|

Microeconomics

ECO402

VU

Lesson

20

Cost in

the Long Run

Cost

minimization with Varying

Output Levels

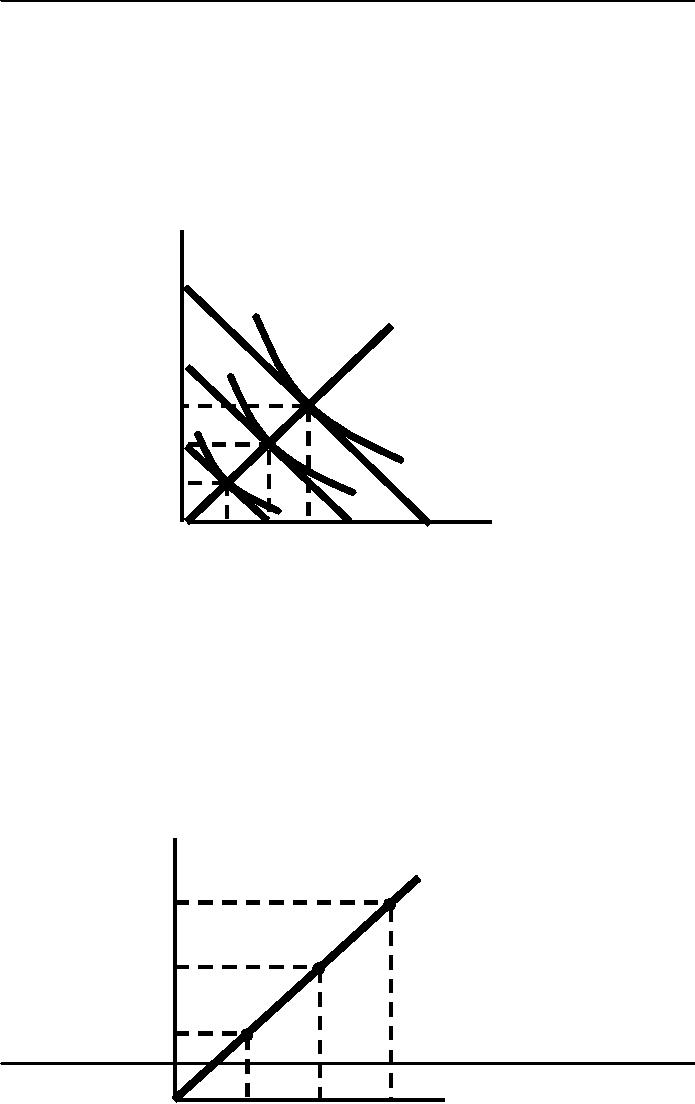

A firm's expansion path

shows the minimum cost

combinations of labor and

capital at each

level

of output.

A

Firm's

The

expansion path

illustrates

Capital

the

least-cost combinations of

per

labor

and capital that can

be

year

used

to produce each level

of

output

in the long-run.

150

$3000

Isocost Line

Expansion

Path

$2000

Isocost

Line

100

C

75

B

50

300

Unit Isoquant

A

25

200

Unit

Isoquan

Labor

per year

100

150

200

300

50

Expansion

Path

Cost

per

Year

Expansion

Path

F

3000

E

A

firm's Long

2000

run

total

cost

curve

D

1000

100

Output,

Units/yr

100

200

300

Microeconomics

ECO402

VU

Long-Run

Versus Short-Run Cost

Curves

What

happens to average costs

when both inputs are

variable (long run) versus

only having

one

input that is variable

(short run)?

