|

CAPITAL WORK IN PROGRESS 2 |

| << CAPITAL WORK IN PROGRESS 1 |

| REVALUATION OF FIXED ASSETS >> |

Financial

Accounting (Mgt-101)

VU

Lesson-20

CAPITAL

WORK IN PROGRESS

If an

asset is not completed at

that time when balance sheet

is prepared, all costs incurred on

that asset up to

the

balance sheet date are

transferred to an account called

Capital

Work in Progress Account.

This

account

is shown separately in the balance

sheet below the fixed asset.

Capital work in progress

account

contains

all expenses incurred on the asset

until it is converted into working

condition. All these

expenses

will

become part of the cost of

that asset. When any

expense is incurred or paid, it is included in the

Capital

Work

in Progress Account through the

following entry:

Debit:

Work

in Progress Account

Credit:

Cash/Bank/Payable

Account

When

an asset is completed and it is

ready to work, all costs

will transfer to the relevant asset

account

through

the following entry:

Debit:

Relevant

asset account

Credit:

Capital

work in progress

account

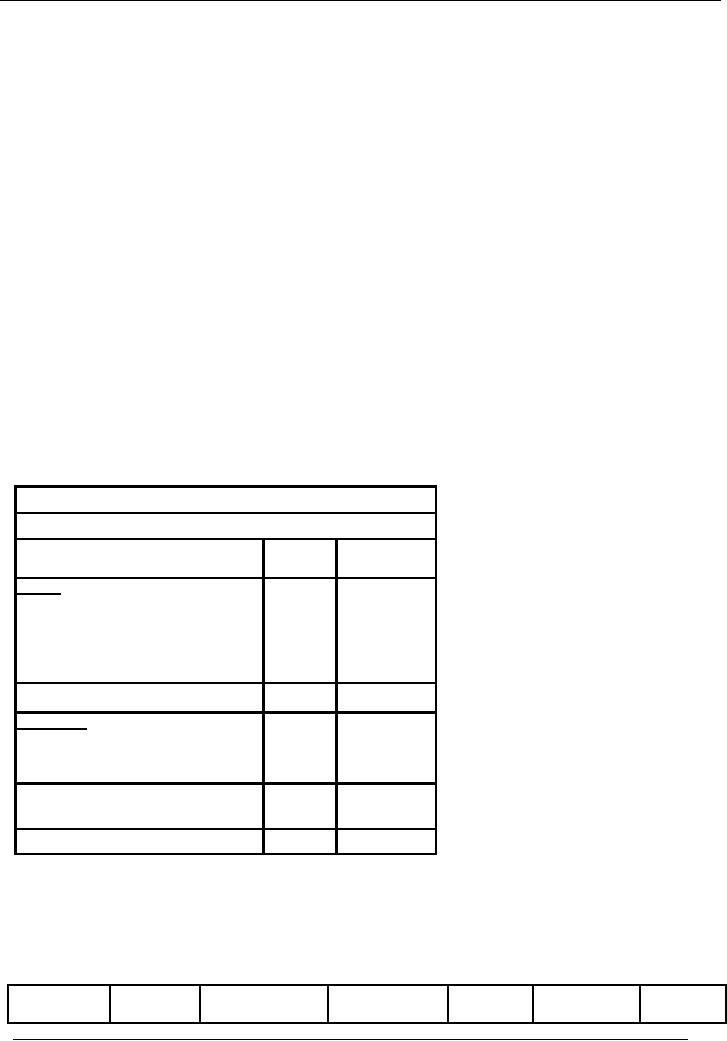

PRESENTATION

It is

already mentioned that Work in

Progress Account is shown

separately in the balance sheet

below the

fixed

asset. i-e.

Name of the

Entity

Balance

Sheet As At

Particulars

Amount

Amount

Rs.

Rs.

Assets

Fixed

Assets

xyz

Capital

Work in Progress

xyz

Other

Long Term Assets

xyz

Current

Assets

Total

Xyz

Liabilities

Capital

xyz

Profit

xyz

Xyz

Long

Term Liabilities

Xyz

Current

Liabilities

Total

Xyz

Consider

the solved illustration in the previous

lecture:

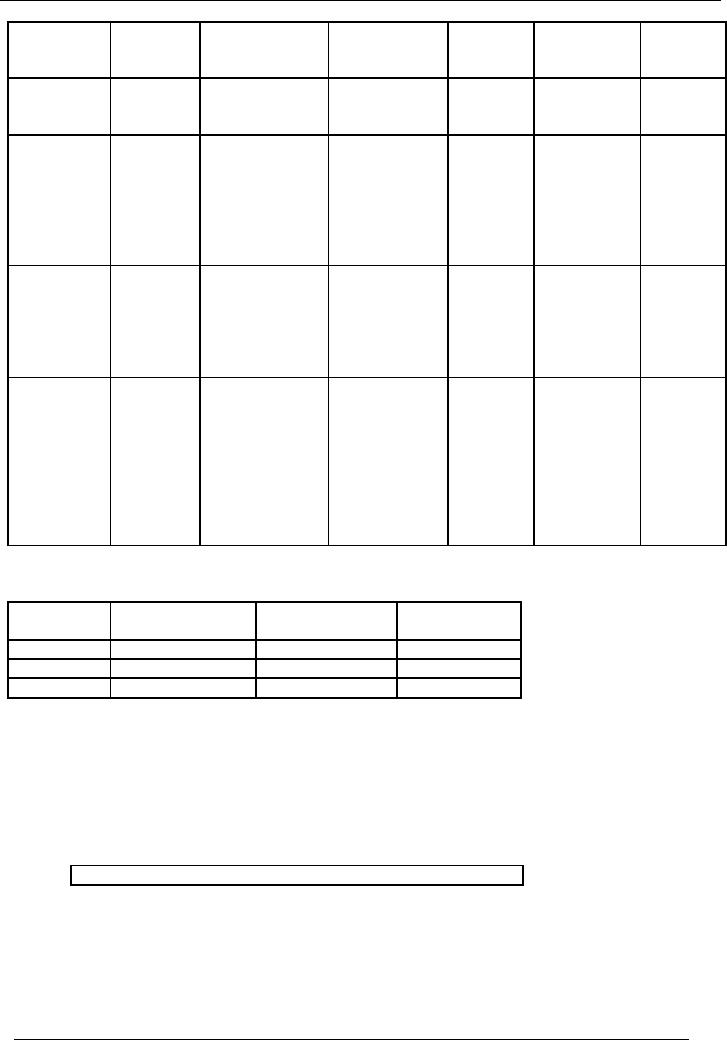

Depreciation

on the basis of

use

Date

Purchase

Depreciation

Accumulated

Total

Written

Total

of

(Rs.)

depreciation

Accum.

Down

Value

Written

144

Financial

Accounting (Mgt-101)

VU

machine

(Rs.)

Dep.

(Rs.)

Down

(Rs.)

Value

(Rs.)

01-09-2000

100,000

Machine # 1

Machine

# 1

20,833

Machine # 1

79,167

100,000

x 25%

20,833

79,167

x10/12=20,833

2001-2002

Machine

# 1

Machine

# 1

61,458

Machine # 1

238,542

79,167x25%

40,625

59,375

= 19,792

31-01-2002

200,000

Machine # 2

Machine

# 2

Machine

# 2

200,000x25%x5/

20,833

179,167

12=20,833

2002-2003

Machine

# 1

Machine

# 1

121,094

Machine # 1

178,906

59,375x25%

55,469

44,531

= 14,844

Machine

# 2

Machine

# 2

Machine

# 2

179,167x25%

65,625

134,375

=44,792

2003-2004

Machine

# 1

Machine

# 1

175,538

Machine # 1

138,281

44,531x25%x

63,819

(36,181)

9/12=

8,350

(sold)

