|

GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit) |

| << GROUP ACCOUNTS: Minority Interest, Inter Co. |

| Comprehensive Workings in Group Accounts Consolidated Balance Sheet >> |

Advance

Financial Accounting

(FIN-611)

VU

LESSON

# 44

GROUP

ACCOUNTS

Example

- [ Case vii ] Inter Co. Trading

(when there is unrealized

profit)

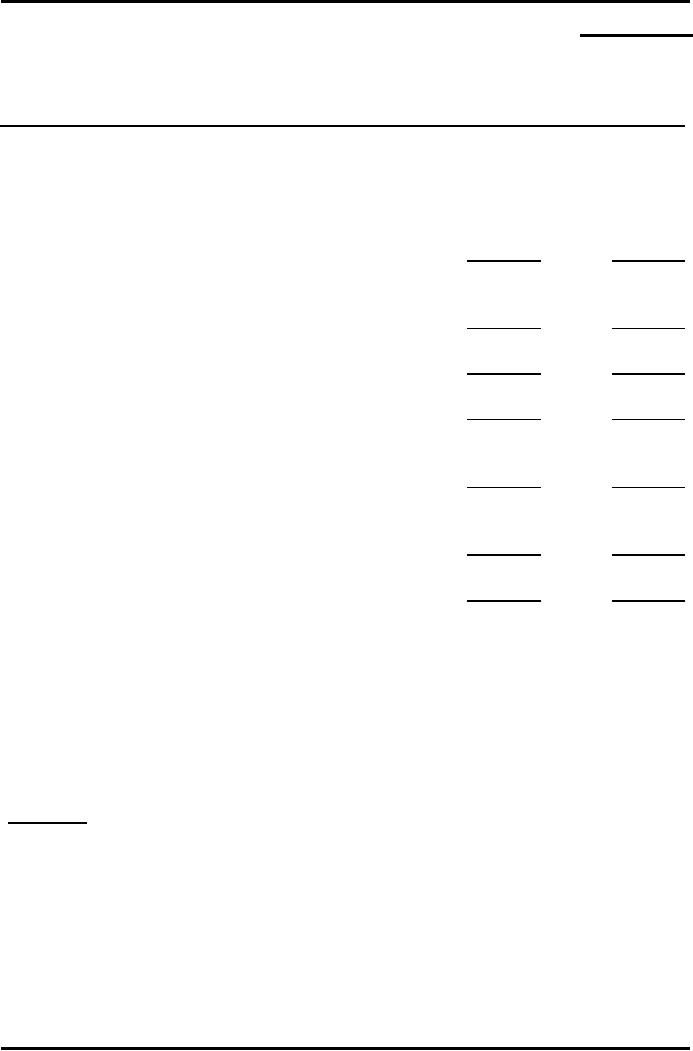

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

7,500

4,000

Cost

of Goods

Sold

(4,500)

(2,900)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Dividend

Income

100

1,300

500

Income

Tax

(520)

(200)

Net

Profit after

Tax

780

300

Ordinary

Dividend paid

(250)

(125)

530

175

Retained

Profits

b/f

1,000

450

Retained

Profits

c/f

1,530

625

The

Parent Co. (P) acquired

80% equity of the Subsidary

Co. (S) on 1st January

2003

for

Rs.1,700 when S's paid up

share capital was Rs.1,250

& it's reserves were

worth

Rs.50.

During the year S sold to P

goods costing Rs.1,000 &

selling price of

Rs.1,250

of which

inventory of Rs. 200 cost to P Co.

remained unsold. (Assume all

reserves

comprise

only of Retained Profits). Goodwill has

been impaired sofar.

Prepare

the Consolidated Income

Statement for the year

ended

Required:

31/12/2008.

