|

Money

& Banking MGT411

VU

Lesson

18

THE

LIQUIDITY PREMIUM

THEORY

Bonds

Liquidity

Premium Theory

Stocks

Essential

Characteristics

Process

Measuring

Level of a Stock

Market

Valuing

Stocks

The

Liquidity Premium

Theory

Risk

is the key to understanding the slope of the

yield curve

The

yield curve's upward slope is due to

long-term bonds being

riskier than

short-term

bonds

Bondholders

face both inflation and interest-rate.

The longer the term the greater

the

inflation

and interest-rate risk

Inflation

risk increases over time

because investors, who care

about the real return,

must

forecast

inflation over longer

periods.

Interest-rate

risk arises when an

investor's horizon and the bond's

maturity do not match.

If

holders

of long-term bonds need to

sell them before maturity and interest

rates have

increased,

the bonds will lose

value

Including

risk in the model means that

we can think of yield as

having two parts:

Risk-free

and

Risk

premium

i1t +

i1et

+1 +

i1et

+

2

+

....

+

i1et

+

n

-1

int =

rp

n +

n

Pure

expectations theory

Risk

premium

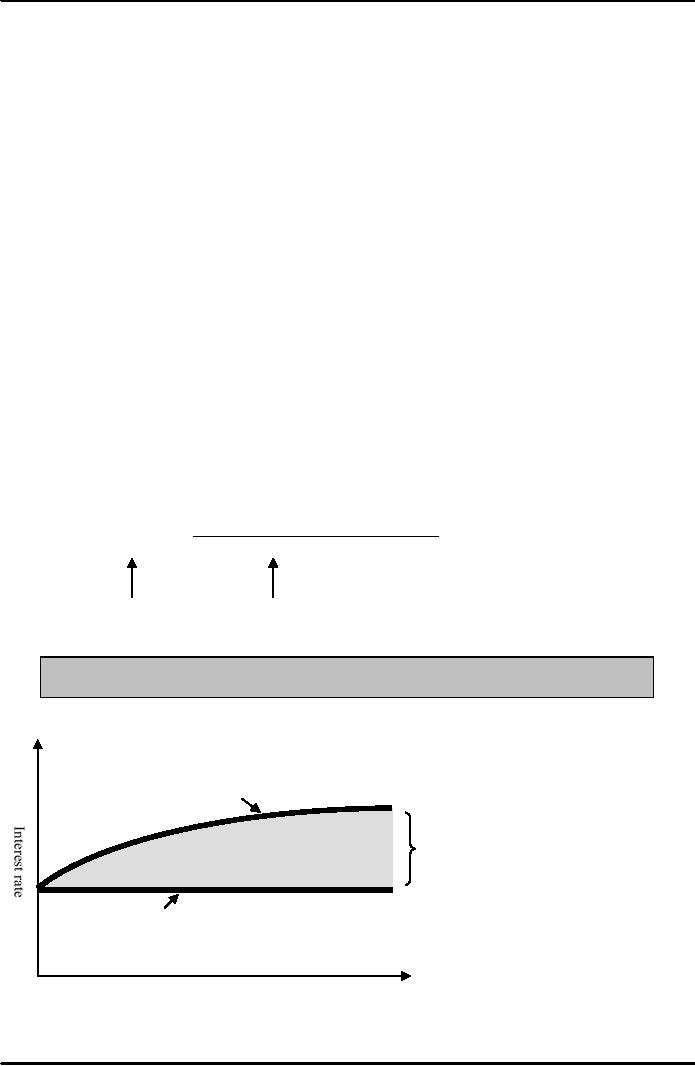

Figure:

Relationship between the Liquidity

Premium and Expectations

Theories

Liquidity

Premium Theory Yield

curve

Liquidity

premium

Expectations

Theory Yield curve

(If

short term interest rates

are expected to

remain

constant)

Time

to maturity

59

Money

& Banking MGT411

VU

Again,

we arrive at the same three conclusions

about the term structure of interest

rates

Interest

rates of different maturities

tend to move

together.

Yields

on short-term bonds are more volatile

than those on long-term

bonds.

Long-term

yields tend to be higher

than short-term yields

Stocks:

An Introduction

Stocks

provide a key instrument for

holding personal wealth as well as a

way to diversify,

spreading

and reducing the risks that we

face

For

companies, they are one of several ways

to obtain financing.

Additionally,

Stocks

and stock markets are one of

the central links between the financial

world and the real

economy.

Stock

prices are fundamental to the

functioning of a market-based

economy

They

indicate the value of the companies

that issued the stocks

and,

They

allocate scarce investment

resources

The

firms deemed most valuable

in the marketplace for stocks are the

ones that will be able

to

obtain

financing for growth. When

resources flow to their most

valued uses, the economy

operates

more efficiently

Most

people see stock market as a place where

fortunes are easily made or

lost, and they

recoil

at

its unfathomable booms and

busts.

Great

American Depression (1929)

Post-September

11, 2001 scenario

Pakistan

stock market on roller-coaster-ride

(March 2005)

What

happens in reality?

Stock

prices tend to rise steadily and

slowly, and

Collapse

rarely when normal market

mechanisms are out of

alignment

For

most people the experience of losing or

gaining wealth suddenly is more memorable

than

the

experience of making it gradually.

By

being preoccupied with the potential

short-term losses associated with

crashes, we lose

sight

of

the gains we could realize if we took a

longer-term view

Essential

Characteristics of Common

Stock

Stocks,

also known as common stock or equity,

are shares in a firm's

ownership

From

their early days, stocks had

two important characteristics

that today are taken

for granted:

The

shares are issued in small

denominations and

The

shares are transferable

Until

recently, stockowners received a

certificate from the issuing

company, but now it is

a

computerized

process where the shares are registered

in the names of brokerage firms

that hold

them

on the owner's behalf

The

ownership of common stock conveys a number of

rights

A

stockholder is entitled to participate in

the shares of the enterprise, but this is

a residual claim

i.e.

meaning the leftovers after

all other creditors have been

paid.

Stockholders

also have limited

liability,

Even

if a company fails, the maximum amount

that the stockholder can

lose is the initial

investment

Stockholders

are entitled to vote at the

firm's annual meeting

including voting to elect

(or

remove)

the firm's board of directors

Following

are some salient features of

stock trading

1.

An

individual share represents

only a small fraction of the

value of the company that

issued

it

2.

A

large number of shares are

outstanding

3.

Prices

of individual shares are

low, allowing individuals to

make relatively small

investments

60

Money

& Banking MGT411

VU

4.

As

residual claimants, stockholders receive the proceeds

of a firm's activities only

after

all

other creditors have been

paid

5.

Because

of limited liability, investor's

losses cannot exceed the price

they paid for the

stock;

and

6.

Shareholders

can replace managers who are

doing a bad job

Measuring

the Level of the Stock

Market

Stocks

are one way in which we

choose to hold our wealth,

so when stock values rise we get

richer

and when they fall we get

poorer

These

changes affect our

consumption and saving patterns, causing general

economic activity to

fluctuate

We

need to understand the dynamics of the stock market,

in order to

Manage

our personal finances and

See

the connections between stock values and economic

conditions

Stock

market indexes

Designed

to give us a sense of the extent to

which stock prices are going

up or down

Tell

us both how much the value

of an average stock has changed, and

how much total

wealth

has

gone up or down

Provide

benchmarks for performance of money

managers, comparing how they

have done to the

market

as a whole

Every

major country in the world

has a stock market, and each

of these markets has an

index

For

the most part, these are

value-weighted indices

To

analyze the performance of these different

markets it is useful to look at

percentage changes,

but

percentage change isn't

everything

The

Dow Jones Industrial

Average

The

Standard & Poor's 500

Index

NASDAQ

Composite index

Financial

Times Stock Exchange 100

Index

Hang

Seng 100

Nikkei

225

KSE

100 Index

The

KSE100

It

contains a representative sample of common stock that

trade on the Karachi Stock

Exchange.

The

KSE stocks that comprise the

index have a total market

value of around Rs. 1,197

Billion

compared

to total market value of Rs.

1,365 Billion for over

679 stocks listed on the

Karachi

Stock

Exchange.

This

means that the KSE100 Index

represents 88 percent of the total market

capitalization of the

Karachi

Stock Exchange, as of February,

2004

61

Table of Contents:

- TEXT AND REFERENCE MATERIAL & FIVE PARTS OF THE FINANCIAL SYSTEM

- FIVE CORE PRINCIPLES OF MONEY AND BANKING:Time has Value

- MONEY & THE PAYMENT SYSTEM:Distinctions among Money, Wealth, and Income

- OTHER FORMS OF PAYMENTS:Electronic Funds Transfer, E-money

- FINANCIAL INTERMEDIARIES:Indirect Finance, Financial and Economic Development

- FINANCIAL INSTRUMENTS & FINANCIAL MARKETS:Primarily Stores of Value

- FINANCIAL INSTITUTIONS:The structure of the financial industry

- TIME VALUE OF MONEY:Future Value, Present Value

- APPLICATION OF PRESENT VALUE CONCEPTS:Compound Annual Rates

- BOND PRICING & RISK:Valuing the Principal Payment, Risk

- MEASURING RISK:Variance, Standard Deviation, Value at Risk, Risk Aversion

- EVALUATING RISK:Deciding if a risk is worth taking, Sources of Risk

- BONDS & BONDS PRICING:Zero-Coupon Bonds, Fixed Payment Loans

- YIELD TO MATURIRY:Current Yield, Holding Period Returns

- SHIFTS IN EQUILIBRIUM IN THE BOND MARKET & RISK

- BONDS & SOURCES OF BOND RISK:Inflation Risk, Bond Ratings

- TAX EFFECT & TERM STRUCTURE OF INTEREST RATE:Expectations Hypothesis

- THE LIQUIDITY PREMIUM THEORY:Essential Characteristics of Common Stock

- VALUING STOCKS:Fundamental Value and the Dividend-Discount Model

- RISK AND VALUE OF STOCKS:The Theory of Efficient Markets

- ROLE OF FINANCIAL INTERMEDIARIES:Pooling Savings

- ROLE OF FINANCIAL INTERMEDIARIES (CONTINUED):Providing Liquidity

- BANKING:The Balance Sheet of Commercial Banks, Assets: Uses of Funds

- BALANCE SHEET OF COMMERCIAL BANKS:Bank Capital and Profitability

- BANK RISK:Liquidity Risk, Credit Risk, Interest-Rate Risk

- INTEREST RATE RISK:Trading Risk, Other Risks, The Globalization of Banking

- NON- DEPOSITORY INSTITUTIONS:Insurance Companies, Securities Firms

- SECURITIES FIRMS (Continued):Finance Companies, Banking Crisis

- THE GOVERNMENT SAFETY NET:Supervision and Examination

- THE GOVERNMENT'S BANK:The Bankers' Bank, Low, Stable Inflation

- LOW, STABLE INFLATION:High, Stable Real Growth

- MEETING THE CHALLENGE: CREATING A SUCCESSFUL CENTRAL BANK

- THE MONETARY BASE:Changing the Size and Composition of the Balance Sheet

- DEPOSIT CREATION IN A SINGLE BANK:Types of Reserves

- MONEY MULTIPLIER:The Quantity of Money (M) Depends on

- TARGET FEDERAL FUNDS RATE AND OPEN MARKET OPERATION

- WHY DO WE CARE ABOUT MONETARY AGGREGATES?The Facts about Velocity

- THE FACTS ABOUT VELOCITY:Money Growth + Velocity Growth = Inflation + Real Growth

- THE PORTFOLIO DEMAND FOR MONEY:Output and Inflation in the Long Run

- MONEY GROWTH, INFLATION, AND AGGREGATE DEMAND

- DERIVING THE MONETARY POLICY REACTION CURVE

- THE AGGREGATE DEMAND CURVE:Shifting the Aggregate Demand Curve

- THE AGGREGATE SUPPLY CURVE:Inflation Shocks

- EQUILIBRIUM AND THE DETERMINATION OF OUTPUT AND INFLATION

- SHIFTS IN POTENTIAL OUTPUT AND REAL BUSINESS CYCLE THEORY