|

Preparing Financial Statements |

| << Adjusting Entry to record Expenses on Fixed Assets |

| Closing entries in Accounting Cycle >> |

Financial

Statement Analysis-FIN621

VU

Lesson-8

ACCOUNTING

CYCLE/PROCESS

(Continued)

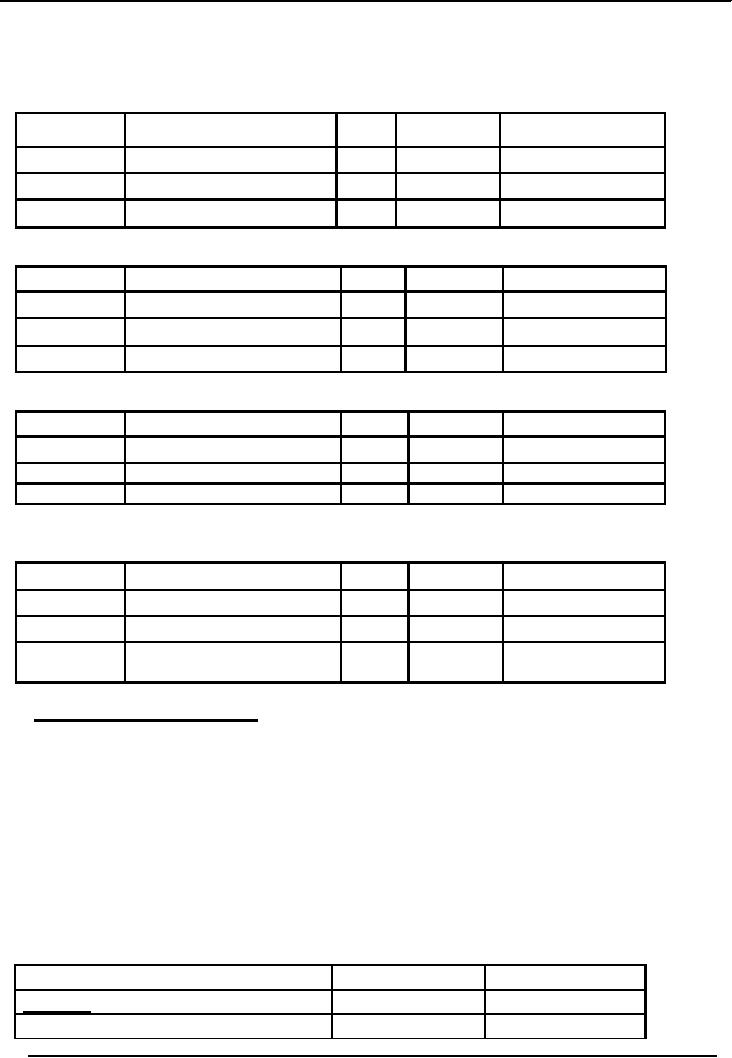

Pre-paid

costs e.g. Pre-paid rent,

will be recorded as follows:

Date

Description

L/F

Dr.

Cr.

Prepaid

Rent

12,000

Cash

Account

12,000

Rent

paid in advance

Pre-paid

costs e.g. Pre-paid rent,

will be recorded as follows:

Date

Description

L/F

Dr.

Cr.

Rent

Expense

1,000

Prepaid

Rent

1,000

Recording

rent expense

Pre-paid

costs e.g. Pre-paid Insurance will be

recorded as follows:

Date

Description

L/F

Dr.

Cr.

Prepaid

Insurance

12,000

Cash

Account

12,000

Insurance

paid in advance

Pre-paid

costs e.g. Pre-paid Insurance will be

recorded as follows:

Date

Description

L/F

Dr.

Cr.

Insurance

Expense

1,000

Prepaid

Insurance

1,000

Recording

Insurance expense

g)

Preparing Financial

Statements

Now

we come to the all-important step of

preparing Financial Statements

from

Accounting

Records. Income Statement is prepared

from Adjusted Trial Balance,

first. Then Statement

of

Owner's equity between Income

Statement and Balance Sheet is prepared.

For this, Net profit/loss

in

Income

Statement is added to/

subtracted from owner's

equity in "Owner's equity

Statement", and the

total/net

is then transferred to Balance Sheet.

After the preparation of Balance Sheet,

the fourth

Financial

Statement i.e. Cash flow

Statement is prepared separately.

As a

practical illustration, let us prepare

these Financial

Statements.

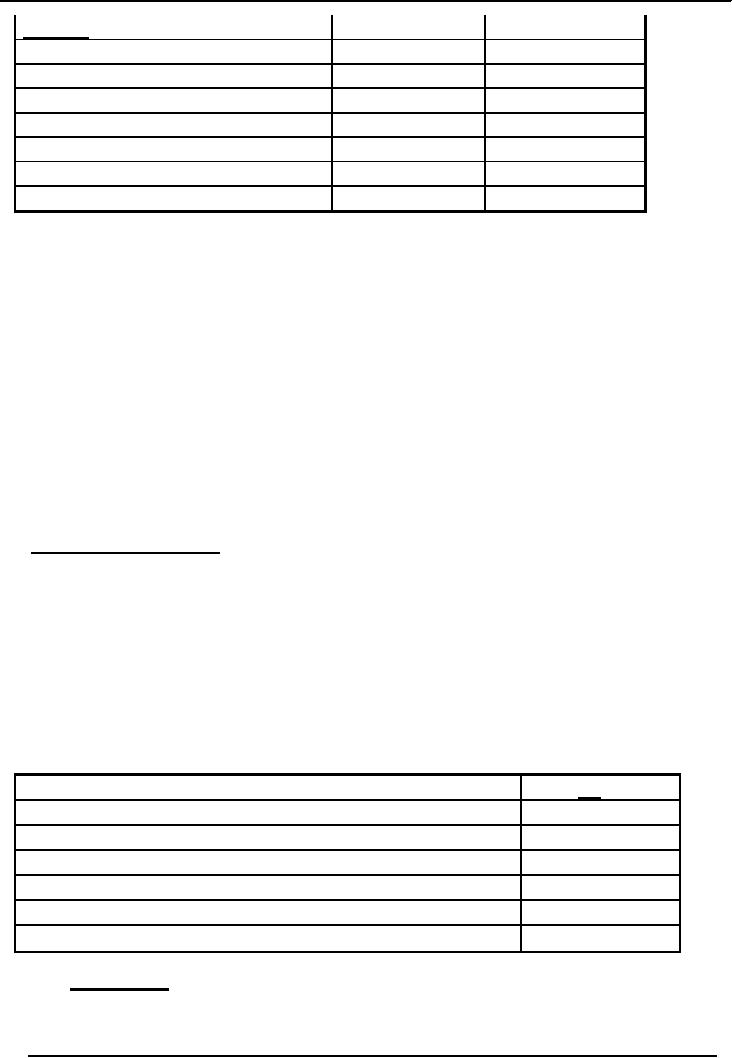

Income

Statement

For

the period ending August 31,

2006

Particulars

Rs.

Rs.

Revenues

Sales

Commission earned.

10,640

32

Financial

Statement Analysis-FIN621

VU

Expenses

Advertising

expenses.

645

Salaries

expenses.

7,400

Telephone

expenses.

400

Depreciation

expense: building

150

Depreciation

expense: office

equipment

45

8,640

Net

Income.

2,000

The

revenue and expenses shown in the income

statement are taken directly

from the company's

adjusted

trial balance. Our measurement of net

income is not absolutely

accurate or precise, because

of

the

assumptions

and estimates in the

accounting process. An income

statement has certain

limitations.

Remember

that the amount shown for depreciation

expense or based on estimates

of the

useful lives of

the

company's building and office

equipment. Also the income

statement includes only

those events that

have

been evidence

by business transactions. Alternative

titles for the income

statement include

earnings

statement, statement of operations,

and profit and loss

statement.

However, income

statement

is by

far the most popular term

for this important financial

statement. In summary, we can say

that an

income

statement is used to summaries the

operating

results of

business by matching the revenue

earned

during a given time period

with the expenses incurred in

obtaining that revenue.

Note:

This is case of service business, and

sole proprietorship. In the case of

Merchandise

&

Manufacturing business:

Net

Income=SalesCost of Goods soldOther

expenses.

ii)

Owner's equity Statement

Owner's

equity which was Rs.180, 000

on July 31, 2006 increases

by Rs.2000 due to

profitable

operations during the month of August,

2006. Net income is transferred to

owner's equity

statement,

which is further transferred to Balance

Sheet. Correspondingly, there would be

either

increase

in Assets (Left) side of the

Accounting Equation (or Balance

Sheet), or decrease in

Liabilities

(Right)

side, to maintain balance.

Statement

of Owner's equity summarizes

increase/decrease in owner's equity

during

accounting

period. It is increased due to profit and

additional investment by the owner. It is

decreased

due to

loss and withdrawal/drawing by the

owner.

Statement of

Owner's equity for the

month of August,

2006

Particulars

Rs.

Khizr,

capital July 31,

2006

180,000

Add:

Net income for August,

2006

2,000

Additional

investment by owner

4,000

Sub

total

186,000

Less

withdrawal/drawing by owner

3,000

Owner's

equity August 31,

2006

183,000

III.

Balance

Sheet

The

balance sheet lists the

amounts of the company's assets,

liabilities, and owner's

equity at

the end of

accounting period. The

balances of the assets and

liability accounts are taken

directly

33

Financial

Statement Analysis-FIN621

VU

from

the adjusted trial balance. Cash is

listed first among the assets. It is

often followed by

such

asset

as marketable securities, short-term notes

receivable, accounts receivable,

inventories, and

supplies.

These are the most common

examples of current assets.

The term "current

assets"

includes

cash and those assets

that will be quickly

converted to cash or used up in

operations

.

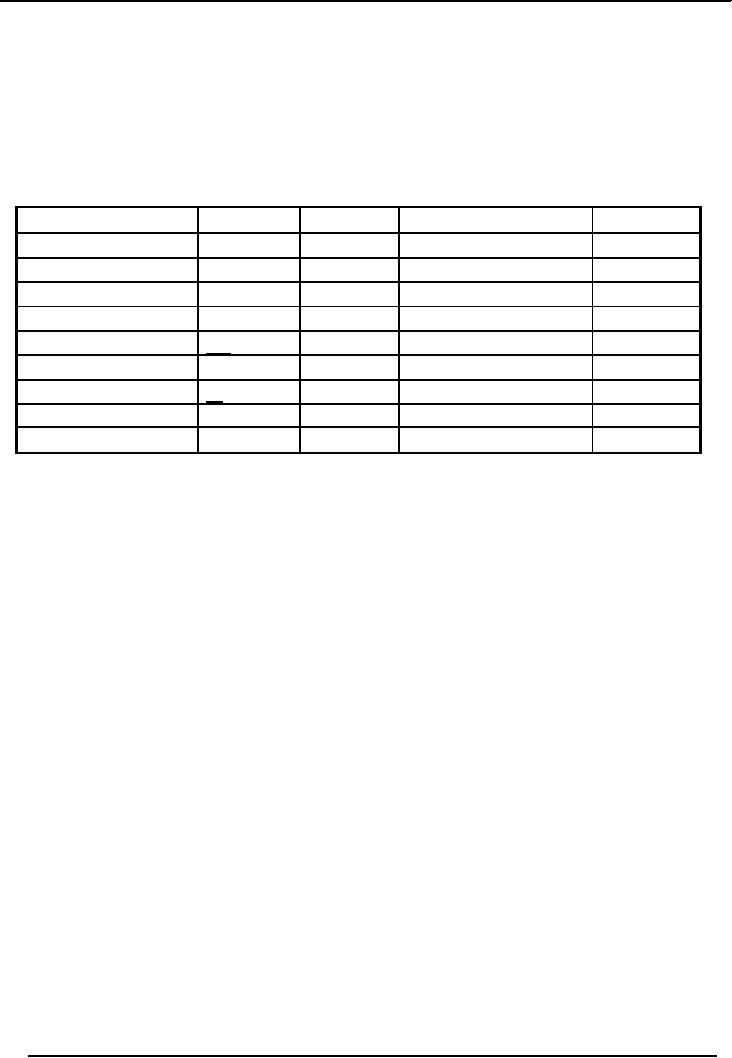

Khizr

Property Dealer

Balance

Sheet

As on August

31,2006

Assets

Rs.

Rs.

Liabilities

& Equity

Rs.

Cash

16,105

Accounts

Payable

23,814

Accounts

Receivables

19,504

Owner's

equity

183,000

Land

130,000

Building

36,000

Less

Accumulated Dep:

150

35,850

Office

Equipment

5,400

Less

Accumulated Dep:

45

5,355

TOTAL

206,814

TOTAL

206,814

-

Owner's

equity obtained from Owner's

equity statement

34

Table of Contents:

- ACCOUNTING & ACCOUNTING PRINCIPLES

- Dual Aspect of Transactions

- Rules of Debit and Credit

- Steps in Accounting Cycle

- Preparing Balance Sheet from Trial Balance

- Business transactions

- Adjusting Entry to record Expenses on Fixed Assets

- Preparing Financial Statements

- Closing entries in Accounting Cycle

- Income Statement

- Balance Sheet

- Cash Flow Statement

- Preparing Cash Flows

- Additional Information (AI)

- Cash flow from Operating Activities

- Operating Activities portion of cash flow statement

- Cash flow from financing Activities

- Notes to Financial Statements

- Charging Costs of Inventory to Income Statement

- First-in-First - out (FIFO), Last-in-First-Out (LIFO)

- Depreciation Accounting Policies

- Accelerated-Depreciation method

- Auditors Report, Opinion, Certificate

- Management Discussion & Analyses (MD&A)

- TYPES OF BUSINESS ORGANIZATIONS

- Incorporation of business

- Authorized Share Capital, Issued Share Capital

- Book Values of equity, share

- SUMMARY

- SUMMARY

- Analysis of income statement and balance sheet:

- COMMON SIZE AND INDEX ANALYSIS

- ANALYSIS BY RATIOS

- ACTIVITY RATIOS

- Liquidity of Receivables

- LEVERAGE, DEBT RATIOS

- PROFITABILITY RATIOS

- Analysis by Preferred Stockholders

- Efficiency of operating cycle, process

- STOCKHOLDERS EQUITY SECTION OF THE BALANCE SHEET 1

- STOCKHOLDERS EQUITY SECTION OF THE BALANCE SHEET 2

- BALANCE SHEET AND INCOME STATEMENT RATIOS

- Financial Consultation Case Study

- ANALYSIS OF BALANCE SHEET & INCOME STATEMENT

- SUMMARY OF FINDGINS