Solution

- [ Case vii

]

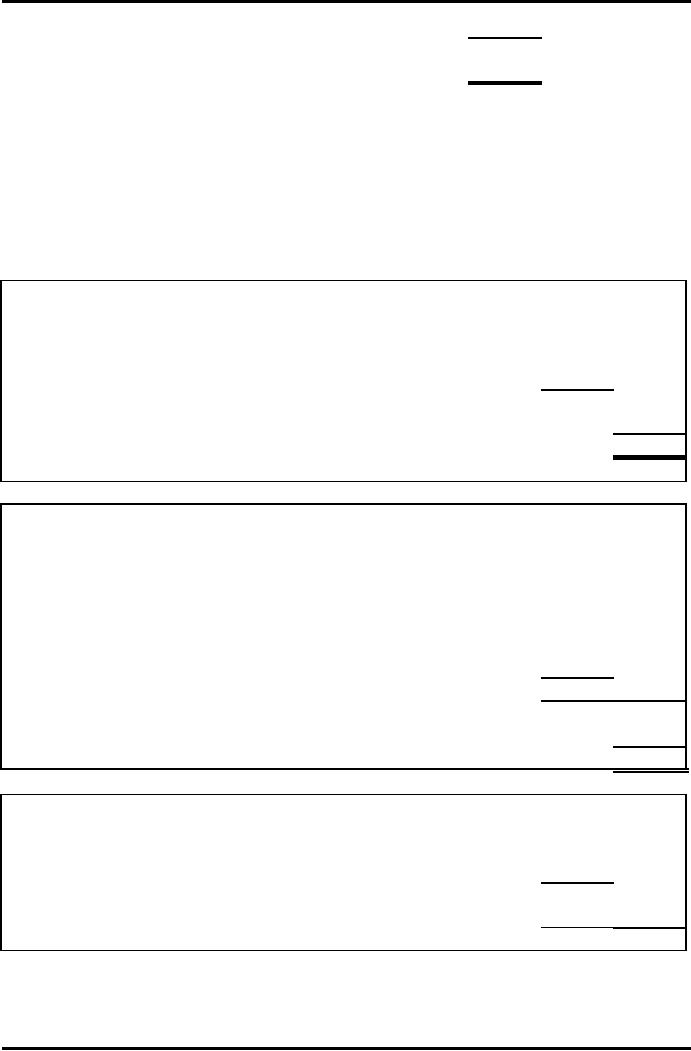

Inventory

of P Co represents purchases made

from S Co worth Rs. 200,

which from the

standpoint

of the group is above cost and

hence reflects unrealized

profit.

Profit

made by the S Co in the intera

group

transactio

Selling

price

1,250

100%

233

Advance

Financial Accounting

(FIN-611)

VU

Cost to

the S Co

(1,000)

profit

made by S

Co

250

20%

Unrealized

profit is the profit made by the S Co on

the stock remained

unsold

by P

Co

stock

at cost to the group is infact

selling price of the S Co.

therefore

the

%age of the profit is 20%.

Applying this %age on the

selling

price of

the unslod stock we get (200 x

20%) Rs. 40 of the

URP

Computation

of Goodwill

Rs.

Rs.

Cost of

Acquisition

1,700

Ordinary

Share Capital of S

80%

of Rs.1,250

1,000

Pre-acquisition

Retained Profits of S

80%

of Rs.50

40

(1,040)

660

Goodwill

totally impaired

(660)

0

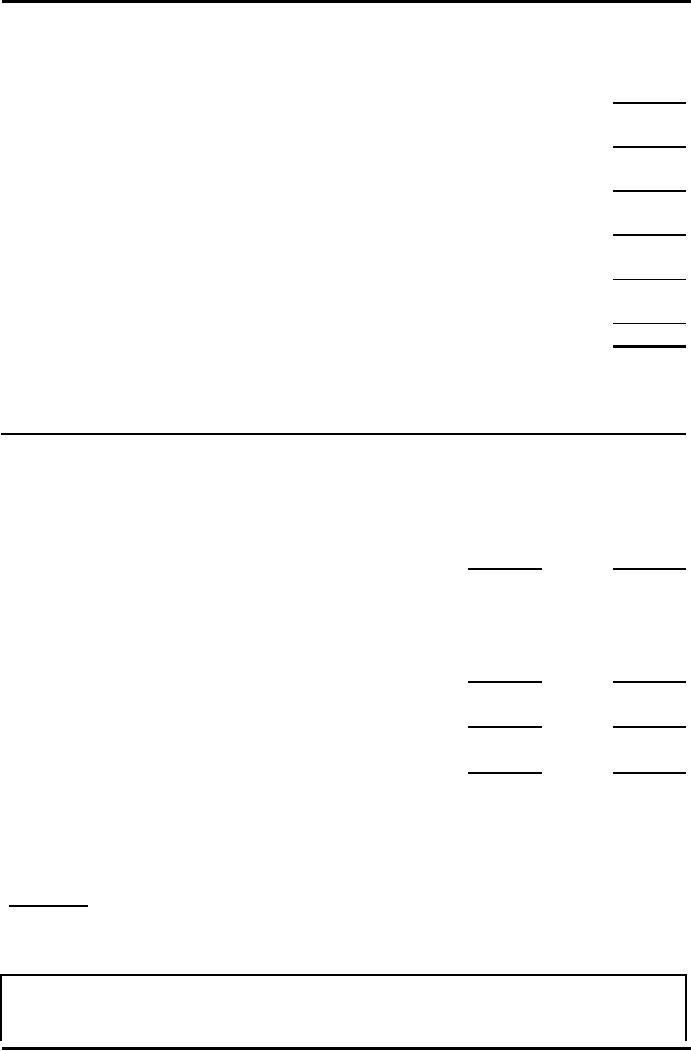

Computation

of opening balance of Group's Retained

Profits

Rs.

Rs.

Total

amount of opening balance of retained

profits of P Co

1,000

Post

acquisition part in opening balance of

retained profits of S Co

opening

balance of retained profits of

S

Co

450

pre-acquisition

retained

profits

-50

to the

extent of H% i.e.80%

400

320

Opening

balance of Group's Retained

Profits b/f

1,320

Goodwill

impairment loss

(660)

660

Computation

of Minority Interest

Rs.

Rs.

Profits

after tax of S

Co.

300

Unrealized

profit

-40

to the

extent of

MI%

260

52

Consolidated

Income Statement

For

the year ended 31st December

2008

234

Advance

Financial Accounting

(FIN-611)

VU

Rs.

(7,500+4,000-

Sales

1,250)

10,250

Cost of

Goods Sold

(4,500+2,900-1250+40)

(6,190)

Gross

Profit

4,060

Operating

Expenses

(2,400)

Profit

before tax

1,660

Income

Tax

(720)

Net

Profit after Tax

940

Minority

Interest

(52)

888

Dividend

Paid

(250)

638

Retained

Profits b/f

660

Retained

Profits c/f

1,298

Example

- [ Case viii ] During the Year

Acquisition of Wholly

Owned

Subsidiary

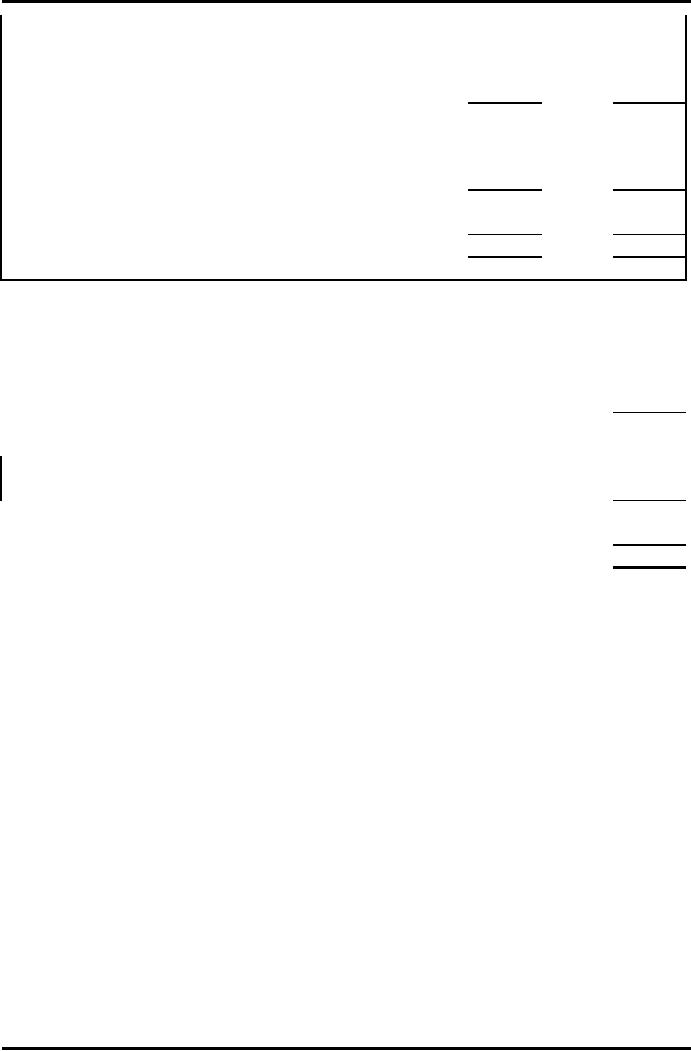

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

900

600

Cost

of Goods

Sold

(400)

(360)

Gross

Profit

500

240

Operating

Expenses

(200)

(48)

Selling

& Distribution

Expenses

(100)

(36)

Operating

Profit

200

156

Income

Tax

(90)

(72)

Net

Profit after

Tax

110

84

The

Parent Co. (P) acquired

100% equity of the Subsidary

Co. (S) on 30th

September

2008.

(Assume profits and losses

accrue evenly throughout the

year).

Prepare

the Consolidated Income

Statement for the year

ended

Required:

31/12/2008.

Solution

- [ Case viii ]

Income

Statement for the year ended

31st December 2008

12

3

months

months

235

Advance

Financial Accounting

(FIN-611)

VU

S

S

Rs.

Rs.

Sales

600

150

Cost of

Goods Sold

(360)

(90)

Gross

Profit

240

60

Operating

Expenses

(48)

(12)

Selling

& Distribution

Expenses

(36)

(9)

Operating

Profit

156

39

Income

Tax

(72)

(18)

Net

Profit after Tax

84

21

Consolidated

Income Statement

For

the year ended 31st December

2008

Rs.

Sales

(900+150)

1,050

Cost of

Goods Sold

(400+90)

(490)

Gross

Profit

560

Operating

Expenses

(200+12)

(212)

Selling

& Distribution

Expenses

(100+9)

(109)

Operating

Profit

239

Income

Tax

(90+18)

(108)

Net

Profit after Tax

131

236

Table of Contents:

- ACCOUNTING FOR INCOMPLETE RECORDS

- PRACTICING ACCOUNTING FOR INCOMPLETE RECORDS

- CONVERSION OF SINGLE ENTRY IN DOUBLE ENTRY ACCOUNTING SYSTEM

- SINGLE ENTRY CALCULATION OF MISSING INFORMATION

- SINGLE ENTRY CALCULATION OF MARKUP AND MARGIN

- ACCOUNTING SYSTEM IN NON-PROFIT ORGANIZATIONS

- NON-PROFIT ORGANIZATIONS

- PREPARATION OF FINANCIAL STATEMENTS OF NON-PROFIT ORGANIZATIONS FROM INCOMPLETE RECORDS

- DEPARTMENTAL ACCOUNTS 1

- DEPARTMENTAL ACCOUNTS 2

- BRANCH ACCOUNTING SYSTEMS

- BRANCH ACCOUNTING

- BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM

- STOCK AND DEBTORS SYSTEM

- INDEPENDENT BRANCH

- BRANCH ACCOUNTING 1

- BRANCH ACCOUNTING 2

- ESSENTIALS OF PARTNERSHIP

- Partnership Accounts Changes in partnership firm

- COMPANY ACCOUNTS 1

- COMPANY ACCOUNTS 2

- Problems Solving

- COMPANY ACCOUNTS

- RETURNS ON FINANCIAL SOURCES

- IASBS FRAMEWORK

- ELEMENTS OF FINANCIAL STATEMENTS

- EVENTS AFTER THE BALANCE SHEET DATE

- PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 1

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 2

- BORROWING COST

- EXCESS OF THE CARRYING AMOUNT OF THE QUALIFYING ASSET OVER RECOVERABLE AMOUNT

- EARNINGS PER SHARE

- Earnings per Share

- DILUTED EARNINGS PER SHARE

- GROUP ACCOUNTS

- Pre-acquisition Reserves

- GROUP ACCOUNTS: Minority Interest

- GROUP ACCOUNTS: Inter Company Trading (P to S)

- GROUP ACCOUNTS: Fair Value Adjustments

- GROUP ACCOUNTS: Pre-acquistion Profits, Dividends

- GROUP ACCOUNTS: Profit & Loss

- GROUP ACCOUNTS: Minority Interest, Inter Co.

- GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit)

- Comprehensive Workings in Group Accounts Consolidated Balance Sheet