|

Corporate

Finance FIN 622

VU

Lesson

21

CAPITAL

STRUCTURE & COST OF

EQUITY

MODIGLIANI

AND MILLER MODEL

The

following topics will be

discussed in this lecture.

Home

made leverage

Modigliani

& Miller Model

How

WACC remains

constant?

Business

& Financial Risk

M & M model

with taxes

1. Home

made leverage

An investor

can change the overall

financial leverage to which he is

exposed, by the use of

personal

borrowing

and investing it.

A

substitution of risks that

investors may undergo in order to move

from overpriced shares in

highly

levered

firms to those in un-levered firms by borrowing in

personal accounts.

Mainly

attributed to the Modigliani-Miller Theorem,

homemade leverage describes the

situation where

individuals

borrowing on the exact same

terms as large firms can duplicate

corporate leverage through

purchasing

and financing

options.

2.

Modigliani & Miller

Model

A financial

theory stating that the

market value of a firm is determined by

its earning power and the risk

of

its

underlying assets, and is independent of

the way it chooses to finance its

investments or distribute

dividends.

Remember, a firm can choose

between three methods of financing:

issuing shares,

borrowing

and

spending profits (as opposed

to dispersing them to shareholders in dividends).

The theorem gets

much

more complicated, but the

basic idea is that, under certain

assumptions, it makes no

difference

whether a

firm finances itself with

debt or equity.

Notes:

In

"Financial Innovations and

Market Volatility" Merton

Miller explains the concept

using the following

analogy:

"Think

of the firm as a gigantic tub of

whole milk. The farmer can

sell the whole milk as is.

Or he can

separate

out the cream and sell it at

a considerably higher price than the

whole milk would bring.

(That's the

analog

of a firm selling low-yield

and hence high-priced debt

securities.) But, of course, what the

farmer

would

have left would be skim

milk with low butterfat

content and that would

sell for much less

than whole

milk.

That corresponds to the levered equity.

The M and M proposition says

that if there were no costs

of

separation

(and, of course, no government dairy-support

programs), the cream plus the

skim milk would

bring

the same price as the whole

milk."

Modigliani-Miller

theorem

The

Modigliani-Miller

theorem forms the

basis for modern thinking on

capital structure. The

basic

theorem

states that, in the absence of taxes,

bankruptcy costs, and asymmetric

information and in an

efficient

market, the value of a firm is unaffected

by how that firm is

financed. It does not matter

if the

firm's

capital is raised by issuing

stock or selling debt. It does

not matter what the firm's dividend

policy is.

3.

How WACC remains

constant?

A calculation of a

firm's cost of capital in which

each category of capital is

proportionately weighted.

All

capital

sources - common stock, preferred stock,

bonds and any other

long-term debt - are included in

a

WACC

calculation.

WACC

is calculated by multiplying the cost of

each capital component by its

proportional weight and

then

summing:

Where:

69

Corporate

Finance FIN 622

VU

Re =

cost of equity

Rd =

cost of debt

E =

market value of the firm's equity

D =

market value of the firm's

debt

V=E+D

E/V =

percentage of financing that is

equity

D/V =

percentage of financing that is

debt

Tc - = corporate

tax rate

The

weight age average cost of

capital will be constant if the

proportionate of weight age of all

sources

remains

constant i.e. common stock, preferred

stock, bonds and any

other long term debt. And

also the

return

on common & preferred stock and

interest on debt remains constant,

then WACC remains

constant.

When

we talk about WACC remains

constant we actually mean

that any combination of debt

& equity from

100%

will not alter the overall

cost of capital. That means

that if you slice bread

into four pieces and

then

each

piece into two to make

total of eight pieces. Now

you have more pieces

but not more

bread.

CAPITAL

STRUCTURE

CURRENT

STATUS

COMBINATIONS

Rs.

Rs.

Rs.

Rs.

Rs.

ASSETS

6,000,000.00

6,000,000.00 6,000,000.00

6,000,000.00

6,000,000.00

DEBT

-

2,000,000.00

3,000,000.00 4,000,000.00

5,000,000.00

EQUITY

6,000,000.00

4,000,000.00 3,000,000.00

2,000,000.00

1,000,000.00

DEBT/EQUITY

RATIO

-

0.50

1.00

2.00

5.00

SHARE

PRICE

20.00

20.00

20.00

20.00

20.00

SHARES

OUTSTANDING

300,000.00

200,000.00

150,000.00

100,000.00

50,000.00

INTEREST

RATE

10.00

10.00

10.00

10.00

10.00

EBIT

800,000.00

800,000.00

800,000.00

800,000.00

800,000.00

ROE

13.33

15.00

16.67

20.00

30.00

EPS

2.67

4.00

5.33

8.00

16.00

WACC

13.33

13.33

13.33

13.33

13.33

What

we mean from 100% or bread in

above example corresponds to

total capitalization in the above

chart.

