|

Economics: Another Perspective, Factors of Production |

| << ECONOMICS:Themes of Microeconomics, Theories and Models |

| REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve >> |

Microeconomics

ECO402

VU

Lesson

2

Economics;

Another Perspective

Economics is

the study of the choices

made by people who are

faced with scarcity.

Scarcity

is a situation in which resources

are limited but can be

used in different

ways;

so

one good or service must be

sacrificed for

another.

Society's

Choices

The

decisions of producers, consumers

and government determine how

an economic

system

answers three fundamental

questions:

1.

What products do we

produce?

2.

How do we produce these

products?

3.

Who consumes the

products?

Factors

of Production

Factors

of production are the

resources that are used to

produce goods and

services:

1.

Natural resources:

The

things created by acts of

nature such as land, water,

mineral, oil and

gas

deposits,

renewable and nonrenewable

resources.

2.

Labor:

The

human effort, physical and

mental, used by workers in

the production of

goods

and

services.

3.

Physical capital.

All

the machines, buildings,

equipment, roads and other

objects made by human

beings

to produce goods and

services.

4.

Human capital:

The

knowledge and skills

acquired by a worker through

education and

experience.

5.

Entrepreneurship:

The

effort to coordinate the

production and sale of goods

and services.

Entrepreneurs

take risk and commit

time and money to a business

without any

guarantee

of profit.

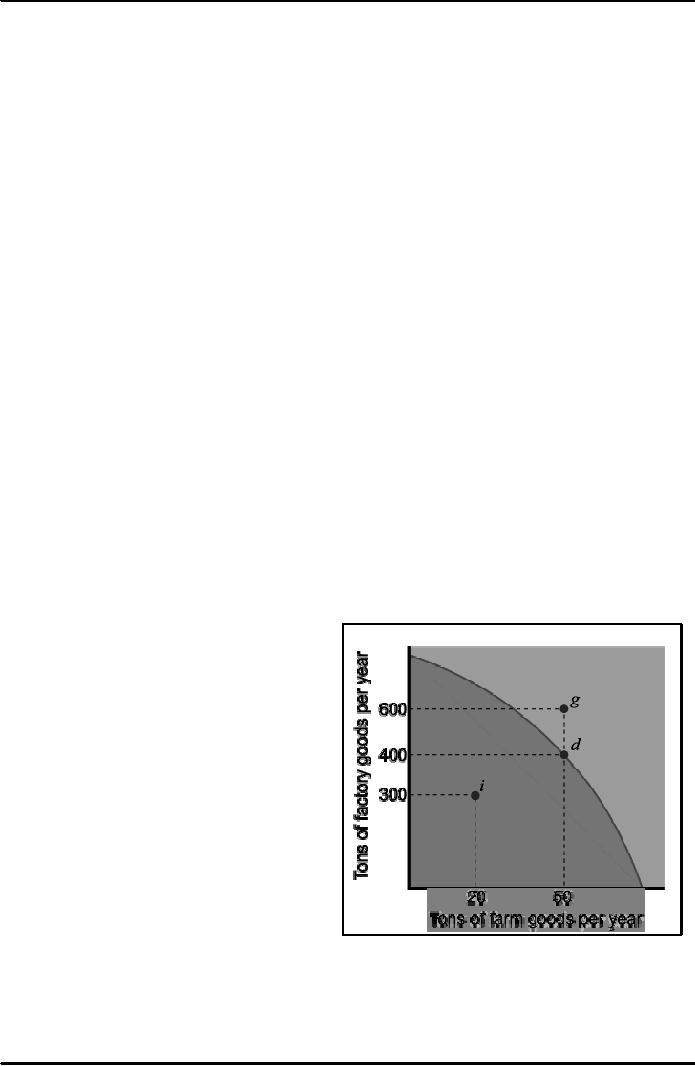

The

Production Possibilities

Frontier

(PPF)

The

PPF curve shows

the possible

combinations

of goods and

services

available

to an economy, given that

all

productive

resources are fully and

efficiently

employed.

When

the economy is at point

i,

resources

are

not fully employed and/or

they are not

used

efficiently. Point g

is

desirable because

it

yields more of both goods,

but not

attainable

given the amount of

resources

available.

Point d

is

one of the possible

combinations

of goods produced

when

resources

are fully and efficiently

employed.

