|

Basic Concepts of Business: capital, profit, budget |

| << Introduction to Financial Accounting |

| Cash Accounting and Accrual Accounting >> |

Financial

Accounting (Mgt-101)

VU

Lesson-2

Learning

Objective

·

The

evolution of accounting started in the

previous lecture continues with a slight

emphasis on how

actual

record keeping started. In addition,

some basic concepts like

capital, profit, and budget

are

introduced.

Different

Types of Business Entities

·

Commercial

Organizations (Profit Oriented)

o Sole

proprietor

o Partnership

o Limited

companies

·

Non-Commercial

Organizations (Non-Profit Oriented)

o NGO's

(Non-government Organizations)

o Trusts

o Societies

The

Basic Concept of Record

Keeping

·

We can

maintain a diary of transactions and note

the daily transactions like sale,

purchase etc. in it.

Problems

Faced in Maintaining Diary of

Transactions

·

How

will we come to know the

income and expenses from

various sources?

·

We

only have a sheet / page on

which daily transactions are

listed.

·

We do

not know which product is

selling better and which is

not.

Available

Alternate

·

One

can go through all the transactions at

the end of the month and

note the different types

of

transactions

on different pages.

·

So

that every page gives

total for a different type of

transaction like sales of

different products

and

expenses

of different types

4

Financial

Accounting (Mgt-101)

VU

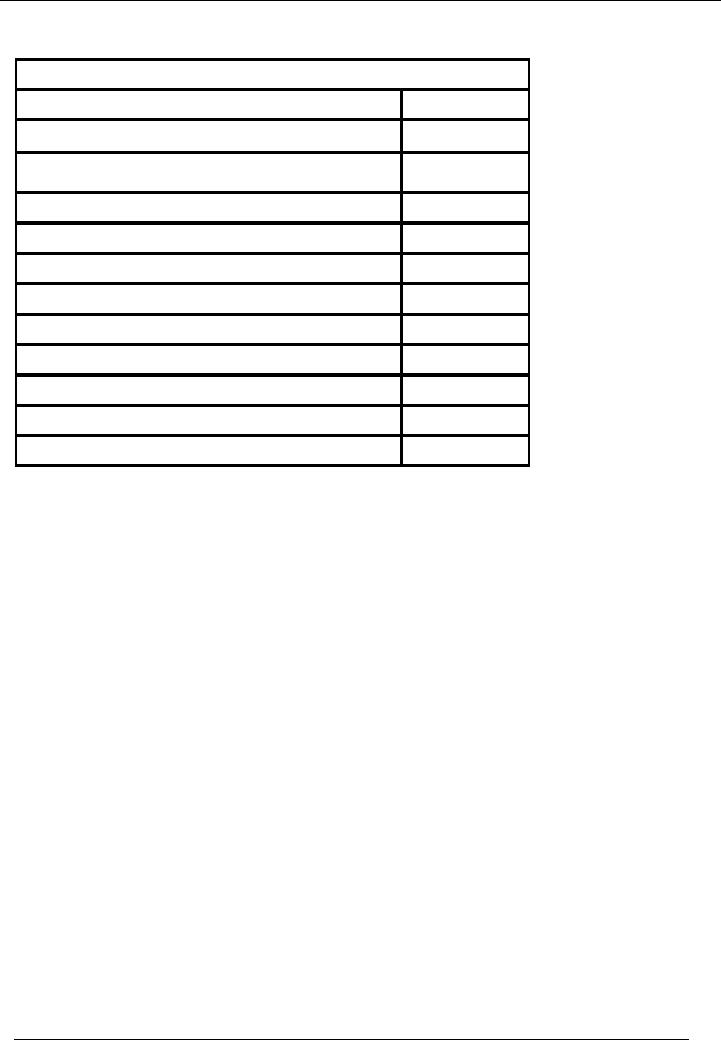

Diary

of Transactions

Transactions

of Jan 20--

P a r t i c u l a r s

Rs.

Sold 5

nos. of Item A

1,000

Purchased

10 nos. of Item B

(

15,000 )

Sold 1

no. of Item C

2,000

Electricity

bill paid

(

1,500 )

Sold 1

no. of Item A

500

Sold 2

nos. of Item B

4,000

Sold 5

nos. of Item A

1,000

Purchased

10 nos. of Item B

(

15,000 )

Sold 1

no. of Item C

2,000

Telephone

bill paid

(

1,000 )

Salary

paid

(

1,500 )

·

Now

try to go through these

transactions and separate,

transactions of different

types.

·

But

what if the number of

transactions is large?

Is it

really possible to go through

hundreds or thousands of transactions at

the month end and

analyse

them to obtain required results.

Cash

and Credit Transactions

·

Sales

and purchase are not

always for cash. Some

times the payment / receipt is

delayed to a future

date

(Sale/purchase for

"UDHAR")

·

The

diary that we have discussed

above, records cash

transactions only.

·

The

"UDHAR"

(credit)

transactions may be noted in

separate diary.

·

Now we

have two diaries. One for

cash and one for

credit.

·

We

need to know total sales

and purchases (both cash

and credit) and other

information like the

amount

that is payable and

receivable.

·

How

will we get our required

results now?

·

Do we

need another diary to combine information

from both these

diaries?

·

But

when we receive or pay cash

for the credit transactions will we

again record the transactions

on

the

day, when cash is received

or paid? If so,

where?

·

So the

problems keep on increasing

with the size or volume of

business. But one thing is

becoming

certain

and that is that an accurate

reflection of business transacted

can only be obtained if

both

cash

and credit transactions are

recorded in such a manner

that there is no duplication

and yet the

transactions

are completely recorded. This is

possible only under Commercial

Accounting.

Commercial

Accounting

· Commercial

Accounting is done through a system

that is known as Double

entry book keeping.

5

Financial

Accounting (Mgt-101)

VU

Single

Entry and Double Entry

Accounting

·

Single

entry accounting/Cash

accounting.

This

system records only cash

movement of transactions and that

too up to the extent of

o

recording

one aspect of the

transactions.

This

means that only receipt or

payment of cash is recorded

and no separate record

is

o

maintained (about

the source of receipt and

payment) as to from whom the

cash was

received

or to whom it was paid.

·

Double

entry book keeping/Commercial

accounting.

Double

entry or commercial accounting

system records both aspects

of transaction i.e.

o

receipt

or payment and source of

receipt or payment.

It

also records credit transactions. Example

of Electricity Bill

o

.

·

This

concept will be explained in detail in the

next lectures but for the

time being it should be noted

that

in cash accounting date of

receipt / payment of actual

cash is important while in

commercial

accounting

the date on which the expense is

caused, whether paid or not, as well as

the spreading of

the

cost of certain items over

their useful life becomes

important.

Capital

·

No

business can run without

money or resources being invested

therein.

·

Whatever

money or resources from

ones' own pocket are put in

a business is referred to as

CAPITAL.

·

This

capital or investment must earn a

return or profit on its use

even if it is coming out of

ones'

pocket.

·

This

return is also known as PROFIT. So no

capital should be without a profit or a

return.

·

Also,

no Capital even if coming from the

business owner can be without

cost. Why? Because if

the

same

sum that was used in a

business was put in the bank or

used to buy Defence Savings

or

National

Savings Certificates, a certain amount of

profit would have been

earned. By putting this

money

in business, a return must be

expected.

Money

Value of Time

·

Another

important concept to remember in

all businesses is that of MONEY VALUE OF

TIME.

·

Time

spend by the owner also has

value; he should be remunerated for

it.(The time of the

proprietor

or business persons spent on the

business is also a business

cost and must be paid for

by

the

business in addition to the

profit)

· Why?

Because if the business person

had employed somebody else

in his place, the person

would be

paid a

salary.

· Therefore, a

business person's time

and money both

have costs attached to them.

Nothing is free

nor

should be expected to be free of

cost.

Goodwill

·

Then

there is something called

GOODWILL.

·

This is simply the

value attached to the good

reputation earned through good,

clean conduct of

business

over a number of years.

·

This

good reputation also has a

value and becomes part of

investment in business

Is

Cash in Hand Our

Profit?

6

Financial

Accounting (Mgt-101)

VU

·

Not

unless we have deducted

from

it the

total amount of expenses that

are accrued or are on

credit

and added to it the sale

made on credit for which

cash is to be received at a later date.

The

simple

equation for calculation of profit would

thus be:

Cash

Sale-Cash Payment + (Credit Sale-Credit

Expense)

·

Also

remember that certain items

have a long life and

will be used during that

time to earn more

money

for business. The cost of

such items will as be spread

over their life and

also accounted for

accordingly

in the above equation.

·

More

on this in later lectures.

Budget

·

Budgeting is

another important aspect of business

planning.

·

The

budget is made to ensure that

there is at least a balance

between Income earned and

the

expenses

incurred on earning this income in the

first instance, and to

provide a reasonable return

on

the

capital used in the

business.

·

However,

if there is a shortfall between of

Income as against expense, it

means that more is

being

spent

and less earned.

·

Decisions

will be required to bring the situation

to balance or if it cannot be so then to

arrange for

loans

or more capital to ensure

business continues.

·

But

business cannot be run on loans

and these must be

repaid.

·

Budget

Is an Organization's Plan of a Future Period

Expressed in Money

Terms.

7

Table of Contents:

- Introduction to Financial Accounting

- Basic Concepts of Business: capital, profit, budget

- Cash Accounting and Accrual Accounting

- Business entity, Single and double entry book-keeping, Debit and Credit

- Rules of Debit and Credit for Assets, Liabilities, Income and Expenses

- flow of transactions, books of accounts, General Ledger balance

- Cash book and bank book, Accounting Period, Trial Balance and its limitations

- Profit & Loss account from trial balance, Receipt & Payment, Income & Expenditure and Profit & Loss account

- Assets and Liabilities, Balance Sheet from trial balance

- Sample Transactions of a Company

- Sample Accounts of a Company

- THE ACCOUNTING EQUATION

- types of vouchers, Carrying forward the balance of an account

- ILLUSTRATIONS: Ccarrying Forward of Balances

- Opening Stock, Closing Stock

- COST OF GOODS SOLD STATEMENT

- DEPRECIATION

- GROUPINGS OF FIXED ASSETS

- CAPITAL WORK IN PROGRESS 1

- CAPITAL WORK IN PROGRESS 2

- REVALUATION OF FIXED ASSETS

- Banking transactions, Bank reconciliation statements

- RECAP

- Accounting Examples with Solutions

- RECORDING OF PROVISION FOR BAD DEBTS

- SUBSIDIARY BOOKS

- A PERSON IS BOTH DEBTOR AND CREDITOR

- RECTIFICATION OF ERROR

- STANDARD FORMAT OF PROFIT & LOSS ACCOUNT

- STANDARD FORMAT OF BALANCE SHEET

- DIFFERENT BUSINESS ENTITIES: Commercial, Non-commercial organizations

- SOLE PROPRIETORSHIP

- Financial Statements Of Manufacturing Concern

- Financial Statements of Partnership firms

- INTEREST ON CAPITAL AND DRAWINGS

- DISADVANTAGES OF A PARTNERSHIP FIRM

- SHARE CAPITAL

- STATEMENT OF CHANGES IN EQUITY

- Financial Statements of Limited Companies

- Financial Statements of Limited Companies

- CASH FLOW STATEMENT 1

- CASH FLOW STATEMENT 2

- FINANCIAL STATEMENTS OF LISTED, QUOTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES

- FINANCIAL STATEMENTS OF LISTED COMPANIES