101

Microeconomics

ECO402

VU

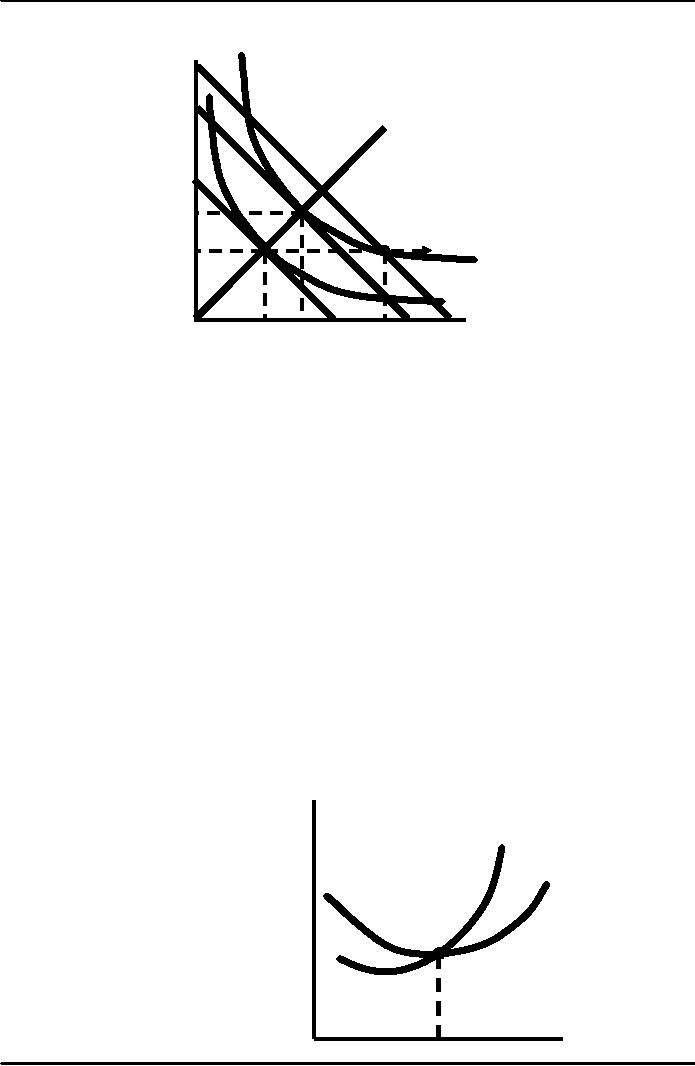

The

Inflexibility of Short-Run

Production

E

Capital

The

long-run expansion

per

path

is drawn as before..

year

C

Long-Run

Expansion

Path

A

K2

Short-Run

P

Expansion

Path

K1

Q2

Q1

L2

L1

L3 D

B

F

Labor

per year

Long-Run

Average Cost (LAC)

Constant Returns to

Scale

·If

input is doubled, output

will double and average

cost is constant at all

levels of output.

Increasing Returns to

Scale

·If

input is doubled, output

will more than double and

average cost decreases at

all levels

of

output.

Decreasing Returns to

Scale

·If

input is doubled, the increase in

output is less than twice as

large and average

cost

increases

with output.

In the long-run:

·Firms

experience increasing and

decreasing returns to scale

and therefore long-run

average

cost is "U" shaped.

Long-run marginal cost

leads long-run average

cost:

·If

LMC < LAC, LAC will

fall

·If

LMC > LAC, LAC will

rise

·Therefore,

LMC = LAC at the minimum of

LAC

Long-Run

Average and Marginal

Cost

Cost($

per

unit

LM

of

output

LA

A

Output

102

Microeconomics

ECO402

VU

Question

What is the relationship

between long-run average

cost and long-run marginal

cost when

long-run

average cost is

constant?

Economies

and Diseconomies of Scale

Economies of Scale

·Increase

in output is greater than the increase in

inputs.

Diseconomies of

Scale

·Increase

in output is less than the increase in

inputs.

