|

Corporate

Finance FIN 622

VU

Lesson

12

ADVANCE

EVALUATION METHODS

The

following topics will be

discussed in this lecture.

Advance

Evaluation Methods:

Sensitivity

analysis

Profitability

analysis

Break

even accounting

Break

even - economic

SENSITIVITY

ANALYSIS:

Sensitivity

analysis is the study of how the

variation in the output of a model

(numerical or otherwise)

can

be

apportioned, qualitatively or

quantitatively, to different sources of

variation.

A

mathematical model is defined by a series

of equations, input factors,

parameters, and variables

aimed to

characterize

the process being investigated. Input is

subject to many sources of uncertainty

including errors

of

measurement, absence of information

and poor or partial understanding of the

driving forces and

mechanisms.

This

imposes a limit on our

confidence in the response or output of

the model. Further, models may

have

to

cope with the natural intrinsic

variability of the system, such as the

occurrence of stochastic events.

Good

modeling

practice requires that the

modeler provides an evaluation of the confidence in

the model, possibly

assessing

the uncertainties associated with the

modeling process and with the

outcome of the model itself.

Uncertainty

and Sensitivity Analysis offer

valid tools for characterizing the

uncertainty associated with a

model.

Applications

Sensitivity

Analysis can be used to

determine:

1.

The model resemblance with the

process under study

2.

The quality of model

definition

3.

Factors that mostly contribute to

the output variability

4.

The region in the space of input

factors for which the model

variation is maximum

5.

Optimal - or instability - regions

within the space of factors

for use in a subsequent

calibration

study

6.

Interactions between

factors

7.

Sensitivity Analysis is popular in financial

applications, risk analysis, signal

processing, neutrals

networks

and any area where

models are developed.

Methodology

There

are several possible

procedures to perform uncertainty (UA)

and sensitivity analysis (SA).

The most

common

sensitivity analysis is sampling-based. A

sampling-based sensitivity is one in

which the model is

executed

repeatedly for combinations of values

sampled from the distribution

(assumed known) of the

input

factors. Other methods are

based on the decomposition of the variance of the

model output and are

model

independent.

In

general, UA and SA are

performed jointly by executing the model

repeatedly for combination of

factor

values

sampled with some

probability distribution. The

following steps can be

listed:

1.

Specify

the target function and

select the input of

interest

2.

Assign

a distribution function to the selected

factors

3.

Generate

a matrix of inputs with that

distribution(s) through an appropriate

design

4. Evaluate

the model and compute the distribution of

the target function

5.

Select a method for

assessing the influence or relative importance of each

input factor on the

target

function.

PROFITABILITY

ANALYSIS

Successful

financial institutions today are able to

effectively identify those

products, customers,

branches,

and

other factors that impact

overall profitability. But

discovering what's actually

profitable isn't always

straightforward. To

really understand what's driving bank

profitability, you need to be

able to drill down

into

the lowest level of detail, and analyze

data with ease and

precision.

Profitability

is a dynamic, accountable solution

for managing customer relationships

and measuring

37

Corporate

Finance FIN 622

VU

performance

providing a complete picture of

your organization's profitability. It

allows you to analyze

your

business across unlimited

dimensions. Beyond customer

profitability, product profitability

and

organizational

profitability, it's sophisticated, multi-dimensional

OLAP environment provides the

unique

ability

to calculate profitability at the account

level, drill up and down

through every level of the

hierarchy,

and

aggregate up for any

reporting or analytical dimension, for

improved accuracy and better

decision-

making.

This

flexibility allows you to

analyze...

Customers

who are 'at risk'

Performance

of an officer that supports

multiple business units

Business

unit performance across a

group of branches

Customer

households reported in multiple

market segments

Geographic

views that aren't aligned

with organizational units

Product

success across a group of

market segments

Origination

trends by groups of officers, branches,

or by market segment

BREAK-EVEN

ACCOUNTING

This type of

report is not one that is

automatically generated by most

accounting software, nor is it

one that

is

normally produced by your accountant,

but it is an important analysis

for you to have and

understand.

For

any new business, you should

predict what gross sales volume level

you will have to achieve

before you

reach

the break-even point and then, of

course, build to make a

profit. For early-stage

businesses, you

should be

able to assess your early

prediction and determine how

accurate they were, and

monitor whether

you

are actually on track to

make the profits you need.

Even the mature business

would be wise to look

at

their

current break-even point and

perhaps find ways to lower

that benchmark to increase

profits. The

recent

massive layoffs at large corporations are

directed at this goal, lowering the

break-even point and

increasing

profits.

Break-Even

Is the Volume Where All

Fixed Expenses Are

Covered:

You

will start a break-even

analysis by establishing all the

fixed (overhead) expenses of

your business. Since

most

of these are done on a monthly

basis, don't forget to include the

estimated monthly amount of

line

items

that are normally paid on a quarterly or

annual basis such as payroll

taxes or insurance. For

example, if

your

annual insurance charge is

$9,000, use 1/12 of that, or

$750 as part of your monthly

budget. With the

semi

variable expense (such as phone

charges, travel, and marketing), use

that portion that you

expect to

spend

each and every

month.

For

the purpose of a model break-even, let's

assume that the fixed

expenses look as

follows:

Administrative

salaries

$1,500

Rent

800

Utilities

300

Insurance

150

Taxes

210

Telephone

240

Auto

expense

400

Supplies

100

Sales

and marketing

300

Interest

100

Miscellaneous

400

Total

$4,500

These

are the expenses that must

be covered by your gross

profit. Assuming that the

gross profit margin

is

30

percent, what volume must

you have to cover this

expense? The answer in this

case is 15,000--30

percent

of that amount is $4,500, which is

your target number.

38

Corporate

Finance FIN 622

VU

The

two critical numbers in these

calculations are the total of the

fixed expense and the

percentage of gross

profit

margin. If your fixed

expense is $10,000 and your

gross profit margin is 25

percent, your

break-even

volume

must be $40,000.

This

Is Not a Static

Number:

You

may do a break-even analysis before

you even begin your business

and determine that your

gross

margin

will come in at a certain

percentage and your fixed

expense budget will be set at a

certain level. You

will

then be able to establish

that your business will

break even (and then go on

to a profit) at a certain level

of

sales volume. But your

pre-start projections and your operating

realities may be very different.

After

three

to six months in business, you should

compare projections to the real-world

results and reassess,

if

necessary,

what volume is required to reach

break-even levels.

Along

the way, expenses tend to

creep up in both the direct and

indirect categories, and you

may fall below

the

break-even volume because

you think it is lower than it

has become. Take your

profit and loss

statement

every

six months or so and refigure your

break-even target number.

Ways

to Lower Break-Even:

There

are three ways to lower

your break-even volume, only

two of them involve cost controls

(which

should

always be your goal on an

ongoing basis).

1.

Lower direct costs, which

will raise the gross margin.

Be more diligent about purchasing

material,

controlling

inventory, or increasing the productivity

of your labor by more cost

effective scheduling or

adding

more efficient technology.

2.

Exercise cost controls on your

fixed expense, and lower the

necessary total dollars. Be

careful when

cutting

expenses that you do so with

an overall plan in mind. You

can cut too deeply as

well as too little

and

cause

distress among workers, or

you may pull back marketing

efforts at the wrong time, which

will give out

the

wrong signal.

3.

Raise prices! Most

entrepreneurs are reluctant to raise

prices because they think

that overall business

will

fall

off. More often than

not that doesn't happen

unless you are in a very

price-sensitive market, and if

you

are,

you really have already

become volume driven.

But if

you are in the typical niche-type small

business, you can raise

your prices 4 to 5 percent

without much

notice of

your customers. The effect is startling.

For example, the first model we

looked at was the

following:

Volume

$15,000

direct

cost

10,500

70%

gross

profit

4,500

Raising

the prices 5 percent would

result in this change:

Volume

$15,750

direct

cost

10,500

67%

gross

profit

5,250

You

will have increased your

margin by 3 percent, so you can

lower the total volume you

will require to

break

even.

The Goal Is

Profit:

You

are in business to make a

profit not just break

even, but by knowing where

that number is, you

can

accomplish

a good bit:

· You

can allocate the sales and

marketing effort to get you to the

point you need to

be.

· Most

companies have slow months,

so if you project volume

below break-even, you can

watch

expenses

to minimize losses. A few really bad months

can wipe out a good bit of

previous profit.

· Knowing

the elements of break-even allows

you to manage the costs to

maximize the bottom

line.

Once

you have gotten this far in

the knowledge of the elements of your

business, you are well on

your way

to

success.

39

Corporate

Finance FIN 622

VU

The

breakeven

point in

economics is the point at which

cost or expenses and income

are equal - there is

no net

loss or gain, one has

"broken even".

The

point at which a firm or

other economic entity breaks

even is equal to its fixed

costs divided by its

contribution

to profit per unit of

output, which can be shown

by the following formula:

The

break even point is also the

point on a chat indicating the time

when something has broken

even, and is

a

general term for not having

gained or lost something in a

process.

The

Contribution per Unit can be

worked out using

Contribution

= Price per Unit - Variable

Costs per Unit

The

break

even point for a

product is the point where

total revenue received

equals total costs

associated

with

the sale of the product (TR=TC). A

break even point is

typically calculated in order

for businesses to

determine

if it would be profitable to sell a

proposed product, as opposed to

attempting to modify an

existing

product instead so it can be

made lucrative. Break-Even Analysis can

also be used to analyze

the

potential

profitability of an expenditure in a sales-based

business.

In

unit sales

If the

product can be sold in a

larger quantity than occurs

at the break even point,

then the firm will make

a

profit;

below this point, a loss.

Break-even quantity is calculated

by:

Total

fixed costs / (price -

average variable costs)

(Explanation

- in the denominator, "price minus

average variable cost" is the variable profit per

unit, or

contribution

margin of each unit that is

sold.)

Firms

may still decide not to

sell low-profit products,

for example those not

fitting well into their

sales mix.

Firms

may also sell products that

lose money - as a loss

leader, to offer a complete

line of products, etc.

But

if a

product does not break

even, or a potential product looks

like it clearly will not

sell better than the

break

even

point, then the firm will

not sell, or will stop

selling, that

product.

An

example:

Assume

we are selling a product for

$2 each.

Assume

that the variable cost associated

with producing and selling

the product is 60 cents.

Assume

that the fixed cost related

to the product (the basic costs

that are incurred in operating

the

business even if no product is produced)

is $1000.

In this

example, the firm would have

to sell (1000/ (2 - 0.6) =

714) 714 units to break

even.

In

price changes

By inserting

different prices into the

formula, you will obtain a

number of break even points, one

for each

possible

price charged. If the firm to

change the selling price for

its product, from $2 to

$2.30, in the

example

above, then it would have to

sell only (1000/(2.3 -

0.6))= 589 units to break

even, rather than

714.

40

Corporate

Finance FIN 622

VU

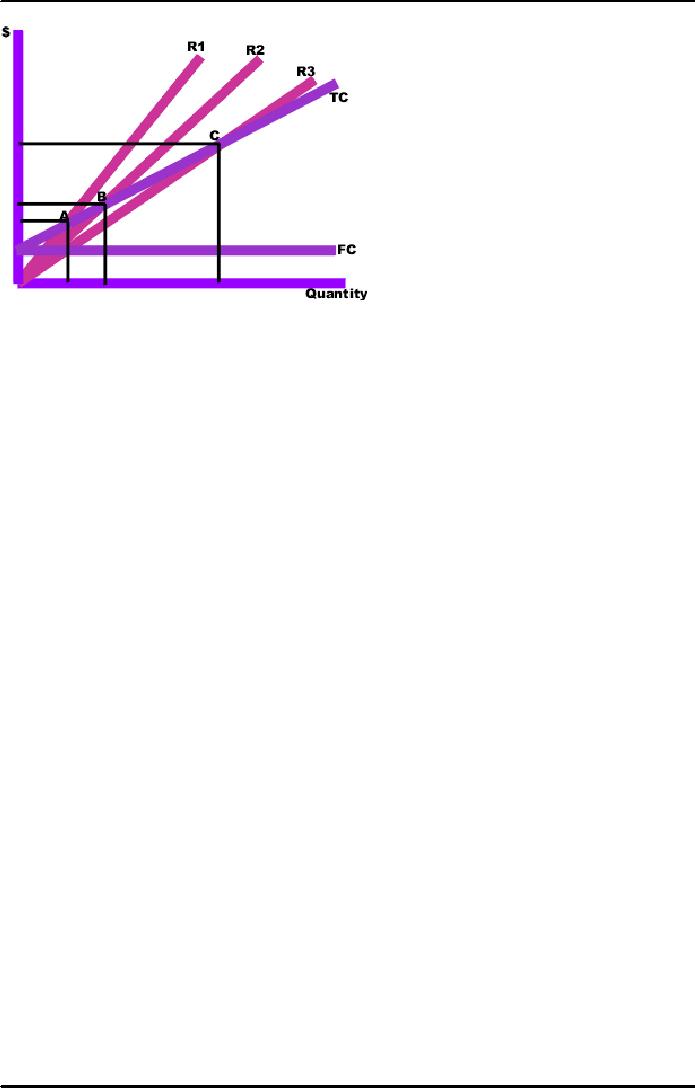

To

make the results clearer, they

can be graphed. To do this, you

draw the total cost curve

(TC in the

diagram)

which shows the total cost

associated with each

possible level of output, the fixed

cost curve (FC)

which

shows the costs that do not

vary with output level, and

finally the various total

revenue lines (R1,

R2,

and

R3) which show the total

amount of revenue received at each

output level, given the price you

will be

charging.

The

break even points (A,B,C)

are the points of intersection between

the total cost curve (TC)

and a total

revenue

curve (R1, R2, or R3).

The break even quantity at

each selling price can be

read off the

horizontal,

axis

and the break even price at

each selling price can be

read off the vertical axis.

The total cost,

total

revenue,

and fixed cost curves

can each be constructed with

simple formula. For example,

the total revenue

curve

is simply the product of selling price

times quantity for each

output quantity. The data

used in these

formulas

come either from accounting

records or from various estimation

techniques such as

regression

analysis.

In

potential expenditures Break-Even

Analysis can be used in the evaluation of

the cost-effectiveness of a

new

expenditure for a sales-revenue based

business. Here, the cost can be

evaluated in terms of

revenues

needed

to break even on the investment, or more

specifically, to determine how

much of an increase in

sales

revenues would be necessary to

break even.

An

illustrative example of this is a retail lumberyard

who is considering the purchase of a

delivery truck. The

goal

is to evaluate how large an

increase in sales revenue is

necessary to break even on the investment

in a

delivery

truck. For this example, the

company's front-door margin

(that is, sales revenue

minus the cost of

goods

sold and costs of doing

business) is 5%, and the cost of the

desired delivery truck is $50,000.

To

calculate

the break-even level of expenditure, the following

formula can be used:

Expenditure

($) = (Front-door margin %) X (Revenue

Increase needed to break

even)

To

break even using the above

example, $50,000 must equal

5% of the sales INCREASE ("SI") in

order to

break

even. The variable which

must be isolated is the Sales

Increase.

$50,000

= 5% of SI

$50,000

= .05 * SI

$50,000/.05

= SI

$1,000,000

= SI

Sales

increase of $1,000,000 is needed to

break even on the investment on the delivery

truck. The business

must

then decide how it can

use the delivery truck to help

increase sales by $1,000,000; if it

can, then they

will

break even, and if it can

not, then it would be an ill-advised

investment. If sales revenues pass

the

break-even

point, 5% of further increase

would be bottom line

profit.

Of

course, in most cases, such

an investment will not be paid out in

lump sum or in one year,

so

appropriate

adjustments can be made for

the payments, and the scenario

can be focused on a monthly

basis

during

repayment, or can be extended

out through and beyond the

repayment period to evaluate a

longer

term

return. Also such

calculations can be used

with smaller-scale and shorter-term

scenarios (such as a

temporary

employee or a new computer) or on a much

larger scale such as a new

construction or

acquisition.

41

Corporate

Finance FIN 622

VU

It is notable that,

since most businesses have

among their goals to be

profitable, desired profits should

be

added

as a cost of doing

business.

Limitations

·

This

is only a supply side (i.e.:

costs only) analysis.

·

It

tells you nothing about what

sales are actually likely to

be for the product at these

various prices.

·

It

assumes that fixed costs

(FC) are constant

·

It

assumes average variable costs

are constant per unit of

output, at least in the range of

sales (both

prices

and likely quantities) of

interest.

ECONOMIC

BEAK-EVEN

The

problem associated with

accounting break even is

that accounting earnings are

calculated after the

deduction of

all costs except the

opportunity cost of the capital

that is invested in the project.

Accounting

for the cost of capital is

simple, at least in principle,

when working out income or

profit, we

should

also deduct the opportunity

cost of capital employed

just as we deduct all other

costs. Income that is

worked

out, as this (after deducting cost of

capital) is known as economic

profit or economic value

added

(EVA).

A project that has a

positive EVA adds to firm

value; one with a negative

EVA reduces firm

value.

42

Table of Contents:

- INTRODUCTION TO SUBJECT

- COMPARISON OF FINANCIAL STATEMENTS

- TIME VALUE OF MONEY

- Discounted Cash Flow, Effective Annual Interest Bond Valuation - introduction

- Features of Bond, Coupon Interest, Face value, Coupon rate, Duration or maturity date

- TERM STRUCTURE OF INTEREST RATES

- COMMON STOCK VALUATION

- Capital Budgeting Definition and Process

- METHODS OF PROJECT EVALUATIONS, Net present value, Weighted Average Cost of Capital

- METHODS OF PROJECT EVALUATIONS 2

- METHODS OF PROJECT EVALUATIONS 3

- ADVANCE EVALUATION METHODS: Sensitivity analysis, Profitability analysis, Break even accounting, Break even - economic

- Economic Break Even, Operating Leverage, Capital Rationing, Hard & Soft Rationing, Single & Multi Period Rationing

- Single period, Multi-period capital rationing, Linear programming

- Risk and Uncertainty, Measuring risk, Variability of returnHistorical Return, Variance of return, Standard Deviation

- Portfolio and Diversification, Portfolio and Variance, RiskSystematic & Unsystematic, Beta Measure of systematic risk, Aggressive & defensive stocks

- Security Market Line, Capital Asset Pricing Model CAPM Calculating Over, Under valued stocks

- Cost of Capital & Capital Structure, Components of Capital, Cost of Equity, Estimating g or growth rate, Dividend growth model, Cost of Debt, Bonds, Cost of Preferred Stocks

- Venture Capital, Cost of Debt & Bond, Weighted average cost of debt, Tax and cost of debt, Cost of Loans & Leases, Overall cost of capital WACC, WACC & Capital Budgeting

- When to use WACC, Pure Play, Capital Structure and Financial Leverage

- Home made leverage, Modigliani & Miller Model, How WACC remains constant, Business & Financial Risk, M & M model with taxes

- Problems associated with high gearing, Bankruptcy costs, Optimal capital structure, Dividend policy

- Dividend and value of firm, Dividend relevance, Residual dividend policy, Financial planning process and control

- Budgeting process, Purpose, functions of budgets, Cash budgetsPreparation & interpretation

- Cash flow statement Direct method Indirect method, Working capital management, Cash and operating cycle

- Working capital management, Risk, Profitability and Liquidity - Working capital policies, Conservative, Aggressive, Moderate

- Classification of working capital, Current Assets Financing Hedging approach, Short term Vs long term financing

- Overtrading Indications & remedies, Cash management, Motives for Cash holding, Cash flow problems and remedies, Investing surplus cash

- Miller-Orr Model of cash management, Inventory management, Inventory costs, Economic order quantity, Reorder level, Discounts and EOQ

- Inventory cost Stock out cost, Economic Order Point, Just in time (JIT), Debtors Management, Credit Control Policy

- Cash discounts, Cost of discount, Shortening average collection period, Credit instrument, Analyzing credit policy, Revenue effect, Cost effect, Cost of debt o Probability of default

- Effects of discountsNot effecting volume, Extension of credit, Factoring, Management of creditors, Mergers & Acquisitions

- Synergies, Types of mergers, Why mergers fail, Merger process, Acquisition consideration

- Acquisition Consideration, Valuation of shares

- Assets Based Share Valuations, Hybrid Valuation methods, Procedure for public, private takeover

- Corporate Restructuring, Divestment, Purpose of divestment, Buyouts, Types of buyouts, Financial distress

- Sources of financial distress, Effects of financial distress, Reorganization

- Currency Risks, Transaction exposure, Translation exposure, Economic exposure

- Future payment situation hedging, Currency futures features, CF future payment in FCY

- CFfuture receipt in FCY, Forward contract vs. currency futures, Interest rate risk, Hedging against interest rate, Forward rate agreements, Decision rule

- Interest rate future, Prices in futures, Hedgingshort term interest rate (STIR), ScenarioBorrowing in ST and risk of rising interest, Scenariodeposit and risk of lowering interest rates on deposits, Options and Swaps, Features of opti

- FOREIGN EXCHANGE MARKETS OPTIONS

- Calculating financial benefitInterest rate Option, Interest rate caps and floor, Swaps, Interest rate swaps, Currency swaps

- Exchange rate determination, Purchasing power parity theory, PPP model, International fisher effect, Exchange rate system, Fixed, Floating

- FOREIGN INVESTMENT: Motives, International operations, Export, Branch, Subsidiary, Joint venture, Licensing agreements, Political risk