total

330,000

ENTRY

# 4

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Advance

Insurance

13,000

Insurance

Account

13,000

Insurance

is paid in advance

Advance

insurance is our asset and

it will be shown in the balance

sheet under the heading of current

assets

and

advance insurance will be

deducted from the insurance

expenses.

The

ledger account of insurance

will be as follows:

Insurance

Account

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Balance

c/d

104,900

Advance insurance

13,000

Balance

b/d

91,900

Total

104,900

Total

104,900

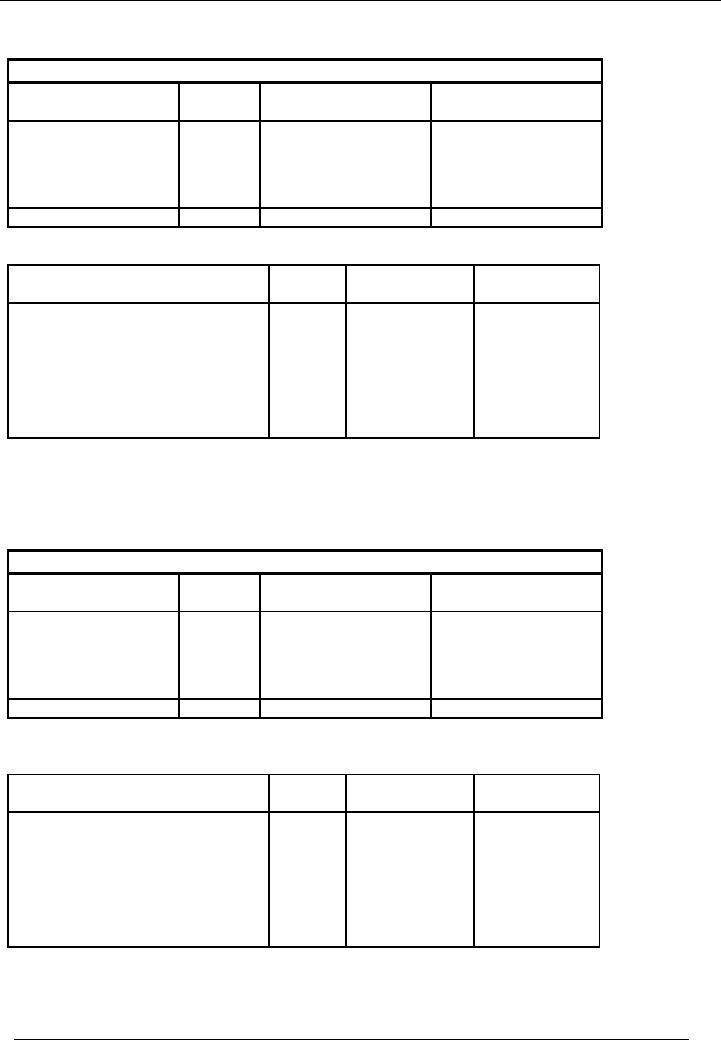

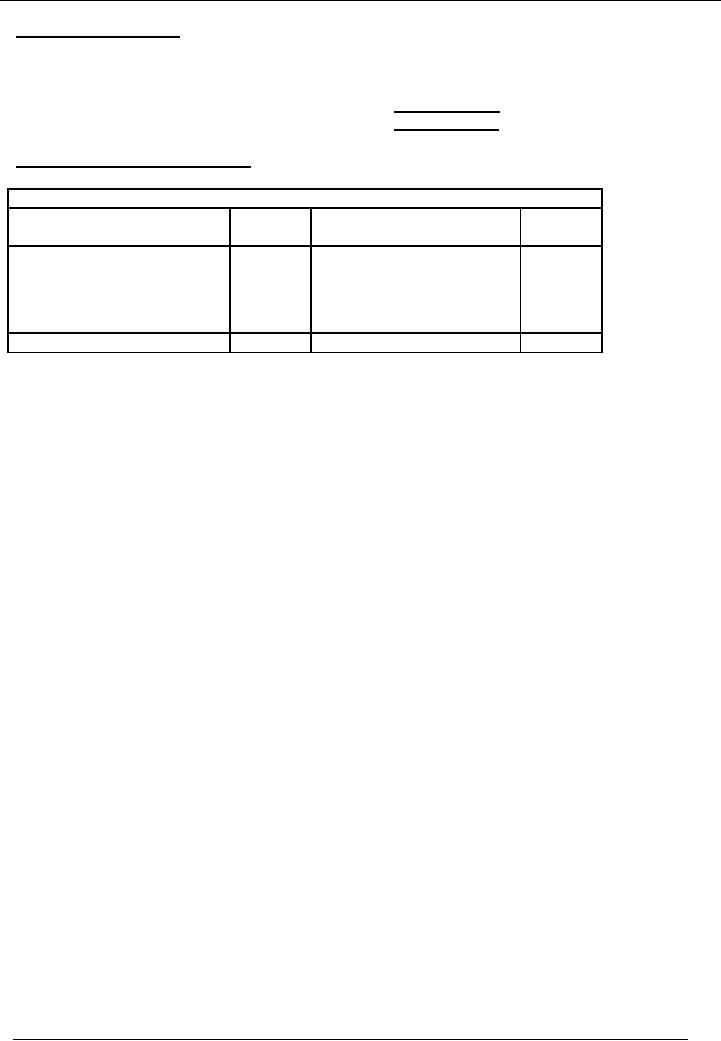

ENTRY

# 5

Particulars

Code