Machine

# 2

Machine

# 2

Machine

# 2

134,375x25%

99,219

100,781

= 33,594

01-07-2003

50,000

Machine # 3

Machine

# 3

Machine

# 3

50,000x25%

12,500

37,500

= 12,500

PRESENTATION

IN THE BALANCE SHEET

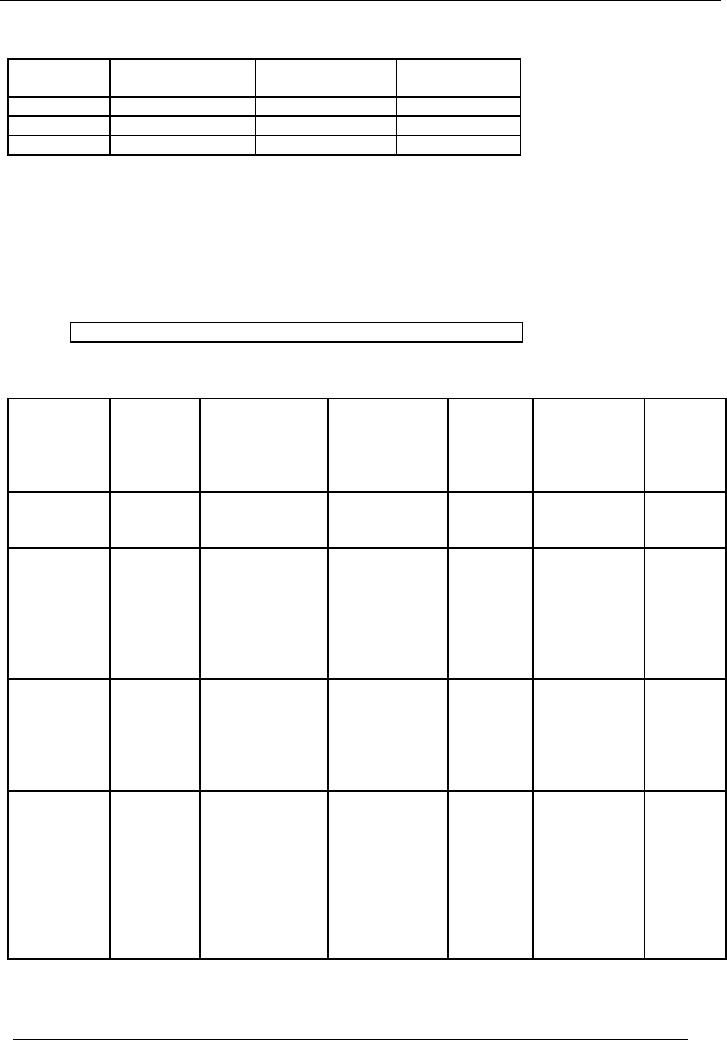

Year

Cost

of Machinery

Accumulated

Written

Down

Depreciation

Value

2000-2001

100,000

20,833

79,167

2001-2002

300,000

61,458

238,542

2002-2003

300,000

121,094

178,906

Written

Down Value of the year

2003-2004

Opening

Written Down Value:

Rs.

178,906

Add:

Cost of machine

purchased:

Rs.

50,000

Less:

Depreciation of Machine # 1 in

2003-2004:

(8,350)

Less:

Depreciation of other

assets:

(46,094)

Less:

Written Down Value of

machine disposed:

(36,181)

Closing

Written Down Value:

Rs.

138,281

145

Financial

Accounting (Mgt-101)

VU

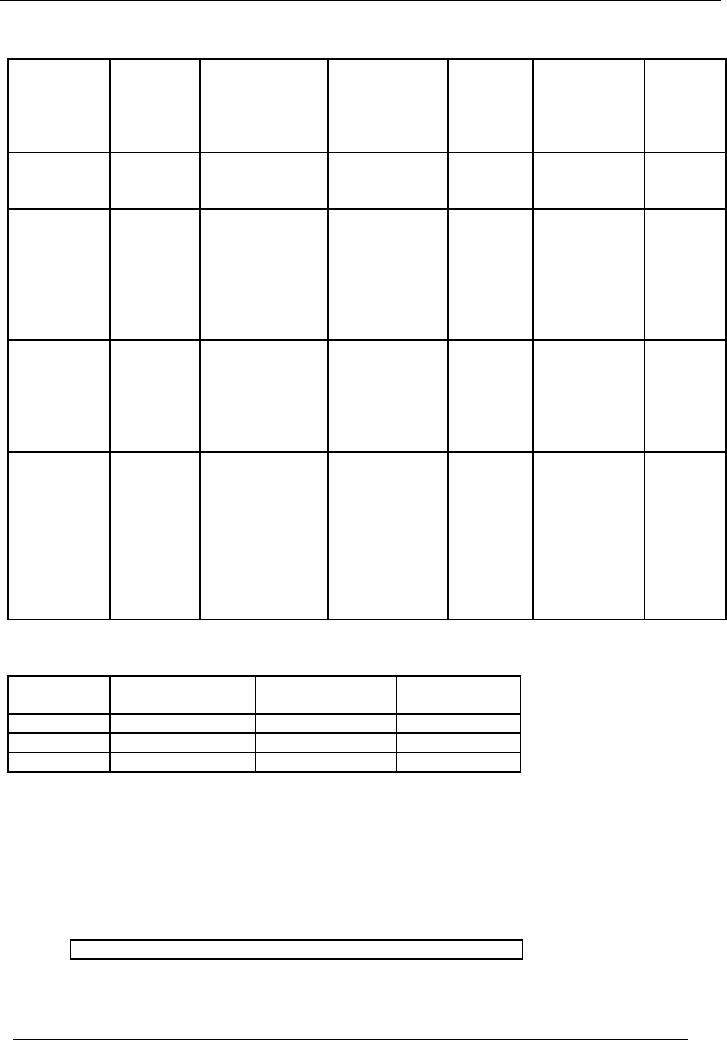

Full

year depreciation in the

year of purchase and no depreciation in

the year of sale:

Date

Purchase

Depreciation

Accumulated

Total

Written

Total

of

(Rs.)

depreciation

Accum.