Measuring

Economies of Scale

Ec =

Cost

-

output

elasticity

=

%Δ in

cost from a 1%

increase

in

output

Therefore,

the following is true:

EC< 1: MC < AC

·Average cost indicate

decreasing economies of

scale

EC = 1: MC = AC

·Average cost indicate

constant economies of

scale

EC > 1: MC > AC

·Average cost indicate

increasing economies of

scale

The

Relationship Between Short-Run

and Long-Run Cost

We will use short

and long-run cost to

determine the optimal plant

size

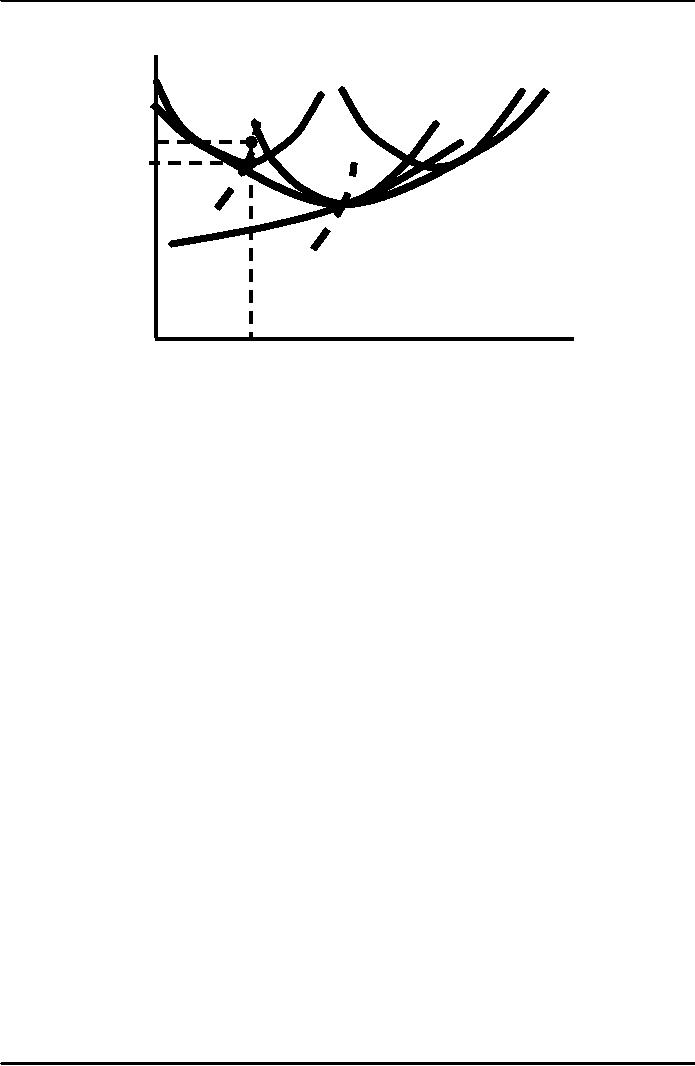

Long-Run

Cost with Constant Returns

to Scale

Cost

With

many plant sizes with SAC =

$10

($

per unit

the

LAC = LMC and is a straight

line

of

output

SAC1

SAC2

SAC3

SMC2

SMC3

SMC

LAC

=

LMC

Q1

Q2

Q3

Output

Observation

The optimal plant

size will depend on the

anticipated output (e.g. Q1 choose SAC1,etc).

The long-run average

cost curve is the envelope

of the firm's short-run

average cost curves.

Question

What would happen to

average cost if an output

level other than that

shown is chosen?

103

Microeconomics

ECO402

VU

Long-Run

Cost with Economies &

Diseconomies of Scale

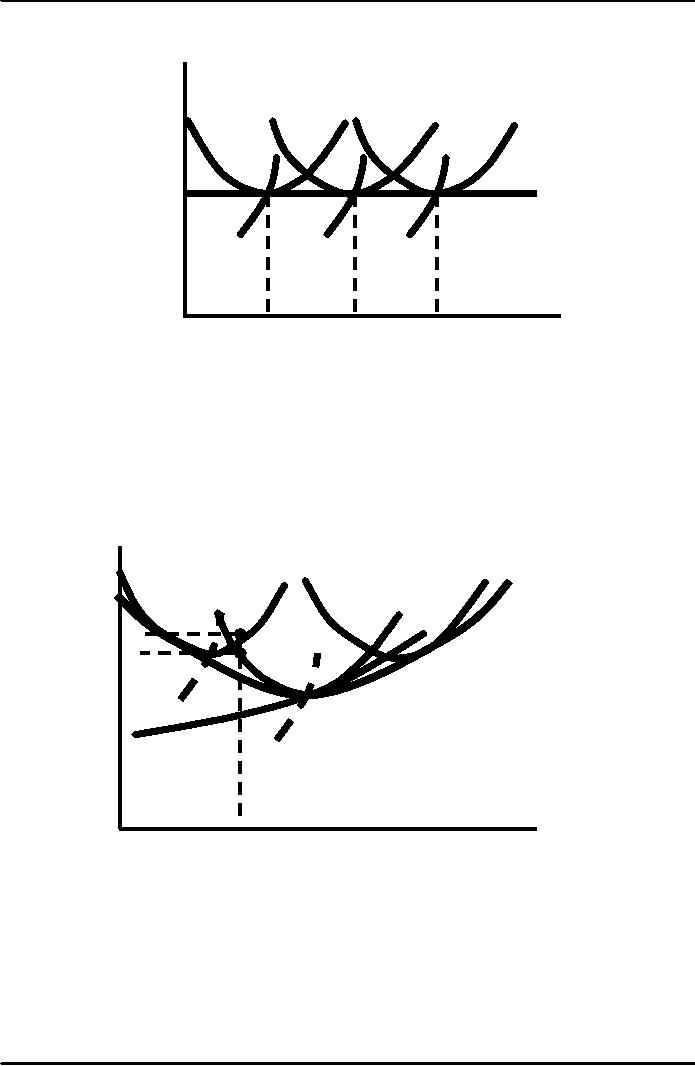

Cost

SAC1

($

per unit

LAC

SAC3

of

output

SAC2

A

$10

$8

B

If

the output is Q1 a

SMC1

SMC3

manager

would

chose the small

LMC

SMC2

plant

SAC1 and SAC

$8.

Q1

Output

What

is the firms' long-run cost

curve?

Firms can change

scale to change output in

the long-run.

The long-run cost

curve is the dark blue

portion of the SAC curve

which represents the

minimum

cost for any level of

output.

Observations

The LAC does

not include the minimum

points of small and large

size plants? Why

not?

LMC is not the envelope of

the short-run marginal cost.

Why not?

Measuring

Economies of Scale

Ec = (ΔC/

C) /(ΔQ/

Q)

Ec =(ΔC/ ΔQ)/(C/

Q) = M /A

C C

Therefore,

the following is

true:

EC< 1: MC

< AC

·

Average

cost indicate decreasing

economies of scale

EC = 1: MC =

AC

·

Average

cost indicate constant

economies of scale

EC > 1: MC

> AC

·

Average

cost indicate increasing

economies of scale

The

Relationship Between Short-Run

and Long-Run Cost

We will use

short and long-run cost to

determine the optimal plant

size

104

Microeconomics

ECO402

VU

Long-Run

Cost with Constant Returns

to Scale

Cost

With

many plant sizes with SAC =

$10

($

per unit

the

LAC = LMC and is a straight

line

of

output

SAC1

SAC2

SAC3

SMC2

SMC3

SMC

LAC

=

LMC

Q1

Q2

Q3

Output

Observation

The

optimal plant size will

depend on the anticipated

output (e.g. Q1 choose

SAC1,etc).

The

long-run average cost curve

is the envelope of the

firm's short-run average

cost

curves.

Question

What

would happen to average cost

if an output level other

than that shown is

chosen?

Long-Run

Cost with Economies &

Diseconomies of Scale

Cost

SAC1

($

per unit

LAC

SAC3

of

output

SAC2

A

$10

$8

B

If

the output is Q1 a

manager

SMC1

SMC3

would

chose the small

plant

LMC

SAC1 and SAC

$8.

SMC2

Q1

Output

What

is the firms' long-run cost

curve?

Firms can

change scale to change

output in the

long-run.

The long-run

cost curve is the dark

blue portion of the SAC

curve which represents

the

minimum

cost for any level of

output.

Observations

The LAC

does not include the

minimum points of small and

large size plants? Why

not?

LMC is not the

envelope of the short-run

marginal cost. Why

not?

105

Table of Contents:

- ECONOMICS:Themes of Microeconomics, Theories and Models

- Economics: Another Perspective, Factors of Production

- REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve

- Changes in Market Equilibrium:Market for College Education

- Elasticities of supply and demand:The Demand for Gasoline

- Consumer Behavior:Consumer Preferences, Indifference curves

- CONSUMER PREFERENCES:Budget Constraints, Consumer Choice

- Note it is repeated:Consumer Preferences, Revealed Preferences

- MARGINAL UTILITY AND CONSUMER CHOICE:COST-OF-LIVING INDEXES

- Review of Consumer Equilibrium:INDIVIDUAL DEMAND, An Inferior Good

- Income & Substitution Effects:Determining the Market Demand Curve

- The Aggregate Demand For Wheat:NETWORK EXTERNALITIES

- Describing Risk:Unequal Probability Outcomes

- PREFERENCES TOWARD RISK:Risk Premium, Indifference Curve

- PREFERENCES TOWARD RISK:Reducing Risk, The Demand for Risky Assets

- The Technology of Production:Production Function for Food

- Production with Two Variable Inputs:Returns to Scale

- Measuring Cost: Which Costs Matter?:Cost in the Short Run

- A Firms Short-Run Costs ($):The Effect of Effluent Fees on Firms Input Choices

- Cost in the Long Run:Long-Run Cost with Economies & Diseconomies of Scale

- Production with Two Outputs--Economies of Scope:Cubic Cost Function

- Perfectly Competitive Markets:Choosing Output in Short Run

- A Competitive Firm Incurring Losses:Industry Supply in Short Run

- Elasticity of Market Supply:Producer Surplus for a Market

- Elasticity of Market Supply:Long-Run Competitive Equilibrium

- Elasticity of Market Supply:The Industrys Long-Run Supply Curve

- Elasticity of Market Supply:Welfare loss if price is held below market-clearing level

- Price Supports:Supply Restrictions, Import Quotas and Tariffs

- The Sugar Quota:The Impact of a Tax or Subsidy, Subsidy

- Perfect Competition:Total, Marginal, and Average Revenue

- Perfect Competition:Effect of Excise Tax on Monopolist

- Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power

- The Social Costs of Monopoly Power:Price Regulation, Monopsony

- Monopsony Power:Pricing With Market Power, Capturing Consumer Surplus

- Monopsony Power:THE ECONOMICS OF COUPONS AND REBATES

- Airline Fares:Elasticities of Demand for Air Travel, The Two-Part Tariff

- Bundling:Consumption Decisions When Products are Bundled

- Bundling:Mixed Versus Pure Bundling, Effects of Advertising

- MONOPOLISTIC COMPETITION:Monopolistic Competition in the Market for Colas and Coffee

- OLIGOPOLY:Duopoly Example, Price Competition

- Competition Versus Collusion:The Prisoners Dilemma, Implications of the Prisoners

- COMPETITIVE FACTOR MARKETS:Marginal Revenue Product

- Competitive Factor Markets:The Demand for Jet Fuel

- Equilibrium in a Competitive Factor Market:Labor Market Equilibrium

- Factor Markets with Monopoly Power:Monopoly Power of Sellers of Labor