3

Microeconomics

ECO402

VU

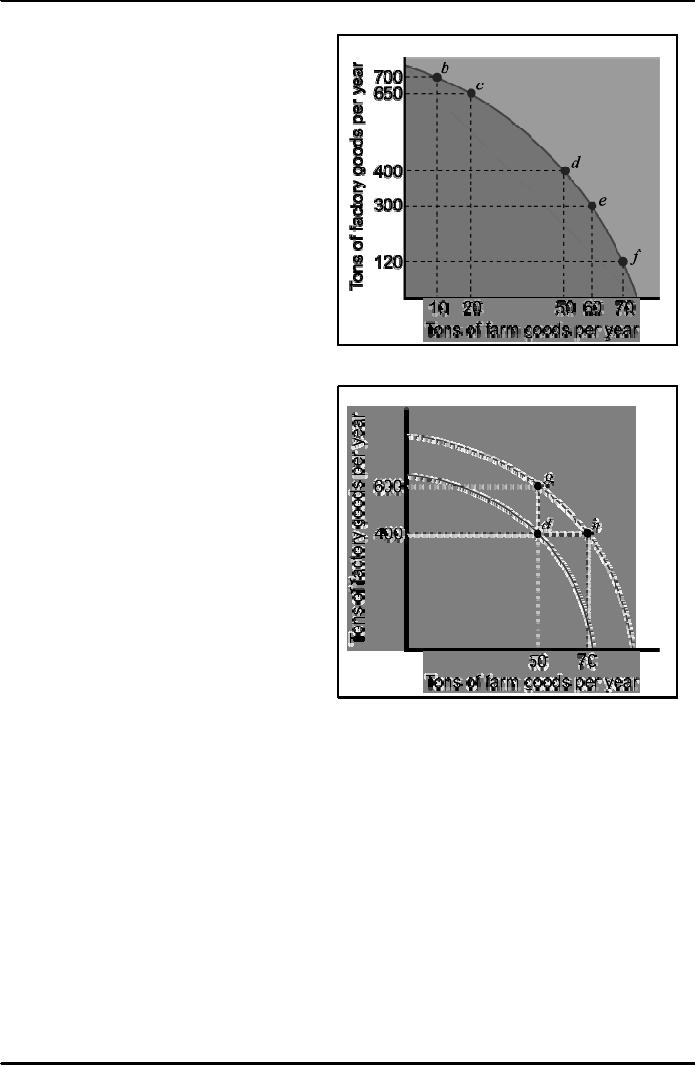

Scarcity

and the PPF

To

increase the amount of farm

goods by

10

tons, we must sacrifice 100

tons of

factory

goods.

The

PPF curve is bowed out

because

resources

are not perfectly adaptable

to the

production

of the two goods. As

we

increase

the production of one good,

we

sacrifice

progressively more of the

other.

Shifting

the PPF Curve

To

increase the production of

one good

without

decreasing the production of

the

other,

the PPF curve must

shift outward.

The

PPF curve shifts outward as

a result of

an

increase in the economy's

resources OR

a

technological innovation that

increases

the

output obtained from a given

amount of

resources.

From point d,

an additional 200

tons

of factory goods or 20 tons of

farm

goods

are now possible

(or any

combination

in between).

4

Table of Contents:

- ECONOMICS:Themes of Microeconomics, Theories and Models

- Economics: Another Perspective, Factors of Production

- REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve

- Changes in Market Equilibrium:Market for College Education

- Elasticities of supply and demand:The Demand for Gasoline

- Consumer Behavior:Consumer Preferences, Indifference curves

- CONSUMER PREFERENCES:Budget Constraints, Consumer Choice

- Note it is repeated:Consumer Preferences, Revealed Preferences

- MARGINAL UTILITY AND CONSUMER CHOICE:COST-OF-LIVING INDEXES

- Review of Consumer Equilibrium:INDIVIDUAL DEMAND, An Inferior Good

- Income & Substitution Effects:Determining the Market Demand Curve

- The Aggregate Demand For Wheat:NETWORK EXTERNALITIES

- Describing Risk:Unequal Probability Outcomes

- PREFERENCES TOWARD RISK:Risk Premium, Indifference Curve

- PREFERENCES TOWARD RISK:Reducing Risk, The Demand for Risky Assets

- The Technology of Production:Production Function for Food

- Production with Two Variable Inputs:Returns to Scale

- Measuring Cost: Which Costs Matter?:Cost in the Short Run

- A Firms Short-Run Costs ($):The Effect of Effluent Fees on Firms Input Choices

- Cost in the Long Run:Long-Run Cost with Economies & Diseconomies of Scale

- Production with Two Outputs--Economies of Scope:Cubic Cost Function

- Perfectly Competitive Markets:Choosing Output in Short Run

- A Competitive Firm Incurring Losses:Industry Supply in Short Run

- Elasticity of Market Supply:Producer Surplus for a Market

- Elasticity of Market Supply:Long-Run Competitive Equilibrium

- Elasticity of Market Supply:The Industrys Long-Run Supply Curve

- Elasticity of Market Supply:Welfare loss if price is held below market-clearing level

- Price Supports:Supply Restrictions, Import Quotas and Tariffs

- The Sugar Quota:The Impact of a Tax or Subsidy, Subsidy

- Perfect Competition:Total, Marginal, and Average Revenue

- Perfect Competition:Effect of Excise Tax on Monopolist

- Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power

- The Social Costs of Monopoly Power:Price Regulation, Monopsony

- Monopsony Power:Pricing With Market Power, Capturing Consumer Surplus

- Monopsony Power:THE ECONOMICS OF COUPONS AND REBATES

- Airline Fares:Elasticities of Demand for Air Travel, The Two-Part Tariff

- Bundling:Consumption Decisions When Products are Bundled

- Bundling:Mixed Versus Pure Bundling, Effects of Advertising

- MONOPOLISTIC COMPETITION:Monopolistic Competition in the Market for Colas and Coffee

- OLIGOPOLY:Duopoly Example, Price Competition

- Competition Versus Collusion:The Prisoners Dilemma, Implications of the Prisoners

- COMPETITIVE FACTOR MARKETS:Marginal Revenue Product

- Competitive Factor Markets:The Demand for Jet Fuel

- Equilibrium in a Competitive Factor Market:Labor Market Equilibrium

- Factor Markets with Monopoly Power:Monopoly Power of Sellers of Labor