|

COMMON –SIZE AND INDEX ANALYSIS |

| << Analysis of income statement and balance sheet: |

| ANALYSIS BY RATIOS >> |

Financial

Statement Analysis-FIN621

VU

Lesson-32

COMMON SIZE

AND INDEX

ANALYSIS

Method

used by interested parties such as investors,

creditors, and management to evaluate the

past,

current,

and projected conditions and performance of the

firm. Ratio analysis is the most common

form

of

financial analysis. It provides relative

measures of the firm's conditions and

performance. Horizontal

Analysis

and Vertical Analysis are

also popular forms.

Horizontal analysis is used to evaluate

the trend

in the

accounts over the years,

while vertical analysis, also

called a Common Size Financial

Statement

discloses

the internal structure of the firm. It indicates the

existing relationship between sales

and each

income

statement account. It shows the mix of

assets that produce income and

the mix of the sources

of

capital,

whether by current or long-term

debt or by equity funding.

When using the financial

ratios, a

financial

analyst makes two types of

comparisons:

(a) Industry

comparison. The

ratios of a firm are

compared with those of

similar firms or with

industry

averages

or norms to determine how the company is

faring relative to its competitors.

Industry average

ratios

are available from a number of

sources

(b)

Trend

analysis. A

firm's present ratio is

compared with its past and

expected future ratios to

determine

whether the company's financial

condition is improving or deteriorating

over time.

After

completing the financial statement

analysis, the firm's financial analyst

will consult with

management

to discuss plans and prospects, any

problem areas identified in the analysis,

and possible

solutions.

Given below is a list of

widely used financial

ratios.

2.

Trend

percentages/ Horizontal Analysis/

Index Analysis: This

analysis considers changes in

items of

financial statement from a

base year to the following

years to show the direction of

change.

This

is also called horizontal analysis. In

this, the figures of various

years are placed side by

side in

adjacent columns

in the form of comparative financial

statements.

3. Component

percentages/ Vertical Analysis/

Common- Size Analysis: This

type of analysis

indicates the

relative size of each item

in the Financial Statements as a

percentage of the total of

that

Statement

i.e. Total Assets or total

Liabilities & Shareholders equity in Balance

Sheet and Sales in

Income

Statement. Such a statement is

then called common-size

Financial Statement. This

type of

analysis

technique is also called

Vertical Analysis.

Vertical

Analysis

When

using vertical analysis, the analyst

calculates each item on a

single financial statement as

a

percentage

of a total. The term vertical

analysis applies

because each year's figures

are listed vertically

on a

financial statement. The

total used by the analyst on the

income statement is net sales

revenue,

while

on the balance sheet it is total assets.

This approach to financial statement

analysis, also known as

component

percentages,

produces common-size

financial statements. Common-size

balance sheets and

income

statements can be more easily

compared, whether across the

years for a single company

or

across

different companies

Financial

statement item that is used

as a base value. All other

accounts on the financial statement

are

compared

to it. In the balance sheet,

for example, total assets

equals 100%. Each asset is

stated as a

percentage

of total assets. Similarly,

total liabilities and stockholders'

equity are assigned 100%

with a

given

liability or equity account

stated as a percentage of the total

liabilities and stockholders'

equity.

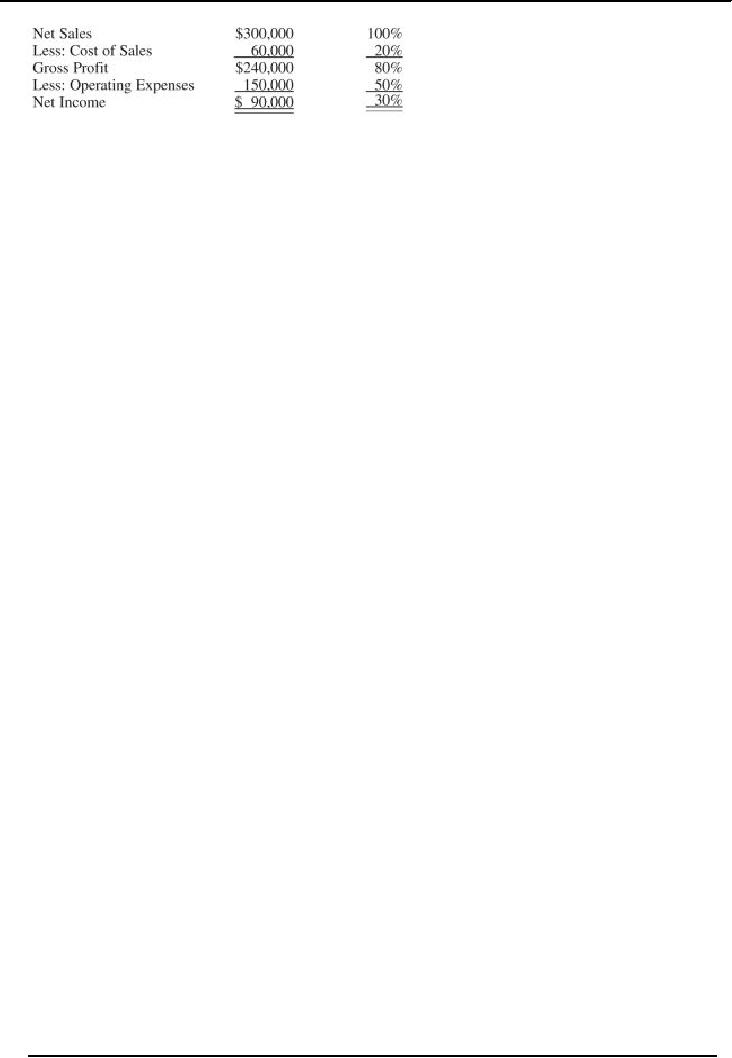

For

the income statement, 100% is

assigned to net sales with

all revenue and expense accounts

related to

it.

Under vertical analysis, the statements

showing the percentages are

referred to as Common Size

Financial

Statements. Common size percentages

can be compared from one

period to another to identify

areas

needing attention. An illustration

follows:

128

Financial

Statement Analysis-FIN621

VU

Horizontal

Analysis

When

an analyst compares financial

information for two or more

years for a single company,

the

process

is referred to as horizontal

analysis,

since the analyst is reading

across the page to compare

any

single

line item, such as sales

revenues. In addition to comparing

dollar amounts, the analyst

computes

percentage

changes from year to year

for all financial statement

balances, such as cash and

inventory.

Alternatively,

in comparing financial statements

for a number of years, the analyst

may prefer to use a

variation

of horizontal analysis called trend

analysis.

Trend analysis involves calculating

each year's

financial

statement balances as percentages of the

first year, also known as

the base year. When

expressed

as percentages, the base

year figures are always

100 percent, and percentage changes

from the

base

year can be

determined.

Time

series analysis of financial statements

covering more than one accounting

period; also called

Trend

Analysis. It looks at the percentage

change in an account over

time. The percentage

change

equals

the change over the prior

year. For example, if sales

in 20X0 are $100,000 and in

20X1 are

$300,000,

there is a 200% increase

($200,000/$100,000). By examining the

magnitude of direction of a

financial

statement item over time,

the analyst can evaluate its

reasonableness.

Common

Size Financial Statement

A company

financial statement that

displays all items as

percentages of a common base figure.

This

type

of financial statement allows

for easy analysis between companies or

between time periods of a

company.

129

Table of Contents:

- ACCOUNTING & ACCOUNTING PRINCIPLES

- Dual Aspect of Transactions

- Rules of Debit and Credit

- Steps in Accounting Cycle

- Preparing Balance Sheet from Trial Balance

- Business transactions

- Adjusting Entry to record Expenses on Fixed Assets

- Preparing Financial Statements

- Closing entries in Accounting Cycle

- Income Statement

- Balance Sheet

- Cash Flow Statement

- Preparing Cash Flows

- Additional Information (AI)

- Cash flow from Operating Activities

- Operating Activities’ portion of cash flow statement

- Cash flow from financing Activities

- Notes to Financial Statements

- Charging Costs of Inventory to Income Statement

- First-in-First - out (FIFO), Last-in-First-Out (LIFO)

- Depreciation Accounting Policies

- Accelerated-Depreciation method

- Auditor’s Report, Opinion, Certificate

- Management Discussion & Analyses (MD&A)

- TYPES OF BUSINESS ORGANIZATIONS

- Incorporation of business

- Authorized Share Capital, Issued Share Capital

- Book Values of equity, share

- SUMMARY

- SUMMARY

- Analysis of income statement and balance sheet:

- COMMON –SIZE AND INDEX ANALYSIS

- ANALYSIS BY RATIOS

- ACTIVITY RATIOS

- Liquidity of Receivables

- LEVERAGE, DEBT RATIOS

- PROFITABILITY RATIOS

- Analysis by Preferred Stockholders

- Efficiency of operating cycle, process

- STOCKHOLDERS’ EQUITY SECTION OF THE BALANCE SHEET 1

- STOCKHOLDERS’ EQUITY SECTION OF THE BALANCE SHEET 2

- BALANCE SHEET AND INCOME STATEMENT RATIOS

- Financial Consultation Case Study

- ANALYSIS OF BALANCE SHEET & INCOME STATEMENT

- SUMMARY OF FINDGINS