We

have various debt equity combinations in

above chart but the total

capitalization in every case is 6

million.

This is the basis of our

statement WACC remains

constant.

4.

Business & Financial

Risk

Business

Risk

Risk

associated with the unique circumstances

of a particular company, as they might affect the

price of that

company's

securities.

70

Corporate

Finance FIN 622

VU

Risks

can fester and spread

anywhere inside an organization. Many

are industry-specific, such as the

regulatory

concerns within financial services

and healthcare. Others are common to

all industries, such

as

supply

chain capacity, financial reporting

reliability, human resources

availability, and consumer

relationship

integrity.

Productivity specialist's help

you identify, prioritize,

and manage risks so that

you can enhance

performance

and ultimately, business

value.

Financial

Risk

· An

assessment of the possibility that a given investment

or loan will fail to bring a

return and may

result

in a loss of the original investment or

loan.

· The

risk that a company will not

have adequate cash flow to

meet financial obligations

· The

risk that an investment will be unable to

return profit to an investor.

5. M & M

Model with Taxes

A financial

theory stating that the

market value of a firm is determined by

its earning power and the risk

of

its

underlying assets, and is independent of

the way it chooses to finance its

investments or distribute

dividends.

Remember, a firm can choose

between three methods of financing:

issuing shares, borrowing

or

spending

profits (as opposed to

dispersing them to shareholders in dividends).

The theorem gets much

more

complicated, but the basic

idea is that, under certain assumptions,

it makes no difference whether a

firm

finances itself with debt or

equity.

Notes:

With

Taxes

Proposition

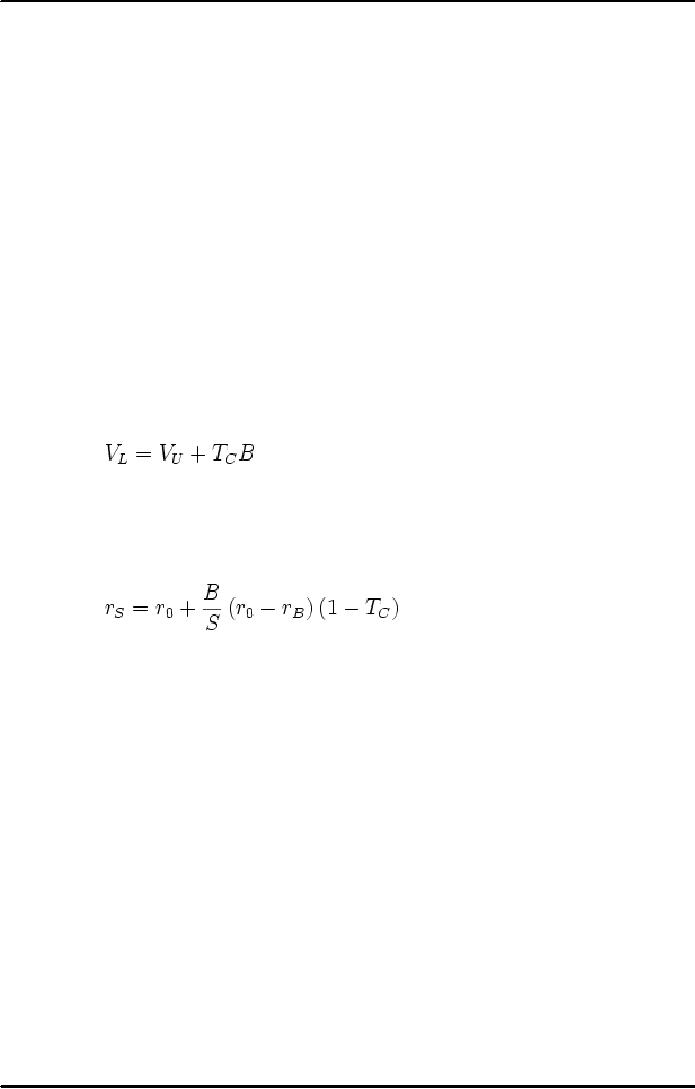

1:

· VL is the value of a levered

firm.

· VU is the value of an un-levered

firm.

· TCB is the tax rate(T_C) x the

value of debt (B)

This

means that there are

advantages for firms to be levered,

since corporations can deduct

interest

payments.

Therefore leverage lowers tax

payments. Dividend payments

are non-deductible.

Proposition

2:

· Rs - is the cost of

equity.

· r0 is the cost

of capital for an all equity

firm.

· rB is the cost of debt.

· B/S

-

is

the debt-to-equity

ratio.

· Tc - is the tax

rate.

The

same relationship as earlier described

stating that the cost of equity

rises with leverage, because

the risk

to

equity rises, still holds.

The formula however has implications

for the difference with the WACC.

The

following assumptions are made in

the propositions with

taxes:

· corporations

are taxed at the rate TC on

earnings after interest,

· no

transaction cost exist,

and

· individuals

and corporations borrow at the same

rate

· Debt

is for ever.

Concluding the

discussion, the after tax cash flow of

two identical firms in terms of EBIT

but having

different

capital structure debt equity

weight age will effect the value of

firm. This is because debt

in

capital

structure provides tax shield as interest

on debt is tax deductible expense. Thus

tax shield increases

the

value of firm: a levered

firm's value is greater than the

un-levered firm.

71

Table of Contents:

- INTRODUCTION TO SUBJECT

- COMPARISON OF FINANCIAL STATEMENTS

- TIME VALUE OF MONEY

- Discounted Cash Flow, Effective Annual Interest Bond Valuation - introduction

- Features of Bond, Coupon Interest, Face value, Coupon rate, Duration or maturity date

- TERM STRUCTURE OF INTEREST RATES

- COMMON STOCK VALUATION

- Capital Budgeting Definition and Process

- METHODS OF PROJECT EVALUATIONS, Net present value, Weighted Average Cost of Capital

- METHODS OF PROJECT EVALUATIONS 2

- METHODS OF PROJECT EVALUATIONS 3

- ADVANCE EVALUATION METHODS: Sensitivity analysis, Profitability analysis, Break even accounting, Break even - economic

- Economic Break Even, Operating Leverage, Capital Rationing, Hard & Soft Rationing, Single & Multi Period Rationing

- Single period, Multi-period capital rationing, Linear programming

- Risk and Uncertainty, Measuring risk, Variability of returnHistorical Return, Variance of return, Standard Deviation

- Portfolio and Diversification, Portfolio and Variance, RiskSystematic & Unsystematic, Beta Measure of systematic risk, Aggressive & defensive stocks

- Security Market Line, Capital Asset Pricing Model CAPM Calculating Over, Under valued stocks

- Cost of Capital & Capital Structure, Components of Capital, Cost of Equity, Estimating g or growth rate, Dividend growth model, Cost of Debt, Bonds, Cost of Preferred Stocks

- Venture Capital, Cost of Debt & Bond, Weighted average cost of debt, Tax and cost of debt, Cost of Loans & Leases, Overall cost of capital WACC, WACC & Capital Budgeting

- When to use WACC, Pure Play, Capital Structure and Financial Leverage

- Home made leverage, Modigliani & Miller Model, How WACC remains constant, Business & Financial Risk, M & M model with taxes

- Problems associated with high gearing, Bankruptcy costs, Optimal capital structure, Dividend policy

- Dividend and value of firm, Dividend relevance, Residual dividend policy, Financial planning process and control

- Budgeting process, Purpose, functions of budgets, Cash budgetsPreparation & interpretation

- Cash flow statement Direct method Indirect method, Working capital management, Cash and operating cycle

- Working capital management, Risk, Profitability and Liquidity - Working capital policies, Conservative, Aggressive, Moderate

- Classification of working capital, Current Assets Financing Hedging approach, Short term Vs long term financing

- Overtrading Indications & remedies, Cash management, Motives for Cash holding, Cash flow problems and remedies, Investing surplus cash

- Miller-Orr Model of cash management, Inventory management, Inventory costs, Economic order quantity, Reorder level, Discounts and EOQ

- Inventory cost Stock out cost, Economic Order Point, Just in time (JIT), Debtors Management, Credit Control Policy

- Cash discounts, Cost of discount, Shortening average collection period, Credit instrument, Analyzing credit policy, Revenue effect, Cost effect, Cost of debt o Probability of default

- Effects of discountsNot effecting volume, Extension of credit, Factoring, Management of creditors, Mergers & Acquisitions

- Synergies, Types of mergers, Why mergers fail, Merger process, Acquisition consideration

- Acquisition Consideration, Valuation of shares

- Assets Based Share Valuations, Hybrid Valuation methods, Procedure for public, private takeover

- Corporate Restructuring, Divestment, Purpose of divestment, Buyouts, Types of buyouts, Financial distress

- Sources of financial distress, Effects of financial distress, Reorganization

- Currency Risks, Transaction exposure, Translation exposure, Economic exposure

- Future payment situation hedging, Currency futures features, CF future payment in FCY

- CFfuture receipt in FCY, Forward contract vs. currency futures, Interest rate risk, Hedging against interest rate, Forward rate agreements, Decision rule

- Interest rate future, Prices in futures, Hedgingshort term interest rate (STIR), ScenarioBorrowing in ST and risk of rising interest, Scenariodeposit and risk of lowering interest rates on deposits, Options and Swaps, Features of opti

- FOREIGN EXCHANGE MARKETS OPTIONS

- Calculating financial benefitInterest rate Option, Interest rate caps and floor, Swaps, Interest rate swaps, Currency swaps

- Exchange rate determination, Purchasing power parity theory, PPP model, International fisher effect, Exchange rate system, Fixed, Floating

- FOREIGN INVESTMENT: Motives, International operations, Export, Branch, Subsidiary, Joint venture, Licensing agreements, Political risk