#

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Rent

Receivables

20,000

Rental

Income

20,000

Rental

Income receivable

Rent

receivables is our income

and it will be shown in the

balance sheet under the heading of

current assets

and

rent will be shown as income

in the profit & loss

account

209

Financial

Accounting (Mgt-101)

VU

The

ledger account of rent will

be as follows:

Rent

Account

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Balance

c/d

180,000

Receivable

20,000

Balance

b/d

200,000

Total

200,000

Total

200,000

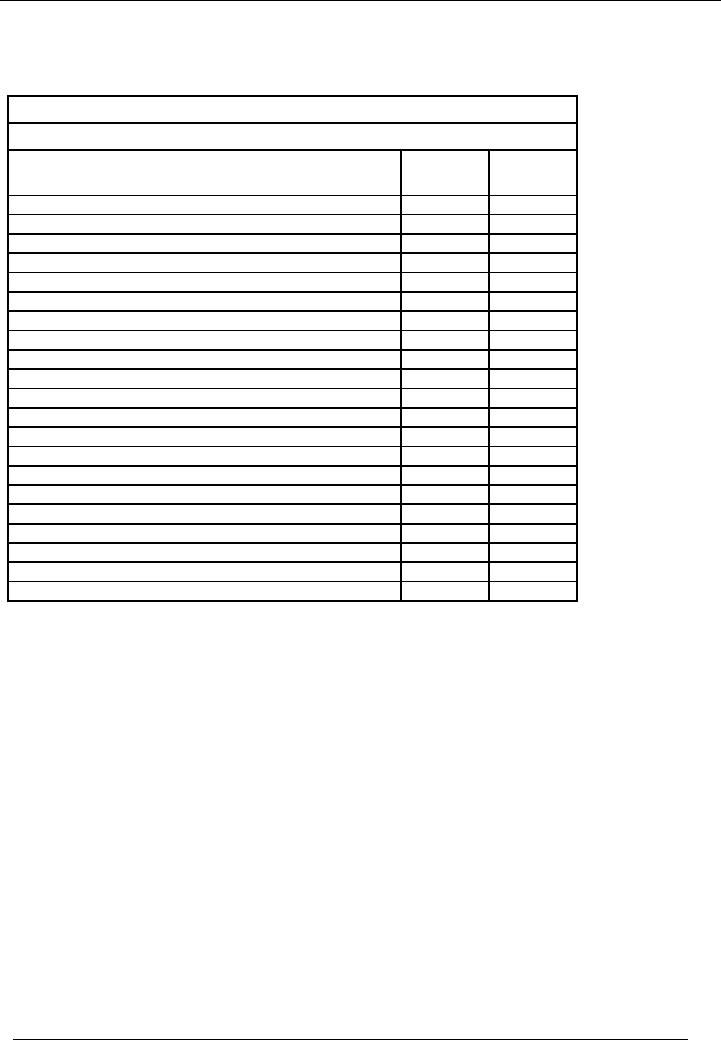

PROFIT

& LOSS ACCOUNT

Naseem

Trading Company

Profit &

Loss Account for the

year ended June 30,

2002

Particulars

Amount

Amount

Rs.

Rs.

Income

/ Sales / Revenue

1,975,600

Less:

Sales Return

1,962,000

(13,600)

Less:

Cost of Goods

Sold

(See

note # 1)

(1087700)

Gross

Profit

874300

sLess:

Administrative expenses

(See

note # 2)

(585900)

Less:

Selling Expenses

(64,000)

Carriage

on sales

Operating

profit

224400

Add:

Other Income (Rent received)

200000

Net

Income

424400

210

Financial

Accounting (Mgt-101)

VU

NOTE #

1

COST

OF GOODS SOLD

Rs.

Opening

stock

115,200

Add:

Purchases

813,500

Less:

purchase return

(10,000)

Add:

Carriage on purchases

40,800

Add:

Wages

169,600

Add:

Fuel and power

94600

Less:

Closing stock

(136,000)

Cost

of goods sold

1087700

NOTE #

2

ADMINISTRATIVE

EXPENSES

General

expenses

60,000

Insurance

91,900

Depreciation

on Machinery

40,000

Depreciation

on Building

64,000

Salaries

330,000

Total

Administrative Expenses

585900

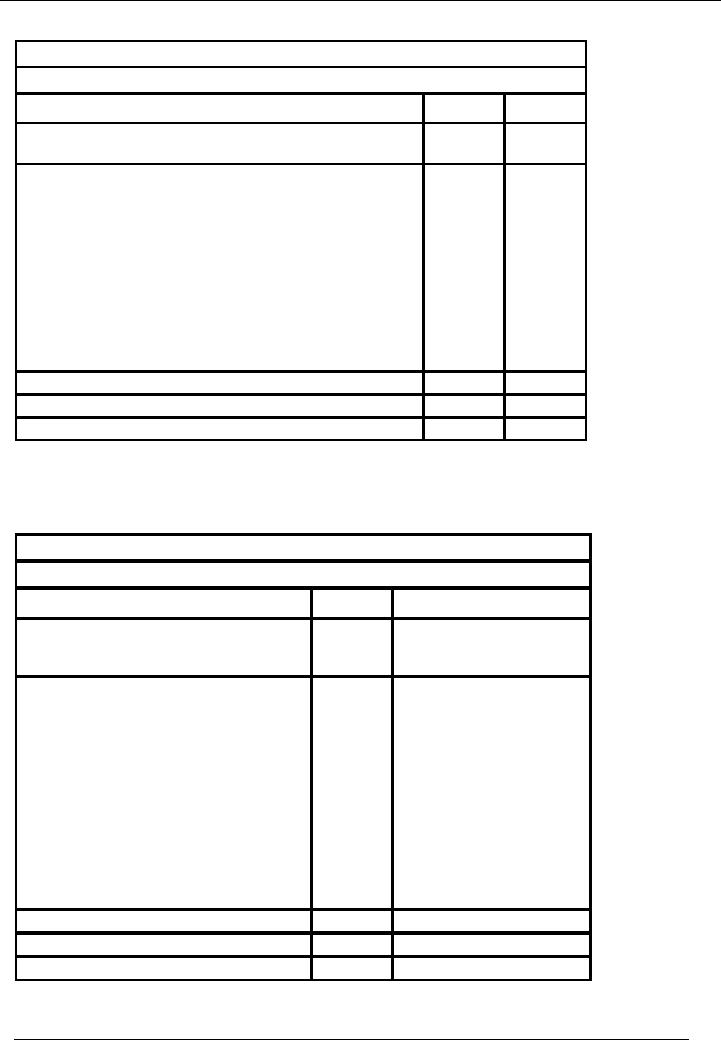

BALANCE

SHEET

Naseem

Trading Company

Balance

Sheet As At June 30,

2002

Liabilities

Assets

Particulars

Amount

Particulars

Amount

Rs.

Rs.

Capital

1,090,000

Fixed Assets

Add:

Profit and Loss Account

424,400

land

200,000

Less:

Drawings

(12,000)

Machinery

400,000

360,000

Less:

Dep.

(40,000)

Building

640,000

576,000

Less:

Dep.

(64,000)

1,502,400

1,136,000

Current

Liabilities

Current

Assets

Creditors

126,000

Debtors

290,000

Salaries

payable

30,000

Cash in hand

10,800

Cash

at bank

52,600

Closing

stock

136,000

Rant

receivable

20,000

Advance

insurance

13,000

Total

1,658,400

Total

1,658,400

211

Financial

Accounting (Mgt-101)

VU

ILLUSTRATION

# 2

Following

trial balance has been

extracted from the books of Arif

Traders on June 30,

2002

Arif

Traders

Trial

balance as on June 30,

2002

Particulars

Amount

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Sales

987,000

Stock

on June 30,2002

175,500

Material

Consumed

537,000

Cash

in Hand

10,500

Cash

at Bank

57,000

Capital

Account July 01,

2001

495,000

Drawings

142,500

Furniture

72,000

Rent

Paid

51,000

Wages

Paid

129,000

Discounts

Allowed

34,500

Discounts

Received

18,000

Debtors

246,000

Creditors

124,500

Provision

for Doubtful Debts Jul. 01

2001

13,500

Vehicles

120,000

Vehicle

Running Costs

22,500

Bad

Debts Written off

40,500

Total

1,638,000

1,638,000

Further

information available:

· Wages

and salaries payable on June

30, 2002 Rs.

4,500

· Rent

prepaid on June 30, 2002 Rs.

7,000

· Vehicle

running costs payable on

June 30 Rs. 3,000

· Increase

in provision for doubtful

debts Rs. 3,000

· Depreciation

rate is 12.5% for furniture

and 20% for vehicle.

You

are required to prepare Profit

and Loss Account for the

year and Balance Sheet as on

June 30, 2002

212

Financial

Accounting (Mgt-101)

VU

SOLUTION

Arif

Traders

Profit and

Loss Account for the

Year Ending June 30,

2002

Particulars

Rs.

Rs.

Sales

987,000

Less:

Cost of Goods Sold (material

consumed)

(537,000)

Gross

Profit

450,000

Less:

Expenses

Wages

and Salaries

Note

1

(133,500)

Rent

Note

2

(44,000)

Discount

Allowed

(34,500)

Vehicle

Running Cost

Note

3

(25,500)

Provision

for Doubtful Debt

Note

4

(43,500)

Depreciation

Note

5

(33,000)

(314,000)

Operating

profit

136000

Add:

Other income( Discount

receive)

18000

Net

Income

154,000

In the

profit & loss account

prepared above, the amount of bad

debts written off are

grouped with the

provision

for doubtful debts (see

note # 4)

In the

following presentation, bad

debts are shown separately

and working of provision of

bad debts is

shown

in Note # 4(a).

Arif

Traders

Profit

and Loss Account for the

Year Ending June 30,

2002

Particulars

Rs.

Rs.

Sales

987,000

Less:

Cost

of

Goods

Sold

(material

(537,000)

consumed)

Gross

Profit

450,000

Less:

Expenses

Wages

and Salaries

Note

1

(133,500)

Rent

Note

2

(44,000)

Discount

Allowed

(34,500)

Vehicle

Running Cost

Note

3

(25,500)

Bad

Debts

(40,500)

Provision

for Doubtful Debt

Note

4(a)

(3,000)

(314,000)

Depreciation

Note

5

(33,000)

Operating

Profit

136000

Add:

Other income( Discount

receive)

18000

Net

Income

154000

213

Financial

Accounting (Mgt-101)

VU

Arif

traders

Balance

Sheet As At June 30,

2002

Particulars

Amount

Rs.

Amount

Rs.

Assets

Fixed

Assets

Note

5

159,000

Current

Assets

Stocks

175,500

Debtors

Note

6

229,500

Prepaid

Expenses

7,000

Cash

at Bank

57,000

Cash

in Hand

10,500

479,500

Total

638,500

Liabilities

Capital

495,000

Profit

154,000

Less:

Drawings

(142,500)

506,500

Current

Liabilities

Creditors

124,500

Expenses

Payable

Note

7

7,500

132,000

Total

638,500

Note

# 1

Salaries

& Wages

Salaries

& Wages

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Salaries

& Wages Paid

129,000

Salaries

& Wages Payable

4,500

Transfer to

Profit & Loss

Account

133,500

Total

133,500

Total

133,500

Note

# 2

Rent

Salaries

& Wages

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Rent

Paid

51,000

Rent Payable

7,000

Transfer to

Profit & Loss

Account

44,000

Total

51,000

Total

51,000

214

Financial

Accounting (Mgt-101)

VU

Note

# 3

Vehicle

running cost

Vehicle

Running cost

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Cost

Paid

22,500

Cost

Payable

3,000

Transfer to

Profit & Loss

Account

25,500

Total

25,500

Total

133,500

Note

# 4

Provision

for doubtful debts

Provision

for doubtful debts

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Bad

Debts

40,500

Balance B/F

13,500

Transfer to

Profit & Loss

Balance

C/F

16,500

Account

43,500

Total

57,000

Total

57,000

Note

# 4(a)

Provision

for doubtful debts

Provision

for doubtful debts Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Balance

B/F

13,500

Transfer to

Profit & Loss

Balance

C/F

16,500

Account

3,000

Total

16,500

Total

16,500

Note

# 5

Fixed

Assets at WDV

Cost

Rate

Dep.

WDV

Furniture

72,000

12.5%

9,000

63,000

96,000

Vehicle

120,000

20%

24,000

33,000

159,000

215

Financial

Accounting (Mgt-101)

VU

Note

# 6

Debtors

Debtors

246,000

Less:

Provision for

Doubtful

Debts (note

4)

(16,500)

229,500

Note

# 7

Expenses

Payable

Expenses

Payable

Account

Code --------

Particulars

Amount

Particulars

Amount

Dr.

(Rs.)

Cr.

(Rs.)

Salaries

4,500

Vehicle

running cost

3,000

Balance

C/F

7,500

Total

7,500

Total

7,500

216

Table of Contents:

- Introduction to Financial Accounting

- Basic Concepts of Business: capital, profit, budget

- Cash Accounting and Accrual Accounting

- Business entity, Single and double entry book-keeping, Debit and Credit

- Rules of Debit and Credit for Assets, Liabilities, Income and Expenses

- flow of transactions, books of accounts, General Ledger balance

- Cash book and bank book, Accounting Period, Trial Balance and its limitations

- Profit & Loss account from trial balance, Receipt & Payment, Income & Expenditure and Profit & Loss account

- Assets and Liabilities, Balance Sheet from trial balance

- Sample Transactions of a Company

- Sample Accounts of a Company

- THE ACCOUNTING EQUATION

- types of vouchers, Carrying forward the balance of an account

- ILLUSTRATIONS: Ccarrying Forward of Balances

- Opening Stock, Closing Stock

- COST OF GOODS SOLD STATEMENT

- DEPRECIATION

- GROUPINGS OF FIXED ASSETS

- CAPITAL WORK IN PROGRESS 1

- CAPITAL WORK IN PROGRESS 2

- REVALUATION OF FIXED ASSETS

- Banking transactions, Bank reconciliation statements

- RECAP

- Accounting Examples with Solutions

- RECORDING OF PROVISION FOR BAD DEBTS

- SUBSIDIARY BOOKS

- A PERSON IS BOTH DEBTOR AND CREDITOR

- RECTIFICATION OF ERROR

- STANDARD FORMAT OF PROFIT & LOSS ACCOUNT

- STANDARD FORMAT OF BALANCE SHEET

- DIFFERENT BUSINESS ENTITIES: Commercial, Non-commercial organizations

- SOLE PROPRIETORSHIP

- Financial Statements Of Manufacturing Concern

- Financial Statements of Partnership firms

- INTEREST ON CAPITAL AND DRAWINGS

- DISADVANTAGES OF A PARTNERSHIP FIRM

- SHARE CAPITAL

- STATEMENT OF CHANGES IN EQUITY

- Financial Statements of Limited Companies

- Financial Statements of Limited Companies

- CASH FLOW STATEMENT 1

- CASH FLOW STATEMENT 2

- FINANCIAL STATEMENTS OF LISTED, QUOTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES