|

Opening Stock, Closing Stock |

| << ILLUSTRATIONS: Ccarrying Forward of Balances |

| COST OF GOODS SOLD STATEMENT >> |

Financial

Accounting (Mgt-101)

VU

Lesson-15

STOCK

Stock

is termed as "the value of

goods available to the business

that are ready for

sale". For accounting

purposes,

stock is of two

types:

· Opening

stock

· Closing

stock

Opening

stock is the

value of goods available for

sale in the beginning of an accounting

period.

Closing

stock is the

value of goods unsold at the end of the

accounting period.

Journal

Entries

(In

Case of Trading

Concern)

Journal

entries for those goods

which are bought for

resale purposes are as

follows:

Purchase

of goods:

Debit:

Stock/Material

Account

Credit:

Cash/Bank/Creditor

Consumption of

goods

Debit:

Cost

of goods sold

Credit:

Stock

Payment

in case of credit purchase

Debit:

Creditors

Account

Credit:

Cash/Bank

( In

Case of Manufacturing

Concern)

·

In

case of manufacturer there

are at least two types of

Stock Accounts:

o Raw

Material Stock

Account

o Finished

Goods Stock Account

Raw

material

Raw

material is the basic part of an item,

which is processed to make a

complete item

Finished

goods

Finished

goods contain the items that

are ready for sale,

but could not be sold in

that accounting

period.

Work

in process

In manufacturing

concern, raw material is put

in a process to convert it into

finished goods. At the end

of

accounting

period, some part of raw

material remains under process.

i-e. it is neither in shape of

raw material

nor in

shape of finished goods.

Such items are taken in

stock as work in

process.

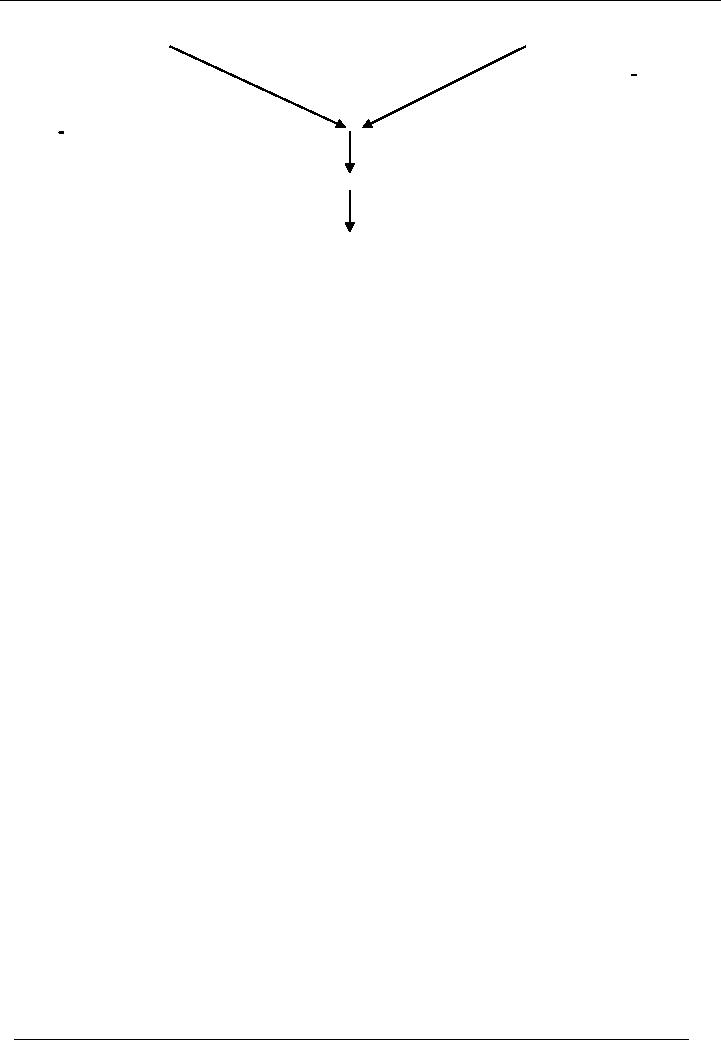

Flow

of costs

108

Financial

Accounting (Mgt-101)

VU

Raw

Material Stock

Other

Costs Accounts

Work

in Process Account

Finished

Goods Account

Cost

of Goods Sold

Account

In manufacturing

concern, Raw material stock

is put into process. For

accounting purposes, all

value of

stock

and other manufacturing costs

are charged to work in

process account. When the

process is completed

and

the goods are prepared, all

the value of work in process is

charged to finished goods

account. The

business

sells finished goods for the

whole accounting year. At the

end of the year, goods that

are unsold are

deducted

from cost of goods sold

account.

Journal

Entries (Manufacturing

Concern)

Purchase

of raw material

Debit:

Stock/Material

Account

Credit:

Cash/Bank/Creditors

Other

direct costs incurred

Debit:

Relevant

cost/Expense Head

Credit:

Cash/Bank/Payables

Raw

material issued and other

costs allocated to production of

units

Debit:

Work

in process

Credit:

Stock

Material Account

Debit:

Work

in process

Credit:

Relevant

Expense Head Account

When

production is completed

Debit:

Finished

Goods Stock Account

Credit:

Work

in process account

Entry

for Cost of sale

Debit:

Cost

of Goods Sold Account

Credit:

Finished

Goods Stock Account

Entry

for sale of goods

Debit:

Cash/Account

receivable Account

109

Financial

Accounting (Mgt-101)

VU

Credit:

Sales

Account

Return of

purchased material

There

are two options for

recording purchase material

return

· Option

1

Debit:

Goods

Return Account

Credit:

Stock

Material Account

AND

Debit:

Cash/Bank

Account

Credit:

Goods

Return Account

OR

If our

supplier supplies us some other

material in exchange of material

returned. Then:

Debit

Raw

Material Stock

Account

Credit:

Goods

Return Account

In the

first case above, cash is

received in return of goods. In the

second case, defective goods

are

exchanged

with quality goods. That is

why, we debited our stock account.

Both entries are correct

for

return

of purchased items.

Option

2

Debit:

Cash/Creditor

Account

Credit:

Stock

Account

Example

1

· Record

the following transactions:

1.

Purchased goods for cash

Rs. 10,000

2.

Purchased goods on credit from

ABC Co. Rs.

25,000

3.

Sold goods whose cost

was Rs. 20,000

4.

Returned goods to ABC Co.

that originally cost Rs.

5,000

5.

Paid to ABC Co. Rs.

15,000 through cheque

6.

Sold goods whose cost

was Rs. 5,000

·

Answer

following questions.

1.

What is the cost of goods

sold?

2.

What is the value of closing

stock?

3.

What amount is payable to ABC

Co.?

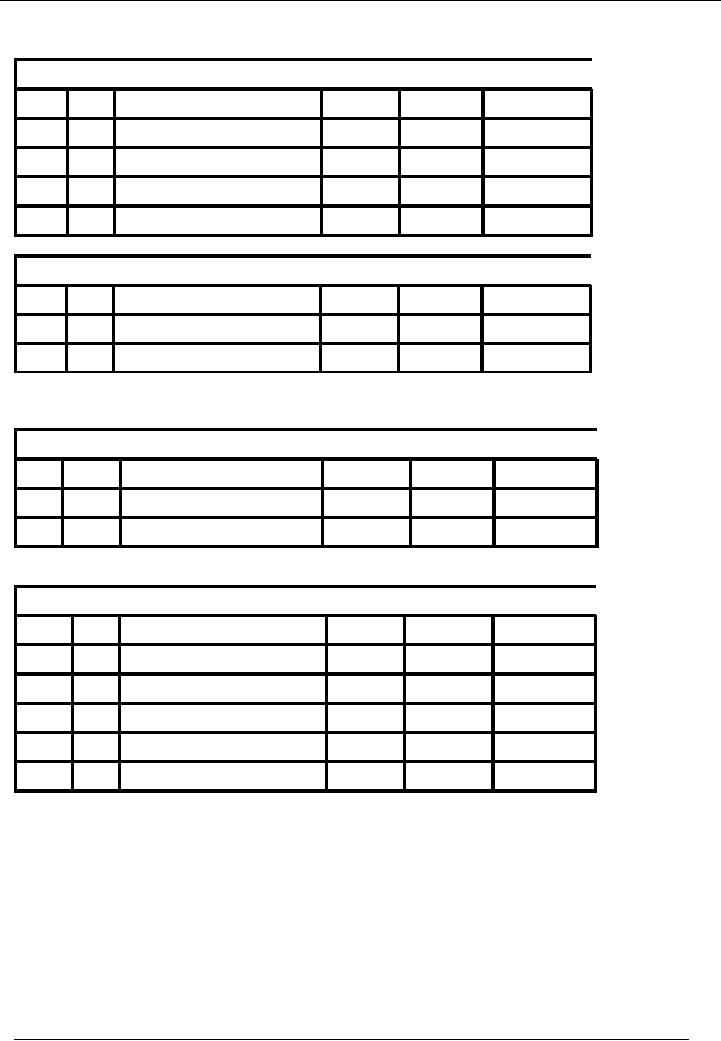

1

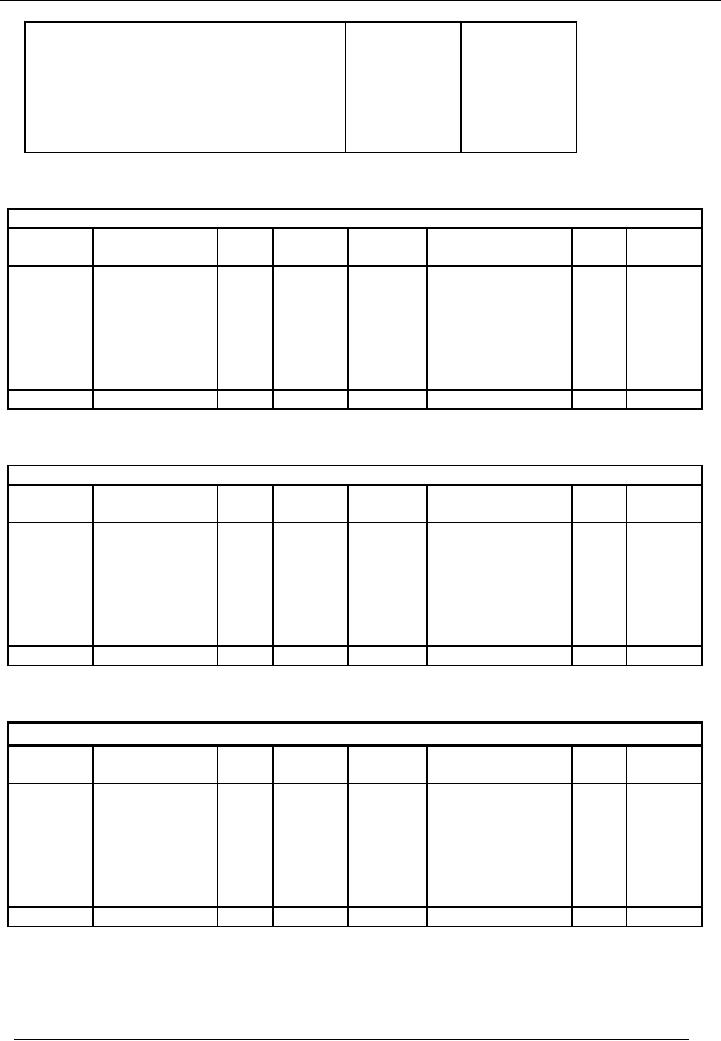

Purchased goods for cash

Rs. 10,000

Cash

Account

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

(10,000)

110

Financial

Accounting (Mgt-101)

VU

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased goods on credit from

ABC Co. Rs.

25,000

ABC

Co.

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

2

Purchased

goods from ABC

25,000

(25,000)

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased

goods from ABC

25,000

35,000

111

Financial

Accounting (Mgt-101)

VU

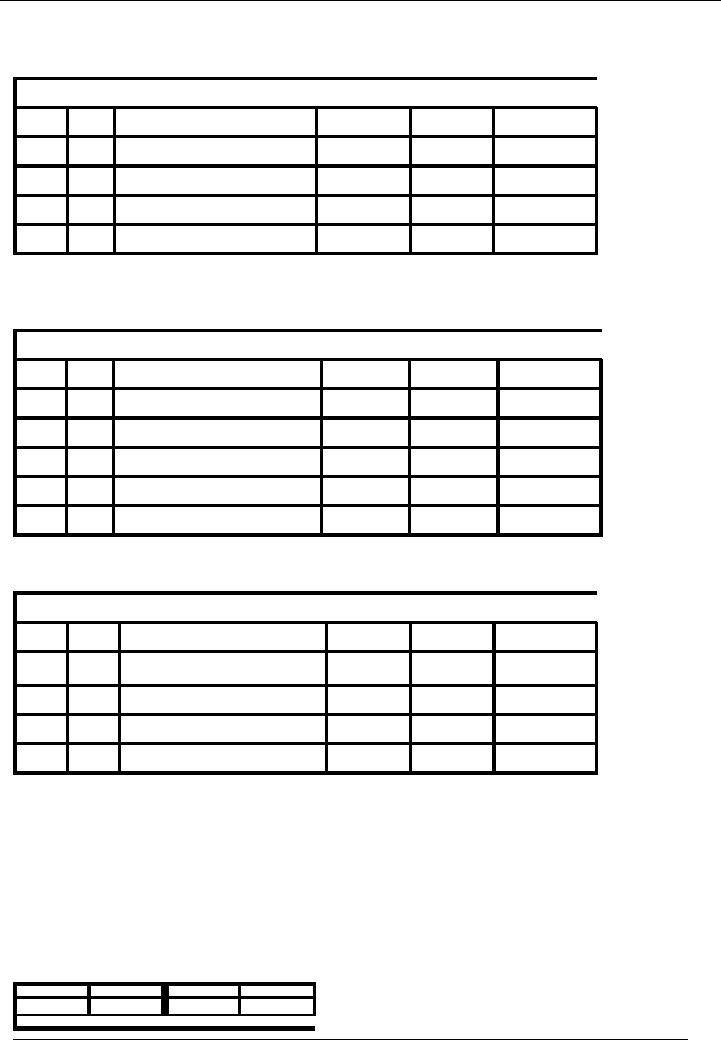

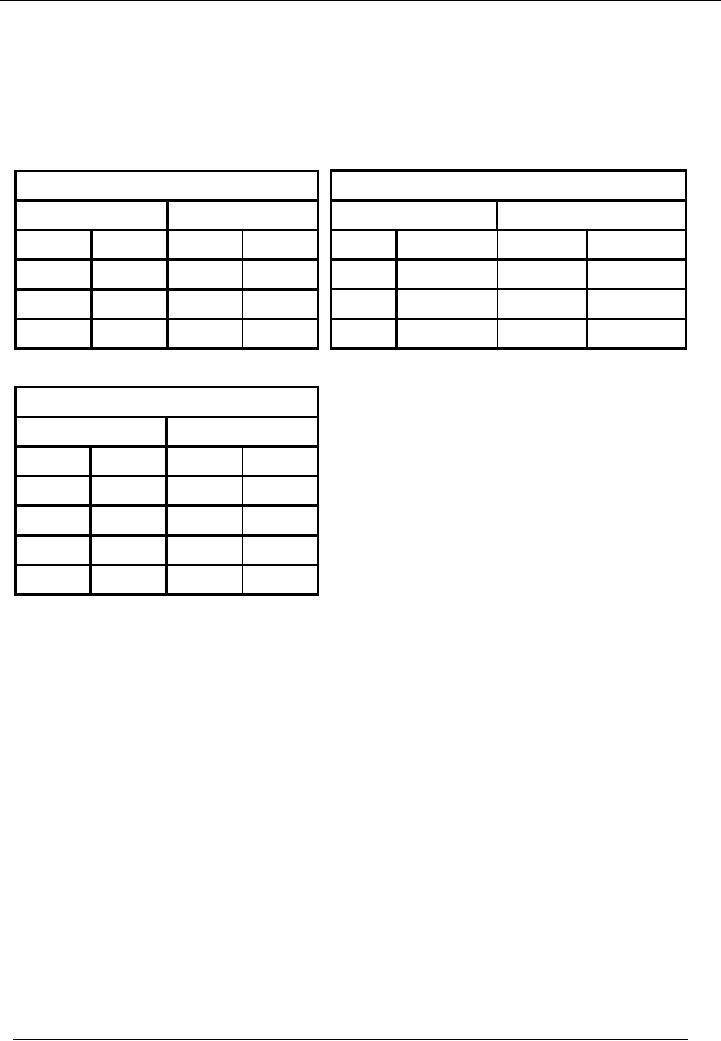

3

Sold goods whose cost

was Rs. 20,000

Cost

of Goods Sold

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

3

Goods

sold

20,000

20,000

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased

goods from ABC

25,000

35,000

3

Goods

sold

20,000

15,000

4

Returned goods to ABC Co.

cost Rs. 5,000

ABC

Co.

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

2

Purchased

goods from ABC

25,000

(25,000)

4

Returned

goods to ABC

5,000

(20,000)

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased

goods from ABC

25,000

35,000

3

Goods

sold

20,000

15,000

4

Returned

goods to ABC

5,000

10,000

112

Financial

Accounting (Mgt-101)

VU

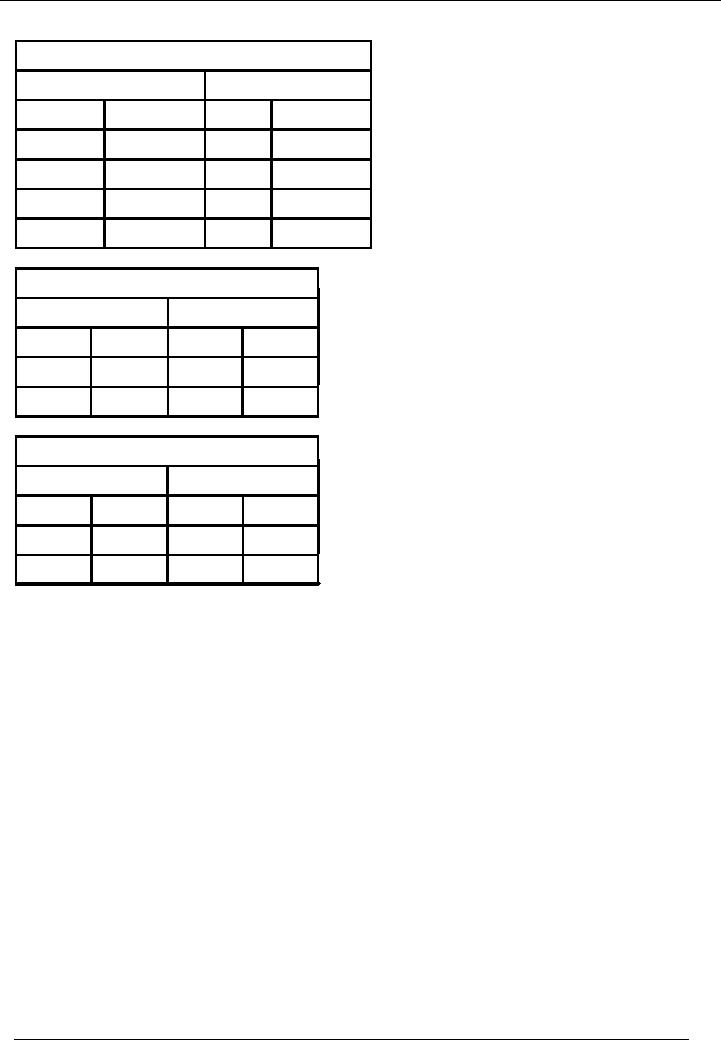

5

Paid to ABC Co. Rs.

15,000 through cheque

ABC

Co.

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

2

Purchased

goods from ABC

25,000

(25,000)

4

Returned

goods to ABC

5,000

(20,000)

5

Paid

to ABC

15,000

(5,000)

Bank

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

5

Paid

to ABC

15,000

6

Sold goods whose cost

was Rs. 5,000

Cost

of Goods Sold

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

3

Goods

sold

20,000

20,000

6

Goods

sold

5,000

25,000

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased

goods from ABC

25,000

35,000

3

Goods

sold

20,000

15,000

4

Returned

goods to ABC

5,000

10,000

6

Goods

sold

5,000

5,000

113

Financial

Accounting (Mgt-101)

VU

Q1

What is the cost of goods

sold?

Cost

of Goods Sold

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

3

Goods

sold

20,000

20,000

6

Goods

sold

5,000

25,000

Q2

What is the value of closing

stock?

Stock

Account Code --

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

1

Purchased

goods for cash

10,000

10,000

2

Purchased

goods from ABC

25,000

35,000

3

Goods

sold

20,000

15,000

4

Returned

goods to ABC

5,000

10,000

6

Goods

sold

5,000

5,000

Q3

What amount is payable to ABC

Co.?

ABC

Co.

Code

--

Date

No.

Narration

Dr.

Rs.

Cr.

Rs.

Bal.

Dr/(Cr)

2

Purchased

goods from ABC

25,000

(25,000)

4

Returned

goods to ABC

5,000

(20,000)

5

Paid

to ABC

15,000

(5,000)

Example

2

·

Using the

following data calculate the

Cost of Goods Sold of XYZ

Co.

Stock

levels

Opening

Rs.

Closing

Rs.

Raw

material

100,000

85,000

Work

in process

90,000

95,000

Finished

goods

150,000

140,000

Purchase

of raw material during the

period Rs. 200,000

Paid

to labour Rs. 180,000 out of

which Rs. 150,000 used on

production.

Other

production costs Rs.

50,000

O/S

100,000

Raw

Material Account

114

Financial

Accounting (Mgt-101)

VU

Purch.

200,000

WIP

215,000

Labour

Account

C/S

85,000

Cost

180,000

Charge

150,000

Total

300,000

Total

300,000

Total

180,000

Total

180,000

Work

in Process Account

Other

Costs Account

O/B

90,000

Paid

50,000

Charge

50,000

Raw

M

215,000

Labour

150,000

F/G

410,000

O/H

50,000

C/B

95,000

Total

505,000

Total

505,000

Total

50,000

Total

50,000

Cost

of goods sold

Finished

Goods Stock Account

F/G

420000

O/S

150,000

COS

420,000

WIP

410,000

C/S

140,000

Total

560,000

Total

460,000

ILLUSTRATION

# 1

Record

the following transactions

· Purchased

goods for cash Rs,

10,000

· Purchased

goods from Ali Brothers.

worth of Rs. 20,000

· Sold

goods having cost of

Rs.15,000

· Returned

goods to Ali Brothers. worth of

Rs. 4,000

· Sold

goods having cost of Rs.

5,000

· Paid

to Ali Brothers. Rs.

10,000.

Also

ascertain

· Cost

of goods sold.

· Value

of closing stock.

· Payable

to Ali Brothers.

115

Financial

Accounting (Mgt-101)

VU

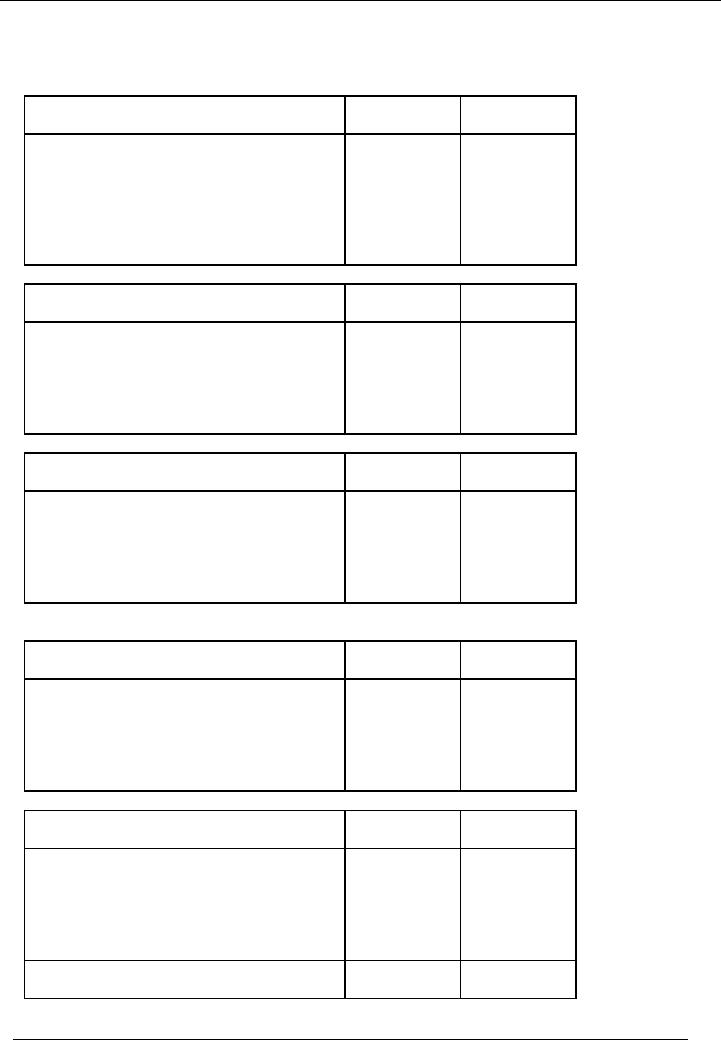

SOLUTION

First, we

will pass journal

entries

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Stock

Account

10,000

Cash

Account

10,000

Goods

purchased for cash

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Stock

Account

20,000

Ali

Brothers.

20,000

Goods

purchased from Ali

Brothers.

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Cost

of goods sold

15,000

Stock

Account

15,000

Goods

sold whose cost was

Rs. 15,000

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Ali

Brothers.

4,000

Stock

Account

4,000

Goods

returned to Ali Brothers.

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

Cost

of goods sold

5,000

Stock

Account

5,000

Goods

sold whose cost was

Rs. 5,000

Particulars

Amount(Dr.)

Amount(Cr.)

Rs.

Rs.

116

Financial

Accounting (Mgt-101)

VU

Ali

Brothers. Account

10,000

Cash

Account

10,000

Paid

to Ali Brothers.

PAYABLE

TO ALI BROTHERS

Ali

Brothers Account

Date

Particulars

Code

Amount

Date

Particulars

Code

Amount

#

Rs.

(Dr.)

#

Rs.

(Cr.)

Goods

returned

4,000

Purchased

goods

20,000

Paid

cash

10,000

BALANCE

6,000

Total

20,000

Total

20,000

COST

OF GOODS SOLD

Cost

of goods sold

Account

Date

Particulars

Code

Amount Date

Particulars

Code

Amount

#

Rs.

(Dr.)

#

Rs.

(Cr.)

Goods

sold

15,000

Goods

sold

5,000

BALANCE

20,000

Total

20,000

Total

20,000

VALUE OF

CLOSING STOCK

Stock

Account

Date

Particulars

Code

Amount

Date

Particulars

Code

Amount

#

Rs.

(Dr.)

#

Rs.

(Cr.)

Purchased

10,000

Goods

sold

15,000

goods

for cash

Returned

to

Ali

4,000

Purchased

20,000

Brothers

goods

from Ali

Goods

sold

5,000

Brothers.

BALANCE

6,000

Total

30,000

Total

30,000

ILLUSTRATION

# 2

·

Using the

following data calculate the

Cost of Goods Sold of XYZ

Co.

Stock

levels

Opening

Rs.

Closing

Rs.

Raw

material

100,000

85,000

117

Financial

Accounting (Mgt-101)

VU

Work

in process

90,000

95,000

Finished

goods

150,000

140,000

o Purchase

of raw material during the

period Rs. 200,000

o Paid

to labour Rs. 180,000 out of

which Rs. 150,000 used on

production.

o Other

production costs Rs.

50,000

SOLUTION

Labour

Account

Raw

Material Stock

Account

Debit

Credit

Debit

Credit

O/S

100,000

Cost

180,000Charged

150,000

Purchases

200,000

WIP

215,000

C/S

85,000

300,000

Total

180,000Total

180,000

Total

300,000

Total

Other

Costs Account

Debit

Credit

Paid

50,000

Charge

50,000

Total

50,000

Total

50,000

118

Financial

Accounting (Mgt-101)

VU

Work

in Process Account

Debit

Credit

O/B

90,000

Raw

M

215,000

Labor

150,000

F/G

410,000

O/H

50,000

C/B

95,000

Total

505,000

Total

505,000

Finished

Goods Stock

Account

Debit

Credit

O/S

150,000

COS

420,000

WIP

410,000

C/S

140,000

Total

560,000

Total

560,000

Cost

of Goods Sold

Account

Debit

Credit

F/G

420,000

·

In the

Raw Material Account, the

debit side contains:

o Opening

balance

100,000

o Purchases

200,000

·

On the credit

side, closing balance of Rs.

85,000 is shown along with the

balancing figure of Rs.

215,000

which

is charged to work in process OR

WIP account through the

following entry:

Debit:

Work

in process OR WIP

Account

Credit:

Raw

Material Account

·

Labour

cost of Rs. 180,000 is given,

out of which Rs. 150,000 is

charged to production. (Remaining

cost

of Rs.

30,000 will be explained in some later

stage). That means Rs.

150,000 are charged to work

in

process

OR WIP account through the

following entry:

Debit:

Work

in process OR WIP

Account

Credit:

Labour

Cost Account

119

Financial

Accounting (Mgt-101)

VU

·

Other

costs of Rs. 50,000 is also

charged to work in process OR

WIP account through the

following

entry:

Debit:

Work

in process OR WIP

Account

Credit:

Other

Costs Account

·

Work

in process account has the

opening balance of Rs.

90,000 and closing balance

of Rs. 95,000. After

charging

all the above mentioned accounts to

WIP. Balancing figure of

work in process of Rs.

410,000 is

charged

to finished goods account

through the following entry:

Debit:

Finished

Goods Account

Credit:

Work

in process Account

·

Finished

goods account has the

opening balance of Rs.

150,000 and closing balance

of Rs. 140,000.

After

charging WIP account to Finished

goods, the balancing figure of

Rs. 420,000, is charged to

cost of

goods

sold account through the

following entry:

Debit:

Cost

of Goods Sold Account

Credit:

Finished

Goods Account

120

Table of Contents:

- Introduction to Financial Accounting

- Basic Concepts of Business: capital, profit, budget

- Cash Accounting and Accrual Accounting

- Business entity, Single and double entry book-keeping, Debit and Credit

- Rules of Debit and Credit for Assets, Liabilities, Income and Expenses

- flow of transactions, books of accounts, General Ledger balance

- Cash book and bank book, Accounting Period, Trial Balance and its limitations

- Profit & Loss account from trial balance, Receipt & Payment, Income & Expenditure and Profit & Loss account

- Assets and Liabilities, Balance Sheet from trial balance

- Sample Transactions of a Company

- Sample Accounts of a Company

- THE ACCOUNTING EQUATION

- types of vouchers, Carrying forward the balance of an account

- ILLUSTRATIONS: Ccarrying Forward of Balances

- Opening Stock, Closing Stock

- COST OF GOODS SOLD STATEMENT

- DEPRECIATION

- GROUPINGS OF FIXED ASSETS

- CAPITAL WORK IN PROGRESS 1

- CAPITAL WORK IN PROGRESS 2

- REVALUATION OF FIXED ASSETS

- Banking transactions, Bank reconciliation statements

- RECAP

- Accounting Examples with Solutions

- RECORDING OF PROVISION FOR BAD DEBTS

- SUBSIDIARY BOOKS

- A PERSON IS BOTH DEBTOR AND CREDITOR

- RECTIFICATION OF ERROR

- STANDARD FORMAT OF PROFIT & LOSS ACCOUNT

- STANDARD FORMAT OF BALANCE SHEET

- DIFFERENT BUSINESS ENTITIES: Commercial, Non-commercial organizations

- SOLE PROPRIETORSHIP

- Financial Statements Of Manufacturing Concern

- Financial Statements of Partnership firms

- INTEREST ON CAPITAL AND DRAWINGS

- DISADVANTAGES OF A PARTNERSHIP FIRM

- SHARE CAPITAL

- STATEMENT OF CHANGES IN EQUITY

- Financial Statements of Limited Companies

- Financial Statements of Limited Companies

- CASH FLOW STATEMENT 1

- CASH FLOW STATEMENT 2

- FINANCIAL STATEMENTS OF LISTED, QUOTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES