|

THE MONETARY BASE:Changing the Size and Composition of the Balance Sheet |

| << MEETING THE CHALLENGE: CREATING A SUCCESSFUL CENTRAL BANK |

| DEPOSIT CREATION IN A SINGLE BANK:Types of Reserves >> |

Money

& Banking MGT411

VU

Lesson

33

THE

MONETARY BASE

Currency

in the hands of the public and the

reserves of the banking system

are the two

components

of the monetary base, also

called high-powered

money.

Bank

Reserves = Vault Cash plus

Deposits at the central bank

The

central bank can control the

size of the monetary base and

therefore the quantity of

money

Changing

the Size and Composition of

the Balance Sheet

The

central bank controls the

size of its balance sheet.

Policymakers can enlarge or reduce

their

assets

and liabilities at

will

The

central bank can buy

things, like a bond, and

create liabilities to pay

for them. It can

increase

the size of its balance

sheet as much as it wants.

There

are four specific types of

transactions which can

affect the balance sheets of

both the

central

bank and the banking

system:

An

open market operation, in which the

central bank buys or sells a

security;

A

foreign exchange intervention, in which

the central bank buys or sells

foreign currency

reserves;

The

central bank's extension of a

discount loan to a commercial

bank;

The

decision by an individual to withdraw

cash from a bank

Open

market operations, foreign exchange

interventions, and discount loans, all

affect the size

of

the central bank's balance

sheet

They

change the size of the monetary

base;

Cash

withdrawals by the public create

shifts among the different components of

the monetary

base,

changing the composition of the central

bank's balance sheet but

leaving its size

unaffected

One

simple rule will help in

understanding the impact of each of

these four transactions on

the

central

bank's balance sheet:

When

the value of an asset on the balance

sheet increases, either the

value of another asset

decreases

(so that the net change is zero) or

the value of a liability

rises by the same

amount

(and

similarly for an increase in

liabilities)

Open

Market Operations

OMO

is when the central bank buys or

sells securities in financial

markets

These

purchases and sales have a

straightforward impact on the central

bank's balance sheet:

Its

assets and liabilities increase by the

amount of a purchase, and the monetary

base increases

by

the same amount

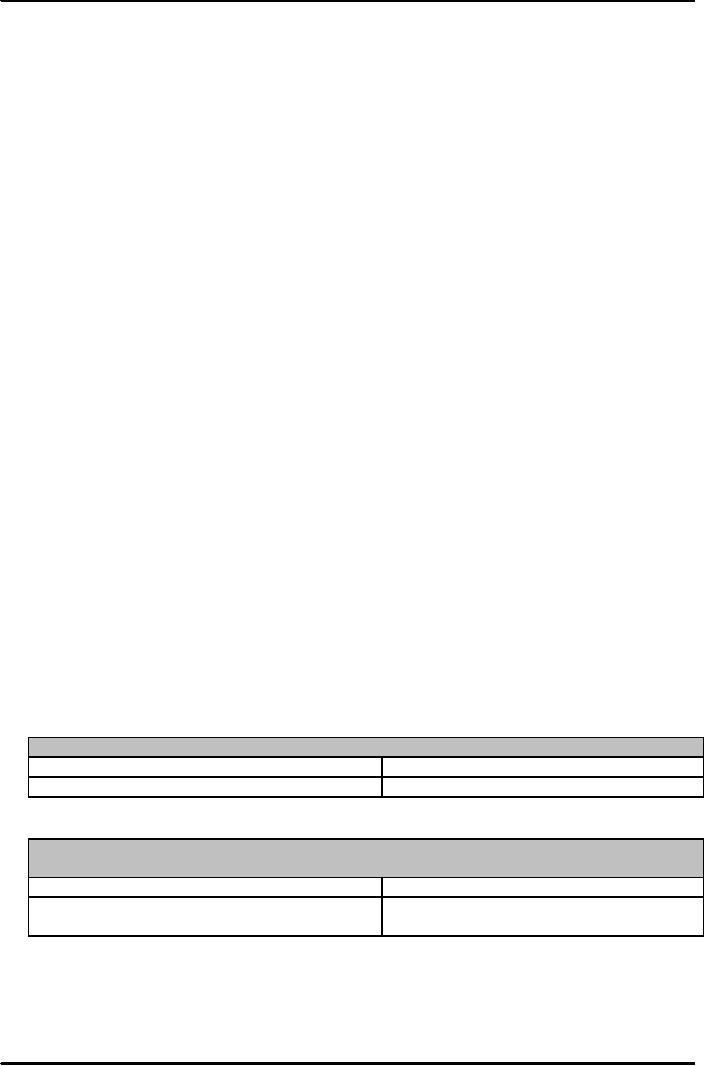

Table:

Change in the Central Bank's

Balance sheet following

purchase of a Treasury

Bond

Assets

Liabilities

Securities(Treasury

Bond)

+$1billion

Reserves

+$1billion

Table:

Change in the Banking

system's balance sheet

following the Central Bank's

purchase

of

a Treasury Bond

Assets

Liabilities

Reserves

+$1billion

Securities

(U.S. Treasury Bond)

-$1billion

In

terms of the banking system's

balance sheet, the purchase

has no effect on the liabilities,

and

results

in two counterbalancing changes on the

asset side, so the net effect there is

zero

For

an open market sale, the effects would be

the same but in the opposite

direction

102

Money

& Banking MGT411

VU

Foreign

Exchange Intervention

The

impact of a foreign exchange

purchase is almost identical to that of

an open market

purchase:

The

central bank's assets and

liabilities increase by the same amount,

as does the monetary

base.

If

the central bank buys from a

commercial bank, the impact

again is like the open

market

purchase,

except the assets involved are

different.

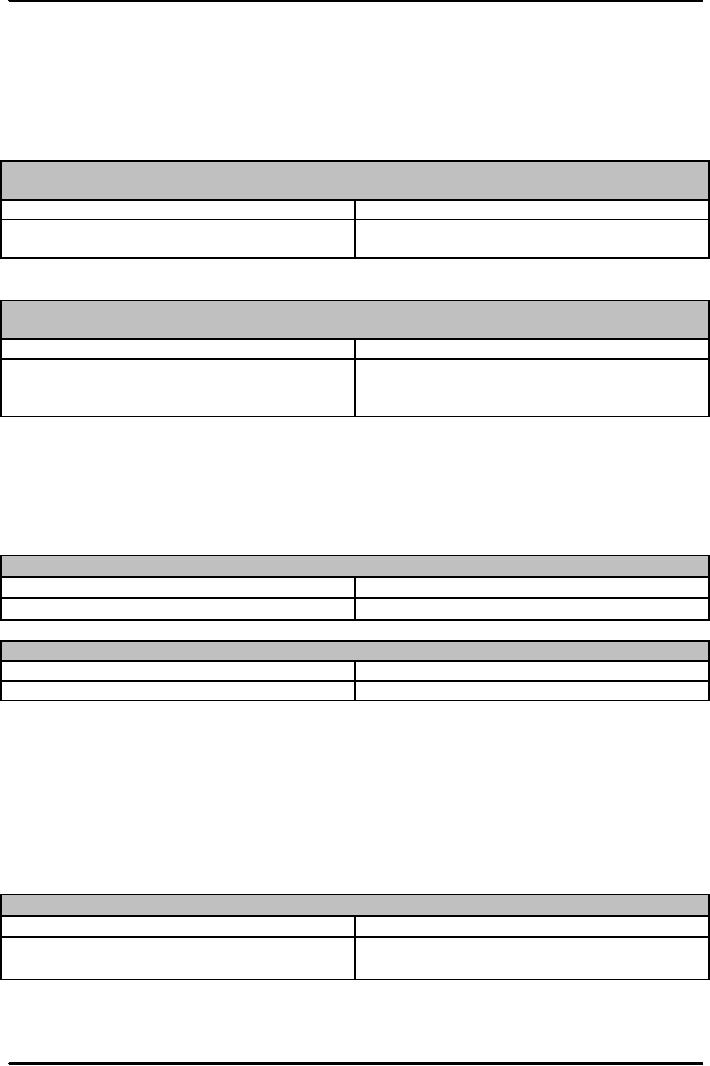

Table:

change in the Central bank's

Balance sheet following

purchase of Euro-denominated

German

Government Bonds

Assets

Liabilities

Foreign

exchange reserves

+$1billion

Reserves

+$1billion

(German

government bonds in

euros)

Table:

Change in the Banking

system's Balance sheet

following the Central bank's

purchase of

Euro-denominated

German Government Bonds

Assets

Liabilities

Reserves

+$1billion

Securities

-$1billion

(German

government bonds)

Discount

Loans

The

central bank does not

force commercial banks to

borrow money; the banks ask

for loans

and

must provide collateral,

usually a Treasury

bond.

When

the central bank makes a

loan it creates an asset and

a matching increase in its

reserve

liabilities.

Table:

Change in the Central Bank's

Balance sheet following a Discount

Loan

Assets

Liabilities

Discount

loans

+$100million

Reserves

+$100million

Table:

Change in the Banking

System's Balance Sheet

following a Discount Loan

Assets

Liabilities

Reserves

+$100million

Discount

loans

-$100million

The

extension of credit to the banking

system raises the level of

reserves and expands the

monetary

base.

The

banking system balance sheet

shows an increase in assets

(reserves) and an increase in

liabilities

(the loan).

Cash

Withdrawal

Cash

withdrawals affect only the

composition, not the size, of the

monetary base.

When

people withdraw cash they

force a shift from reserves

to currency on the central

bank's

balance

sheet.

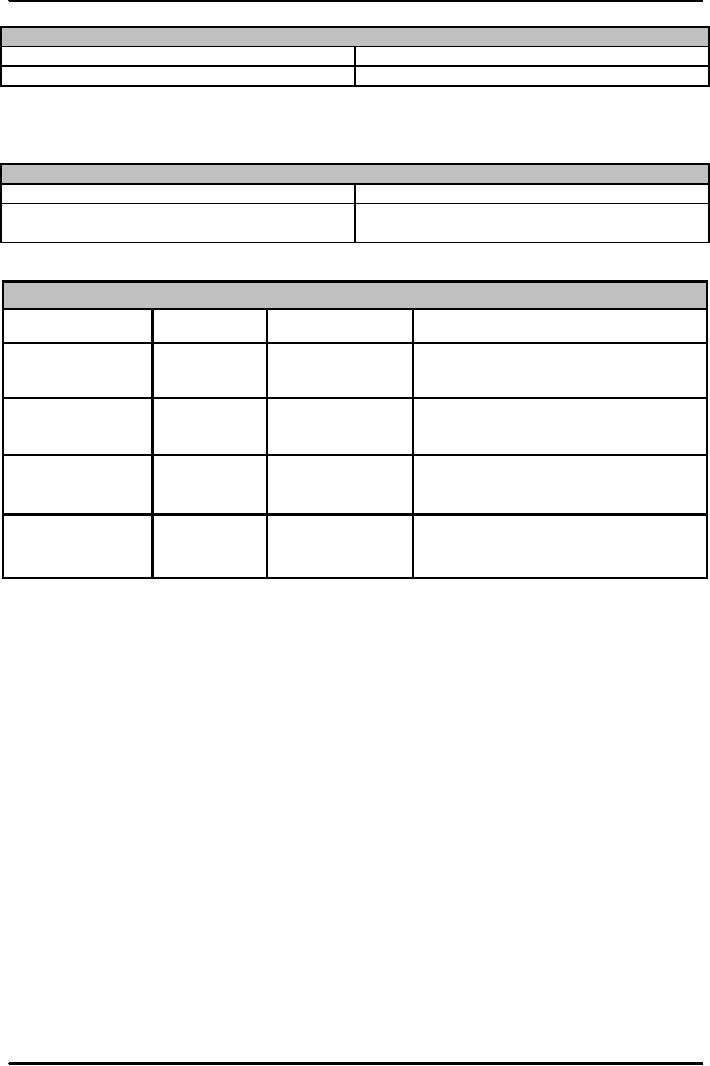

Table:

Change in the Nonbank Public's

Balance Sheet following a

Cash Withdrawal

Assets

Liabilities

Currency

+$100

Checkable

deposits

-$100

The

withdrawal reduces the banking

system's reserves, which is a

decrease in its assets, and

if

the

funds come from a checking

account, there is a matching decrease in

liabilities.

103

Money

& Banking MGT411

VU

Table:

Change in the Banking

system's Balance sheet

following a Cash Withdrawal

Assets

Liabilities

Reserves

-$100

Checkable

deposits

-$100

On

the central bank's balance

sheet both currency and

reserves are liabilities, so there is

just a

change

between the two with a net effect of

zero.

Table:

Change in the Central Bank's

Balance Sheet following a Cash

Withdrawal

Assets

Liabilities

Currency

+$100

Reserves

-$100

Changes

in Size and Composition of Central

Bank's Balance Sheet and

Monetary Base

Transaction

Initiated

by

Typical

action

Impact

Open

market

Central

bank

Purchase

of Treasury Increases reserves, the

size of central

bank's

operation

bond

balance

sheet and Monetary

base

Foreign

Exchange

Central

bank

Purchase

of foreign Increases reserves, the

size of central

bank's

Intervention

govt.

bonds

balance

sheet and Monetary

base

Discount

Loans

Commercial

Extension

of loan to Increases reserves, the

size of central

bank's

bank

commercial

bank

balance

sheet and Monetary

base

Cash

withdrawals

Nonbank

public Withdrawal of

cash

Decreases

reserves and increases

currency,

from

ATM

leaving

size of central bank's

balance sheet

and

Monetary base unchanged

104

Table of Contents:

- TEXT AND REFERENCE MATERIAL & FIVE PARTS OF THE FINANCIAL SYSTEM

- FIVE CORE PRINCIPLES OF MONEY AND BANKING:Time has Value

- MONEY & THE PAYMENT SYSTEM:Distinctions among Money, Wealth, and Income

- OTHER FORMS OF PAYMENTS:Electronic Funds Transfer, E-money

- FINANCIAL INTERMEDIARIES:Indirect Finance, Financial and Economic Development

- FINANCIAL INSTRUMENTS & FINANCIAL MARKETS:Primarily Stores of Value

- FINANCIAL INSTITUTIONS:The structure of the financial industry

- TIME VALUE OF MONEY:Future Value, Present Value

- APPLICATION OF PRESENT VALUE CONCEPTS:Compound Annual Rates

- BOND PRICING & RISK:Valuing the Principal Payment, Risk

- MEASURING RISK:Variance, Standard Deviation, Value at Risk, Risk Aversion

- EVALUATING RISK:Deciding if a risk is worth taking, Sources of Risk

- BONDS & BONDS PRICING:Zero-Coupon Bonds, Fixed Payment Loans

- YIELD TO MATURIRY:Current Yield, Holding Period Returns

- SHIFTS IN EQUILIBRIUM IN THE BOND MARKET & RISK

- BONDS & SOURCES OF BOND RISK:Inflation Risk, Bond Ratings

- TAX EFFECT & TERM STRUCTURE OF INTEREST RATE:Expectations Hypothesis

- THE LIQUIDITY PREMIUM THEORY:Essential Characteristics of Common Stock

- VALUING STOCKS:Fundamental Value and the Dividend-Discount Model

- RISK AND VALUE OF STOCKS:The Theory of Efficient Markets

- ROLE OF FINANCIAL INTERMEDIARIES:Pooling Savings

- ROLE OF FINANCIAL INTERMEDIARIES (CONTINUED):Providing Liquidity

- BANKING:The Balance Sheet of Commercial Banks, Assets: Uses of Funds

- BALANCE SHEET OF COMMERCIAL BANKS:Bank Capital and Profitability

- BANK RISK:Liquidity Risk, Credit Risk, Interest-Rate Risk

- INTEREST RATE RISK:Trading Risk, Other Risks, The Globalization of Banking

- NON- DEPOSITORY INSTITUTIONS:Insurance Companies, Securities Firms

- SECURITIES FIRMS (Continued):Finance Companies, Banking Crisis

- THE GOVERNMENT SAFETY NET:Supervision and Examination

- THE GOVERNMENT'S BANK:The Bankers' Bank, Low, Stable Inflation

- LOW, STABLE INFLATION:High, Stable Real Growth

- MEETING THE CHALLENGE: CREATING A SUCCESSFUL CENTRAL BANK

- THE MONETARY BASE:Changing the Size and Composition of the Balance Sheet

- DEPOSIT CREATION IN A SINGLE BANK:Types of Reserves

- MONEY MULTIPLIER:The Quantity of Money (M) Depends on

- TARGET FEDERAL FUNDS RATE AND OPEN MARKET OPERATION

- WHY DO WE CARE ABOUT MONETARY AGGREGATES?The Facts about Velocity

- THE FACTS ABOUT VELOCITY:Money Growth + Velocity Growth = Inflation + Real Growth

- THE PORTFOLIO DEMAND FOR MONEY:Output and Inflation in the Long Run

- MONEY GROWTH, INFLATION, AND AGGREGATE DEMAND

- DERIVING THE MONETARY POLICY REACTION CURVE

- THE AGGREGATE DEMAND CURVE:Shifting the Aggregate Demand Curve

- THE AGGREGATE SUPPLY CURVE:Inflation Shocks

- EQUILIBRIUM AND THE DETERMINATION OF OUTPUT AND INFLATION

- SHIFTS IN POTENTIAL OUTPUT AND REAL BUSINESS CYCLE THEORY