|

VERIFICATION APPROACH OF AUDIT |

| << TESTING THE NON-CURRENT ASSETS |

| VERIFICATION OF ASSETS >> |

Fundamentals

of Auditing ACC 311

VU

Lesson

32

VERIFICATION

APPROACH OF AUDIT

We are

now moving on to deal with

the substantive testing, or

verification aspect of the

audit. In the past

lectures

we have been learning the

early steps in the time structure of an

audit:

·

Accepting

the appointment

·

Planning,

recording, controlling the

audit

·

Evaluation

internal controls

·

Testing

the controls

By

this stage, the auditor

will have made a decision on

the general approach to be taken to the

audit work. If

the

controls systems are effective

and operating as laid down, the

amount of verification work

will be reduced.

If the

controls are weak or are

not operating effectively, a high

level of verification work

will be performed. It

is

this verification work that we

are dealing with in this

and the next few

lectures.

To

verify means to establish the

truth of something. This audit work

involves the audit in gathering

evidence

this

will lead to a conclusion as to

whether classes of transactions,

balances and disclosures

reflected in the

client's

financial statements are properly stated

(true and fair).

We

have already discussed in

detail the general audit

verification principles; here we

will have a brief over

view

of

those.

Audit

Verification Techniques:

As we

have already discussed in the

previous lectures that at the

verification stage of the

audit, the auditor is

typically

presented with a set of

draft financial statements prepared by

the client. The

role of the auditor is

to

generate

evidence to allow a conclusion to be

reached as to whether the information

contained in

these

financial statements, and the way

the information is presented and

disclosed, give a true

and

fair

view.

We

already know that audit evidences

are generated by the auditor performing

audit tests. Here, in verification

work,

the auditor will use

substantive testing procedures,

designed to give evidence

relating to the figures

in

the

financial statements, rather than control

test, dealing with the

systems that produced those

figures.

However,

the testing procedures

available to the auditor here are

the same as those we saw

earlier. As a

reminder,

audit-testing procedures available to

the auditor are:

1. Inspection

This

covers the physical review or

examination of records, documents

and tangible assets. An

example in

substantive

testing is examining purchase

invoices to ensure that they

have been properly recorded

and

analyzed

in the financial statements.

2. Observation

This

procedure is mainly applicable to

tests of control, but may

also be used in substantive

testing, such as the

auditor

observing the client's

inventory count to gain evidence that

the inventory figure in the

financial

statements

had been arrived at

accurately.

3. Enquiry

Seeking

relevant information from

knowledgeable persons inside or

outside the

enterprise.

An

example in substantive testing is

asking management for an explanation as

to why a receivable has, or

has

not,

been treated as bad.

4. Computation

Checking

the arithmetical accuracy of

records or performing independent

calculations, for example

computing

or

re-computing the depreciation expense

for the year.

5. Analytical

procedures

You

should note that these procedures

are mainly used in substantive

testing rather than as a test of

controls.

They

may help the auditor to understand

relationships between figures in the

financial statements. This is

sometimes

referred to as the business approach to

auditing.

Choice

of Verification Techniques

There

are no specific rules that

exist as to the type(s) of techniques

that the auditor should use

in a given set of

circumstances.

This is principally

a matter of audit judgment and

the nature of the audit objective(s). The

auditor has to look

at

each individual item in its

own right, identify the audit

objective(s) for that

particular item and then

decide

104

Fundamentals

of Auditing ACC 311

VU

the

most reliable audit evidence

available. The circumstances and

evidence available will

affect the type of

technique(s)

he uses.

Audit

Objectives and Financial Statement

Assertions

As

just stated the type(s) of

technique(s) used depend on

the audit objectives that the auditor is

seeking to

achieve.

The

general objective to be achieved by audit

verification work is to establish

whether the financial statements

present

a true and fair view.

We can

identify a number of more

detailed objectives which underlie this

overall objective. These

more

detailed

objectives allow the auditor to design a

series of substantive test on

each audit area (inventory,

receivables,

etc) which will build up the

overall bank of evidence necessary to support

the overall audit

opinion.

In

carrying out substantive audit

tests (verification work) the

auditor will be looking for

evidence on different

assertions

at the financial statements level.

Assertions

in obtaining Audit Evidence:

(a)

Assertions about classes

of transactions and

events for the period under

audit;

(i)

Occurrence

transactions and events that

have been recorded have

occurred and pertain to

the

entity;

(ii)

Completeness

all

transactions and events that

should have been recorded

have been

recorded;

(iii)

Accuracy

amounts and other data

relating to recorded transactions

and events have

been

recorded

appropriately.

(iv)

Cutoff

transactions and events have

been recorded in the proper

period.

(v)

Classification

transactions and events have

been recorded in the proper

accounts.

(b)

Assertions about account

balances at the

period end.

(i)

Existence

assets, liabilities, and equity interests

exist;

(ii)

Rights

and obligations the

entity holds or controls the

rights to assets, and liabilities

are

the

obligations of the entity;

(iii)

Completeness

all

assets, liabilities and equity interests

that should have been

recorded

have

been recorded;

(iv)

Valuation

and allocation

assets, liabilities, and equity interests

are included in the

financial

statements

at appropriate amounts and

any resulting valuation or allocation

adjustments are

appropriately

recorded.

(c)

Assertions about Presentation

and Disclosure:

(i)

Occurrence

and

rights and obligations disclosed

events, transactions and

other matters

have

occurred and pertain to the

entity.

(ii)

Completeness

all

disclosures that should have

been included in the financial

statements

have

been included;

(iii)

Classification

and understandability financial

information is appropriately

presented

and

described, and disclosures

are clearly

expressed;

(iv)

Accuracy

and valuation financial

and other information are

disclosed fairly and

at

appropriate

amounts.

This

concept takes the view that

draft accounts presented by the client to

the auditor are making a

number of

promises,

or assertions. The role of substantive

testing is to verify these

assertions.

The

assertions made by the financial

statements and the related

objectives of the substantive

testing objectives

set

out above can be shown as

follows:

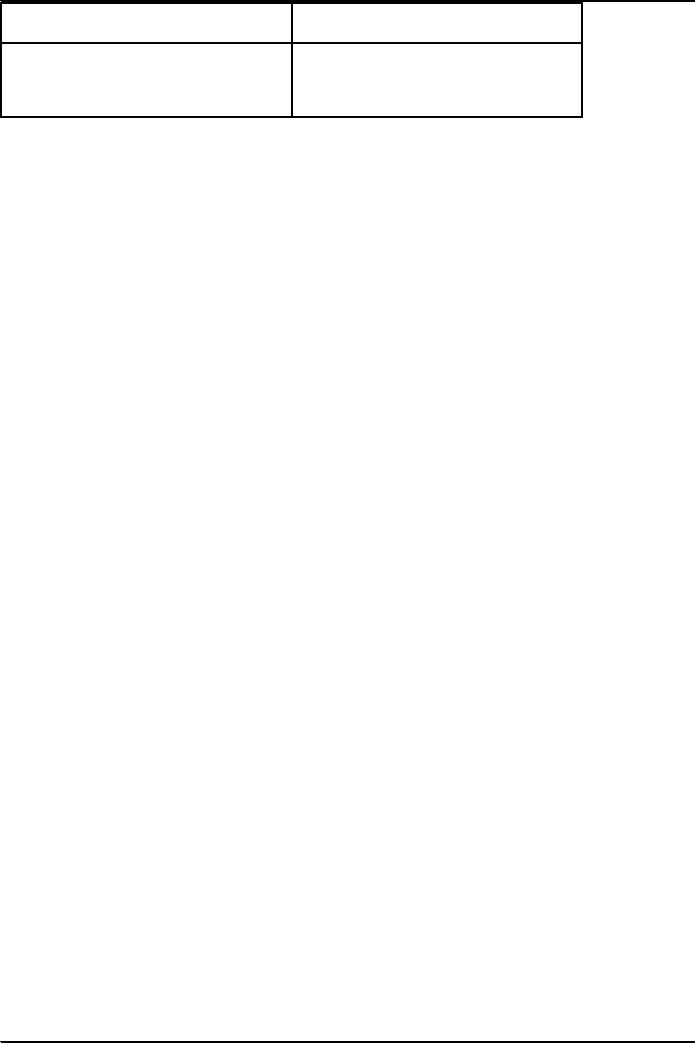

ASSERTION

TESTING

OBJECTIVE

Assets

shown include all rights

under the

Completeness

control

of the enterprise

Transactions

arising during the period

are

Occurrence

reflected

in the period's financial

statements

The

amounts at which assets and

liabilities

Valuation

are

stated is correct

105

Fundamentals

of Auditing ACC 311

VU

Assets

and liabilities included on the balance

Existence

sheet

actually exist

Assets

and liabilities are shown in

the

Presentation

and

financial

statements such that the

user would disclosure

have a

clear understanding of the

client's

financial

situation

Review

of Financial Statements

Content

of Financial Statements

It is

important that you are clear as to

exactly what the financial statements

consist of under

modern

accounting

practice.

They

comprise the

following:

a) The primary

statements

i)

Balance

sheet

ii)

Income statement

iii)

Statement of changes in

equity

iv)

Cash flow

statement

v) The

notes to the accounts

b) The

directors' report

c) The

auditor's report.

The

main principles underlying the

preparation and presentation of

company financial statements are

now set

out by

the International Accounting

Standards Board's document

Framework

for the Preparation and

Presentation of

Financial

Statements.

The

major points from this

document are summarized

below:

1

The

elements of Financial

Statements

The

starting point here is

definitions of assets and liabilities.

The other elements are then defined in

terms of

these.

Assets

are

rights or other access to future

economic benefits controlled by an entity

as a result of past

transactions

or events.

Liabilities

are

obligations of an entity to transfer

economic benefits as a result of

past transactions or

events.

Owners'

equity is

arrived at by deducting liabilities from

assets (capital = assets -

liabilities).

Gains

and losses are

determined in terms of increases

and decreases in owners'

equity.

2

Recognition

in financial statements

Recognition

essentially means the recording

process. The principles here

address such questions as

when is it

acceptable

to recognize (record) an asset or

liability and when should

assets and liabilities be de-recognized

(no

longer

recorded in financial statements). The

main points to note are:

Assets

and liabilities should be recognized

when there is evidence of

their existence and they

can be

reliably

measured.

They

should be derecognized when the

right (assets) or obligations (liabilities) no longer

exist.

The

Timing of Audit

Procedures:

Whereas

tests

of control can be

(and usually are) performed by

the auditor before the client's year

end - at the

so

called interim audit stage -

Substantive

Audit Procedures and

verification work will be

performed

primarily

at or very soon after the

client's year end, as these

procedures normally rely on the

availability of

draft

financial statements.

Verification

of the individual assets and

liabilities by the auditor extends into

the post balance sheet period

(i.e.

the

period between the year end

date and the date of approval of the

financial statements). The auditors

will

use

this to their advantage when

seeking to verify amounts

stated for contingent liabilities, and

for post

balance

sheet events (These are

explained in a later

chapter).

SUBSTANTIVE

PROCEDURES

Substantive

procedures are performed in order to

detect material misstatements at

the assertion level

(Like;

occurrence,

completeness, accuracy, valuation,

existence, rights and control),

and include tests of details

of

classes

of transactions, account balances

and disclosures and

substantive analytical

procedures.

106

Fundamentals

of Auditing ACC 311

VU

Nature

of Substantive Procedures

·

Tests of

details are

ordinarily more appropriate to

obtain audit evidence regarding

certain assertions about

account

balances, including existence and

valuation.

·

Analytical

procedures are

applied on large volume of transactions,

which are predictable over time.

(Cost of

goods

sold, payroll, sale)

Timing of

Substantive Procedures

Year

end substantive procedures

are always more

reliable

In

considering whether to perform

substantive procedures at an interim

date the auditor considers

such

factors

as the following:

· The

control environment and other

relevant controls. (Like payroll

disbursement)

· The

availability of information at a later

date that is necessary for

the auditor's procedures

(Provision

for

doubtful debts can be

investigated interim but debtor

and inventory can be

verified at the year

end).

· The objective

of the substantive

procedure.

· The

assessed risk of material

misstatement (Prefer always at

year end).

· The

nature of the class of

transactions or account balance

and related assertions (Like

frequency of

occurrence

of the transactions e.g.

salaries are paid monthly

whereas bonuses are paid

annually).

· The

ability of the auditor to perform

appropriate substantive procedures or

substantive procedures

combined

with tests of controls to

cover the remaining period in order to

reduce the risk that

misstatements

that exist at period end are

not detected (Staffing problem that

cannot make the

auditor

able to extend till the year

end)

If

substantive procedures are performed at

an interim date, the auditor may

sometimes consider applying

tests

of

controls also on the transactions of

remaining period while extending his

substantive procedures

from

interim

date to the period

end.

Extent

of performance of substantive

procedures

Greater

the risk of material

misstatement due to weaknesses in

the system of internal control,

the greater

would

be the risk of material misstatement in

the financial statements.

In

designing tests of details,

the auditor may use either

audit sampling or may choose to

select items to be

tested

by some other selective

means of testing.

107

Table of Contents:

- AN INTRODUCTION

- AUDITORS REPORT

- Advantages and Disadvantages of Auditing

- OBJECTIVE AND GENERAL PRINCIPLES GOVERNING AN AUDIT OF FINANCIAL STATEMENTS

- What is Reasonable Assurance

- LEGAL CONSIDERATION REGARDING AUDITING

- Appointment, Duties, Rights and Liabilities of Auditor

- LIABILITIES OF AN AUDITOR

- BOOKS OF ACCOUNT & FINANCIAL STATEMENTS

- Contents of Balance Sheet

- ENTITY AND ITS ENVIRONMENT AND ASSESSING THE RISKS OF MATERIAL MISSTATEMENT

- Business Operations

- Risk Assessment Procedures & Sources of Information

- Measurement and Review of the Entitys Financial Performance

- Definition & Components of Internal Control

- Auditing ASSIGNMENT

- Benefits of Internal Control to the entity

- Flow Charts and Internal Control Questionnaires

- Construction of an ICQ

- Audit evidence through Audit Procedures

- SUBSTANTIVE PROCEDURES

- Concept of Audit Evidence

- SUFFICIENT APPROPRIATE AUDIT EVIDENCE AND TESTING THE SALES SYSTEM

- Control Procedures over Sales and Debtors

- Control Procedures over Purchases and Payables

- TESTING THE PURCHASES SYSTEM

- TESTING THE PAYROLL SYSTEM

- TESTING THE CASH SYSTEM

- Controls over Banking of Receipts

- Control Procedures over Inventory

- TESTING THE NON-CURRENT ASSETS

- VERIFICATION APPROACH OF AUDIT

- VERIFICATION OF ASSETS

- LETTER OF REPRESENTATION VERIFICATION OF LIABILITIES

- VERIFICATION OF EQUITY

- VERIFICATION OF BANK BALANCES

- VERIFICATION OF STOCK-IN-TRADE AND STORE & SPARES

- AUDIT SAMPLING

- STATISTICAL SAMPLING

- CONSIDERING THE WORK OF INTERNAL AUDITING

- AUDIT PLANNING

- PLANNING AN AUDIT OF FINANCIAL STATEMENTS

- Audits of Small Entities

- AUDITORS REPORT ON A COMPLETE SET OF GENERAL PURPOSE FINANCIALSTATEMENTS

- MODIFIED AUDITORS REPORT