Down

Value

Written

machine

(Rs.)

Dep.

(Rs.)

Down

(Rs.)

Value

(Rs.)

01-09-2000

100,000

Machine # 1

Machine

# 1

25,000

Machine # 1

75,000

100,000

x 25%

25,000

75,000

=25,000

2001-2002

Machine

# 1

Machine

# 1

93,750

Machine # 1

206,250

75,000x25%

43,750

56,250

= 18,750

31-01-2002

200,000

Machine # 2

Machine

# 2

Machine

# 2

200,000x25%

50,000

150,000

=50,000

2002-2003

Machine

# 1

Machine

# 1

145,313

Machine # 1

154,687

56,250x25%

57,813

42,187

= 14,063

Machine

# 2

Machine

# 2

Machine

# 2

150,000x25%

87,500

112,500

=37,500

2003-2004

Machine

# 1

Machine

# 1

185,935

Machine # 1

121,875

0

57,813

42,187

Machine

sold

(sold)

(sold)

Machine

# 2

Machine

# 2

Machine

# 2

112,500x25%

115,625

84,375

= 28,125

01-07-2003

50,000

Machine # 3

Machine

# 3

Machine

# 3

50,000x25%

12,500

37,500

= 12,500

PRESENTATION

IN THE BALANCE SHEET

Year

Cost

of Machinery

Accumulated

Written

Down

Depreciation

Value

2000-2001

100,000

25,000

75,000

2001-2002

300,000

93,750

206,250

2002-2003

300,000

145,313

154,687

Written

Down Value of the year

2003-2004

Opening

Written Down Value:

Rs.

154,687

Add:

Cost of machine

purchased:

Rs.

50,000

Less:

Depreciation of Machine # 1 in

2003-2004:

0

Less:

Depreciation of other

assets:

(40,625)

Less:

Written Down Value of

machine disposed:

(42,187)

Closing

Written Down Value:

Rs.

121,875

146

Financial

Accounting (Mgt-101)

VU

ILLUSTRATION

# 2

Following

information of machinery account is

available in Year 2004:

· Machine

# 1 is purchased on

August

1, 2000 for Rs.

50,000

· Machine

# 2 is purchased on April 1, 2002

for Rs. 100,000

· Machine

# 3 is purchased on March 1, 2004

for Rs. 150,000

· Machine

# 1 is disposed on May 31,

2004

Depreciation

is charged @ 20% reducing balance method.

Financial year is closed on June 30

every year.

Show

the calculation of depreciation on machinery for

four years using the

following policies:

· Depreciation

is charged on the basis of

use

· Full

depreciation is charged in the year of

purchase and no depreciation is charged

in the year of

disposal,

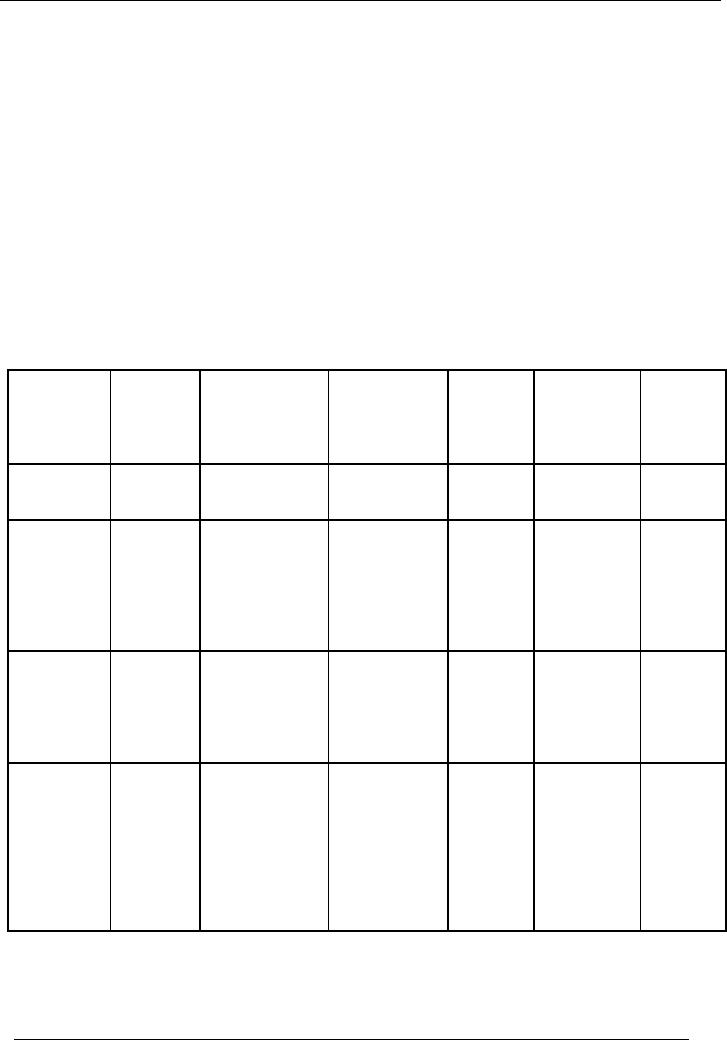

SOLUTION

Depreciation

on the basis of

use

Date

Purchase

Total

Depreciation

Accumulated

Total

Written

of

Down

Value

Written

(Rs.)

depreciation

Accum.

machine

(Rs.)

Down

Dep.

(Rs.)

(Rs.)

Value

(Rs.)

01-08-2000

50,000

Machine # 1

Machine

# 1

9,167

Machine # 1

40,833

50,000

x 20%

9,167

9,167

x11/12=9,167

2001-2002

Machine

# 1

Machine

# 1

22,334

Machine # 1

127,666

40,833x20%

17,334

32,666

= 8,167

Machine

# 2

01-04-2002

100,000

Machine # 2

5,000

Machine

# 2

100,000x20%x3/

95,000

12=5,000

2002-2003

Machine

# 1

Machine

# 1

47,867

Machine # 1

102,133

32,666x20%

23,867

26,133

= 6,533

Machine

# 2

Machine

# 2

Machine

# 2

95,000x20%

24,000

76,000

=19,000

2003-2004

Machine

# 1

Machine

# 1

77,858

Machine # 1

200,800

26,133x20%x

28,658

(21,342)

11/12=

4,791

(sold)

Machine

# 2

Machine

# 2

Machine

# 2

76,000x20%

39,200

60,800

= 15,200

01-03-2004

150,000

Machine # 3

Machine

# 3

Machine

# 3

150,000x20%x

10,000

140,000

4/12=

10,000

147

Financial

Accounting (Mgt-101)

VU

PRESENTATION

IN THE BALANCE SHEET

Year

Cost

of Machinery

Accumulated

Written

Down

Depreciation

Value

2000-2001

50,000

9,167

40,833

2001-2002

150,000

22,334

127,666

2002-2003

150,000

47,867

102,133

Written

Down Value of the year

2003-2004

Opening

Written Down Value:

Rs.

102,133

Add:

Cost of machine

purchased:

Rs.

150,000

Less:

Depreciation of Machine # 1 in

2003-2004:

(4,791)

Less:

Depreciation of other

assets:

(25,200)

Less:

Written Down Value of

machine disposed:

(21,342)

Closing

Written Down Value:

Rs.

200,800

Full

year depreciation in the

year of purchase and no depreciation in

the year of sale:

Date

Purchase

Depreciation

Accumulated

Total

Written

Total

of

(Rs.)

depreciation

Accum.

Down

Value

Written

machine

(Rs.)

Dep.

(Rs.)

Down

(Rs.)

Value

(Rs.)

01-08-2000

50,000

Machine # 1

Machine

# 1

10,000

Machine # 1

40,000

50,000

x 20%

10,000

40,000

=10,000

2001-2002

Machine

# 1

Machine

# 1

38,000

Machine # 1

112,000

40,000x20%

18,000

32,000

= 8,000

01-04-2002

100,000

Machine # 2

Machine

# 2

Machine

# 2

100,000x20%

20,000

80,000

=20,000

2002-2003

Machine

# 1

Machine

# 1

60,400

Machine # 1

89,600

32,000x20%

24,400

25,600

= 6,400

Machine

# 2

Machine

# 2

Machine

# 2

80,000x20%

36,000

64,000

=16,000

2003-2004

Machine

# 1

Machine

# 1

103,200

Machine # 1

171,200

0

24,400

(25,600)

Machine

sold

(sold)

(sold)

Machine

# 2

Machine

# 2

Machine

# 2

64,000x20%

48,800

51,200

= 12,800

01-03-2004

150,000

Machine # 3

Machine

# 3

Machine

# 3

150,000x20%

30,000

120,000

= 30,000

148

Financial

Accounting (Mgt-101)

VU

PRESENTATION

IN THE BALANCE SHEET

Year

Cost

of Machinery

Accumulated

Written

Down

Depreciation

Value

2000-2001

50,000

10,000

40,000

2001-2002

150,000

38,000

112,000

2002-2003

150,000

60,400

89,600

Written

Down Value of the year

2003-2004

Opening

Written Down Value:

Rs.

89,600

Add:

Cost of machine

purchased:

Rs.

150,000

Less:

Depreciation of Machine # 1 in

2003-2004:

0

Less:

Depreciation of other

assets:

(42,800)

Less:

Written Down Value of

machine disposed:

(25,600)

Closing

Written Down Value:

Rs.

171,200

REVALUATION

OF FIXED ASSETS

Fixed

assets are purchased to be

used for longer period. In the

subsequent years, the value of

asset could be

higher or

lower than its present

book value due to

inflationary condition of the economy.

Assets are valued

at

Historical Cost in the books of accounts.

Historical Cost is the original

cost of the asset at which it

was

purchased

plus additional costs incurred on the

asset to bring it in working

condition. Sometimes, the

management

of the business, if it thinks fit,

revalues the asset to present it on

current market value. Once

the

asset

is revalued to its market

value, then its value

has to be constantly monitored to reflect the

changes in

the

market value.

If an

asset is revalued at higher cost than

its original cost, the

excess amount will be treated as

profit on

revaluation of

fixed assets and it is

credited to Revaluation Reserve

Account.

On the

other hand, if an asset is

revalued at lower cost than

its original cost, the

balance amount will be

treated

as loss on revaluation of fixed assets

and it is shown in the profit &

loss account of that year in

which

asset

was revalued.

149

Table of Contents:

- Introduction to Financial Accounting

- Basic Concepts of Business: capital, profit, budget

- Cash Accounting and Accrual Accounting

- Business entity, Single and double entry book-keeping, Debit and Credit

- Rules of Debit and Credit for Assets, Liabilities, Income and Expenses

- flow of transactions, books of accounts, General Ledger balance

- Cash book and bank book, Accounting Period, Trial Balance and its limitations

- Profit & Loss account from trial balance, Receipt & Payment, Income & Expenditure and Profit & Loss account

- Assets and Liabilities, Balance Sheet from trial balance

- Sample Transactions of a Company

- Sample Accounts of a Company

- THE ACCOUNTING EQUATION

- types of vouchers, Carrying forward the balance of an account

- ILLUSTRATIONS: Ccarrying Forward of Balances

- Opening Stock, Closing Stock

- COST OF GOODS SOLD STATEMENT

- DEPRECIATION

- GROUPINGS OF FIXED ASSETS

- CAPITAL WORK IN PROGRESS 1

- CAPITAL WORK IN PROGRESS 2

- REVALUATION OF FIXED ASSETS

- Banking transactions, Bank reconciliation statements

- RECAP

- Accounting Examples with Solutions

- RECORDING OF PROVISION FOR BAD DEBTS

- SUBSIDIARY BOOKS

- A PERSON IS BOTH DEBTOR AND CREDITOR

- RECTIFICATION OF ERROR

- STANDARD FORMAT OF PROFIT & LOSS ACCOUNT

- STANDARD FORMAT OF BALANCE SHEET

- DIFFERENT BUSINESS ENTITIES: Commercial, Non-commercial organizations

- SOLE PROPRIETORSHIP

- Financial Statements Of Manufacturing Concern

- Financial Statements of Partnership firms

- INTEREST ON CAPITAL AND DRAWINGS

- DISADVANTAGES OF A PARTNERSHIP FIRM

- SHARE CAPITAL

- STATEMENT OF CHANGES IN EQUITY

- Financial Statements of Limited Companies

- Financial Statements of Limited Companies

- CASH FLOW STATEMENT 1

- CASH FLOW STATEMENT 2

- FINANCIAL STATEMENTS OF LISTED, QUOTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES