|

Cost

& Management Accounting

(MGT-402)

VU

LESSON#

8

CONTROL

OVER MATERIAL

Control

over material is essential for

different reasons By and

large, materials are the

equivalent of

cash

and therefore pilfering and

theft may occur quite

often if effective control is

not exercised.

Prevention

of material from deterioration and

waste is also necessary. It is

also important to

eliminate

obsolete stocks with the

consequence easing of storage

space and storage

costs-

Moreover,

control over materials is

necessary to prevent extra expenditure on

excessive purchase

of

materials and improper use

of material. And above all, regular

supply of materials to

the

production

departments would help production on

schedule. It will also

ensure preparation of

accurate

statements of the value of material consumed by

each department/job and

final

statements

prepared according to their

needs.

From

the accounting point of

view, the following are

some important requirements of the

effective

material

control;

1.

That no material is purchased without

proper authority.

2.

That the quantity of material

purchased is in fact

received.

3.

That there are proper

storage facilities.

4.

That no material is issued without

proper authorization and the

purpose for which the

material

is required is recorded.

5.

That the accounts provide a

running balance of the value of

the materials on

hand.

Replenishment

of Stock

Materials

are received and issued by

the storekeeper to different

production departments. One

important

duty of a storekeeper is the restocking

of stores in order to ensure

efficient functioning

of

the stores department and

steady flow of materials to

the production departments. The

inflow

and

outflow of materials has to be

regulated in such a manner that

neither production is

adversely

effected

due to want of materials nor

there unnecessary blocking of

capital funds due to

overstocking

of raw materials.

This

implies that there is always a

limit to the minimum and

maximum quantity of materials

or

stock

in the store. The

storekeeper is to requisition for stock

for replenishment in time so as

to

ensure

honoring of requisition slips

from production departments.

Replenishment of stock

therefore

implies as `taking steps for

the fresh purchase of those

stocks which have been

exhausted

and

for which requisitions are to be

honored in future'.

In

order to ensure that the

optimum quantity of materials is

purchased and stock--neither

less nor

more,

the storekeeper applies scientific

techniques of materials management.

Fixing of certain

levels

for each item of materials

is one of such techniques.

The

following levels are generally

fixed.

1.

Order level.

2.

Maximum level.

3.

Minimum level.

4.

Danger level.

Order

Level

It

is also known as Re-ordering level in

relation with an item of stock. It is

the point at which it

becomes

essential to initiate purchase

orders for its fresh

supplies.

Normally,

re-ordering level is a point

between the maximum and

the minimum stock levels.

Fresh

orders

must be placed before the

actual stocks touch the

minimum level, so as to take

care of lapse

in

time the placing of the

order and the receipt of

materials in stores.

Following

are the factors that

are taken into account for

fixing re-order

level.

1.

The maximum

consumption.

50

Cost

& Management Accounting

(MGT-402)

VU

This

is the maximum quantity of

the material that is

expected

to be consumed in a day or in a week or in

a

month

time.

2.

Lead time.

This

is the estimated time period in

number of days or in

weeks

or in months, which is necessarily

required for

placing

an order and finally receiving it in

the stores.

There

might be different lead

times for different

consumptions.

For example; more time

will be required for

maximum

consumption comparing with the

time required

for

minimum or average

consumption.

3.

Economic order

quantity.

Details

of the economic order quantity

will be covered in

the

next lesson; here this

will be sufficient to learn that it

is

the

level where the ordering

quantity will be most

economical.

Although

EOQ is not required while calculating

the

order/re-order

level but one must keep in

mind the EOQ

of

the item for determining

the order level.

Most

of the times where purchases

are made according to

the

EOQ, the order level is

half or the EOQ.

Formula

Order

Level = Maximum Consumption x Lead Time

(maximum)

Maximum

Stock Level

The

maximum stock level indicates

the maximum quantity of an

item of material which can

be

held

in stock at any time. The maximum stock

level is fixed by taking into

consideration the

following

factors:--

1.

Minimum rates of

consumption.

This

is the minimum quantity of

the material that is

expected

to be consumed in a day or in a week or in

a

month

time.

2.

The lead time.

This

is the estimated time period in

number of days or in

weeks

or in months, which is necessarily

required for

placing

an order and finally receiving it in

the stores.

There

might be different lead

times for different

consumptions.

For example; more time

will be required for

maximum

consumption comparing with the

time required

for

minimum or average

consumption.

3.

Economic ordering

quantity.

Details

of the economic order quantity

will be covered in

the

next lesson; here this

will be sufficient to learn that it

is

the

level where the ordering

quantity will be most

economical.

4.

Availability of funds,

5.

Availability of storage

space.

6.

Risk of obsolescence, depletion,

evaporation and material waste,

7.

Future fluctuations of price of

materials.

8.

Cost of storage and

insurance.

9.

The nature of material--seasonal supplies

etc.

51

Cost

& Management Accounting

(MGT-402)

VU

10.

Any restrictions imposed by

the government or restrictions in

respect of import of

materials.

The

maximum stock can be calculated by

applying the following

formula.

Formula

Reorder

level (Minimum consumption

x Lead time) + EOQ

Putting

the formula elements of reorder

level over here the

result will be like

this:

(Maximum

consumption x Lead time) (Minimum

consumption x Lead time) + EOQ

[(Maximum

consumption - Minimum consumption) Lead

time]+ EOQ

Minimum

Level;

This

represents the quantity

below which the stock of any

item should not be allowed to

fall. In

other

words, an enterprise must

maintain minimum quantity of stock so

that the production is

not

adversely

affected due to non-availability of

materials.

The

minimum stock level is fixed by taking

into account:

1.

Re-order level.

2.

Lead time.

This

is the estimated time period in

number of days or in

weeks

or

in months, which is necessarily required

for placing an order

and

finally receiving it in the

stores.

There

might be different lead

times for different

consumptions.

For

example; more time will be

required for maximum

consumption

comparing with the time required

for minimum

or

average consumption.

3.

Average rate of

consumption.

This

is the minimum quantity of

the material that is expected

to

be

consumed in a day or in a week or in a

month time.

Formula

Reorder

level-- (Average consumption

x lead time)

Putting

the formula elements of reorder

level over here the

result will be like

this:

(Maximum

Consumption Average Consumption) x Lead

time

Danger

Level

The

danger level is below the

minimum level and represents

a stage where immediate steps

are

taken

for getting stock replenished. When

the stock reaches danger

level it is indicative that if no

emergency

steps are taken to restock the

materials, the stores will

be completely exhausted

and

normal

production stopped. Generally,

the danger level of stock is

fixed above the minimum

level.

The

danger stock level is fixed by taking

into account:

1.

Average Consumption.

2.

Emergency Lead Time.

Formula

Average

consumption x Emergency time

PRACTICE

QUESTIONS

Q.

1

Following

is the information provided by

the concerned departments about two

components

FRAME

and VASE regarding their

replenishment and

usage:

Minimum

usage

25

units per week

each

Maximum

usage

75

units per week

each

Average

usage

50

units per week

each

52

Cost

& Management Accounting

(MGT-402)

VU

Re-order

quantity

Frame

300

units

Vase

500

units

Re-order

period

Frame

4

to 6 weeks

Vase

2

to 4 weeks

Emergency

lead time

Frame

2

weeks

Vase

1

week

Calculate

for each

component:

1.

Re-order

level,

2.

Maximum

stock level, and

3.

Minimum

stock level,

4.

Danger

stock level.

Solution

Re-order

level:

Maximum

consumption x Lead Time

[maximum]

Frame

75x6

450

units

Vase

75x4

300

units

Maximum

stock level:

Reorder

level (Minimum consumption

x Lead time [minimum]) +

EOQ

Frame

450

+ 300 (25 X4)

650

units

Vase

300

+ 500 (25x2)

750

units

Minimum

stock level:

Reorder

level (Average consumption

x lead time [Average])

Average

lead time = Maximum +

Minimum

2

Frame

450

(50X5)

200

units

Vase

300

(50X3)

150

units

Danger

stock level:

Average

consumption x Emergency lead time

Frame

50

x 2

100

units

Vase

50

x 1

50

units

Q.

2

From

the following information

calculate the Maximum stock

level, Minimum stock

level,

Re-ordering

level and Danger stock

level;-

(a)

Average consumption

330

units per day

(b)

Maximum consumption

420

units per day

(c)

Minimum consumption

240

units per day

(d)

Re-order quantity

3,600

units

(e)

Re-order

period

10

to 15 days

(f)

Emergency Re-order period 12 days

Solution

:

Re-ordering

level:

Maximum

consumption x Lead Time

[maximum]

420x15

6,300

units.

53

Cost

& Management Accounting

(MGT-402)

VU

Maximum

stock level:

Reorder

level (Minimum consumption

x Lead time [minimum]) +

EOQ

6,300

(240 x 10) +

3,600

7,500

units

Minimum

stock level:

Reorder

level (Average consumption

x lead time [Average])

Average

lead time

=

Maximum + Minimum =15+10

=12.5

2

2

6,300

- 330 x 12.5

2,175

units

Danger

stock level:

Average

consumption x Emergency lead time

330

x 12

3,960

units

PROBLEMS

Q.

1

From

the following particulars, calculate:

--

Re-order

level, Minimum level,

Maximum level, and Danger

level.

Average

usage

400

units per day

Minimum

usage

60

units per day

Maximum

usage

130

units per day

Economic

order quantity

5000

units

Re-order

period

25

to 30 days

Q.

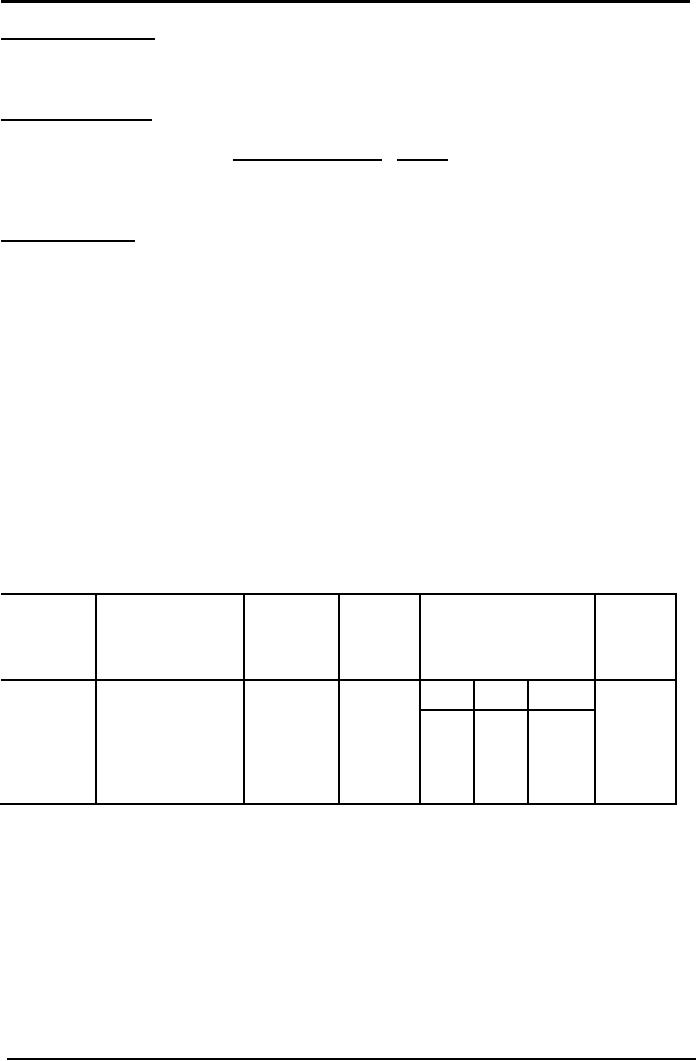

2

In

manufacturing its Products, a Company

uses three raw materials. A, B

and C, in respect of

which

the following apply:

Raw

Usage

per unit of

Re-order

Price

Delivery

Period

Re-order

material

Product

Quantity

Per

kg.

level

kg,

kg.

kg.

Min

Avg

Max

A

10

10,000

0.10

1

2

3

8,000

B

4

5,000

0.30

3

4

5

4,750

C

6

10,000

0.15

2

3

4

2,000

Weekly

production varies from 175

to 225 units, averaging 200

units.

What

would you expect the

quantities of the following to

be:

(a)

Minimum

stock of A

(b)

Maximum

stock of B

(c)

Re-order level of C

(d)

Danger stock

level of A

Q.

3

Two

components of A and B are

used as follows:--

Normal

usage

50

units per week

each

Minimum

usage

25

units per week

each

54

Cost

& Management Accounting

(MGT-402)

VU

Maximum

usage

75

units per week

each

Re-order

quantity--A : 400 units ; B :

600 units.

Re-order

period-- A : 4 to 6 weeks : B : 2 to 4

weeks.

Calculate

for each component;

(a)

Re-order level

(b)

Minimum level

(c)

Maximum level

(d)

Danger stock level.

Q.

4

What

do you understand by maximum stock level,

minimum stock level, and reorder

level?

Calculate

the above from the

following data:

Re-order

quantity

1,500

units

Re-order

period

4

to 6

weeks

Maximum

consumption 400 units per

week

Average

consumption

30

units per week

Minimum

consumption 250 units per

week

Q.

5

The

following information is available in

respect of component

FS-6:

Maximum

stock level

8,400

units

Budgeted

consumptions:

Maximum

1,500

units per month

Minimum

800

units per month

Estimated

delivery period

Maximum

4

months

Minimum

2

months

You

are required to calculate:

(i)

Re-order

level

(ii)

Economic

Order Quantity

55

Table of Contents:

- COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION:COST CLASSIFICATION,

- IMPORTANT TERMINOLOGIES:Cost Center, Profit Centre, Differential Cost or Incremental cost

- FINANCIAL STATEMENTS:Inventory, Direct Material Consumed, Total Factory Cost

- FINANCIAL STATEMENTS:Adjustment in the Entire Production, Adjustment in the Income Statement

- PROBLEMS IN PREPARATION OF FINANCIAL STATEMENTS:Gross Profit Margin Rate, Net Profit Ratio

- MORE ABOUT PREPARATION OF FINANCIAL STATEMENTS:Conversion Cost

- MATERIAL:Inventory, Perpetual Inventory System, Weighted Average Method (W.Avg)

- CONTROL OVER MATERIAL:Order Level, Maximum Stock Level, Danger Level

- ECONOMIC ORDERING QUANTITY:EOQ Graph, PROBLEMS

- ACCOUNTING FOR LOSSES:Spoiled output, Accounting treatment, Inventory Turnover Ratio

- LABOR:Direct Labor Cost, Mechanical Methods, MAKING PAYMENTS TO EMPLOYEES

- PAYROLL AND INCENTIVES:Systems of Wages, Premium Plans

- PIECE RATE BASE PREMIUM PLANS:Suitability of Piece Rate System, GROUP BONUS SYSTEMS

- LABOR TURNOVER AND LABOR EFFICIENCY RATIOS & FACTORY OVERHEAD COST

- ALLOCATION AND APPORTIONMENT OF FOH COST

- FACTORY OVERHEAD COST:Marketing, Research and development

- FACTORY OVERHEAD COST:Spending Variance, Capacity/Volume Variance

- JOB ORDER COSTING SYSTEM:Direct Materials, Direct Labor, Factory Overhead

- PROCESS COSTING SYSTEM:Data Collection, Cost of Completed Output

- PROCESS COSTING SYSTEM:Cost of Production Report, Quantity Schedule

- PROCESS COSTING SYSTEM:Normal Loss at the End of Process

- PROCESS COSTING SYSTEM:PRACTICE QUESTION

- PROCESS COSTING SYSTEM:Partially-processed units, Equivalent units

- PROCESS COSTING SYSTEM:Weighted average method, Cost of Production Report

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Accounting for joint products

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Problems of common costs

- MARGINAL AND ABSORPTION COSTING:Contribution Margin, Marginal cost per unit

- MARGINAL AND ABSORPTION COSTING:Contribution and profit

- COST VOLUME PROFIT ANALYSIS:Contribution Margin Approach & CVP Analysis

- COST VOLUME PROFIT ANALYSIS:Target Contribution Margin

- BREAK EVEN ANALYSIS MARGIN OF SAFETY:Margin of Safety (MOS), Using Budget profit

- BREAKEVEN ANALYSIS CHARTS AND GRAPHS:Usefulness of charts

- WHAT IS A BUDGET?:Budgetary control, Making a Forecast, Preparing budgets

- Production & Sales Budget:Rolling budget, Sales budget

- Production & Sales Budget:Illustration 1, Production budget

- FLEXIBLE BUDGET:Capacity and volume, Theoretical Capacity

- FLEXIBLE BUDGET:ANALYSIS OF COST BEHAVIOR, Fixed Expenses

- TYPES OF BUDGET:Format of Cash Budget,

- Complex Cash Budget & Flexible Budget:Comparing actual with original budget

- FLEXIBLE & ZERO BASE BUDGETING:Efficiency Ratio, Performance budgeting

- DECISION MAKING IN MANAGEMENT ACCOUNTING:Spare capacity costs, Sunk cost

- DECISION MAKING:Size of fund, Income statement

- DECISION MAKING:Avoidable Costs, Non-Relevant Variable Costs, Absorbed Overhead

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS:MAKE OR BUY DECISIONS