|

Pre-acquisition Reserves |

| << GROUP ACCOUNTS |

| GROUP ACCOUNTS: Minority Interest >> |

Advance

Financial Accounting

(FIN-611)

VU

LESSON

# 37

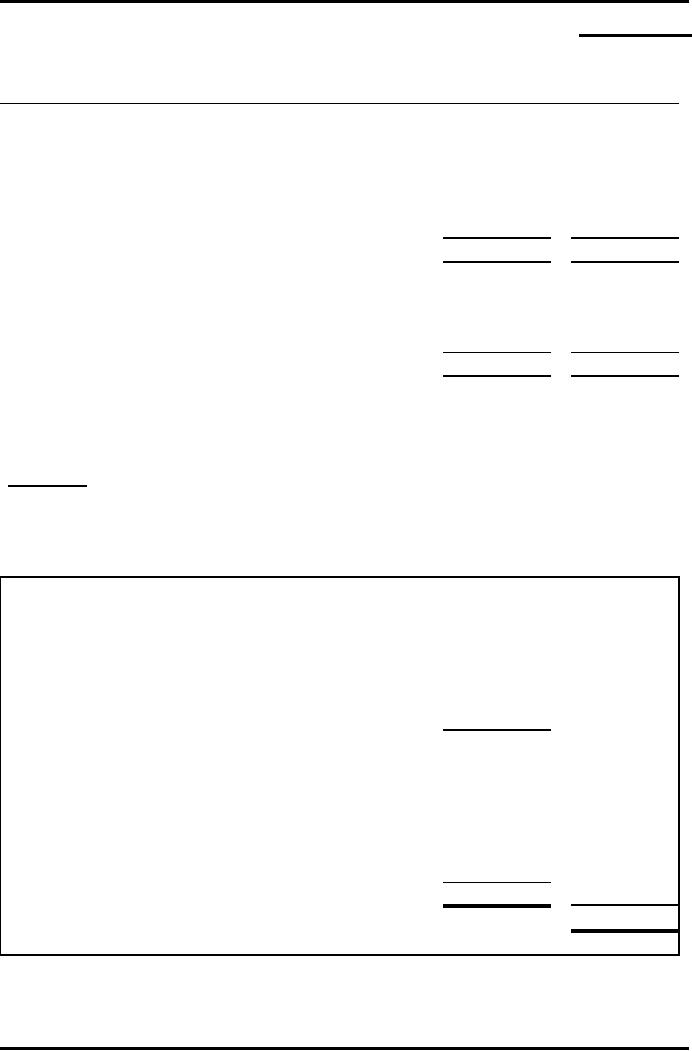

Example

- [ Case iii ] Pre-acquisition

Reserves,

Goodwill

Balance

Sheet as on 31st December

2008

P

S

Rs

Rs

400

Fixed

Assets

1,000

Investment

in S.

500

Current

Assets

400

200

1,900

600

Share

Capital

1,200

300

Reserves

550

150

Current

Liabilities

150

150

1,900

600

The

Parent Co. (P) acquired

100% shares of the

Subsidiary Co. (S) on 1st

January

2008 when

the reserves of the company

were worth Rs100.

Required:

Prepare

the Consolidated Balance

Sheet as on 31/12/2008.

(Ignore

impairment

of Goodwill).

Solution

- [ Case iii ]

Analysis

of Equity of Subsidiary

Company

Pre-

Post-

acquisition

acquisition

Rs

Rs

Share

Capital of subsidiary

company

300

Reserves

of subsidiary company

100

50

400

Calculation

of

Goodwill

Cost of

Investment

500

Pre

acquisition owners' equity of the

subsidiary company

(400)

Goodwill

100

Calculation

of

Group

Reserves

All

reserves of parent

company

550

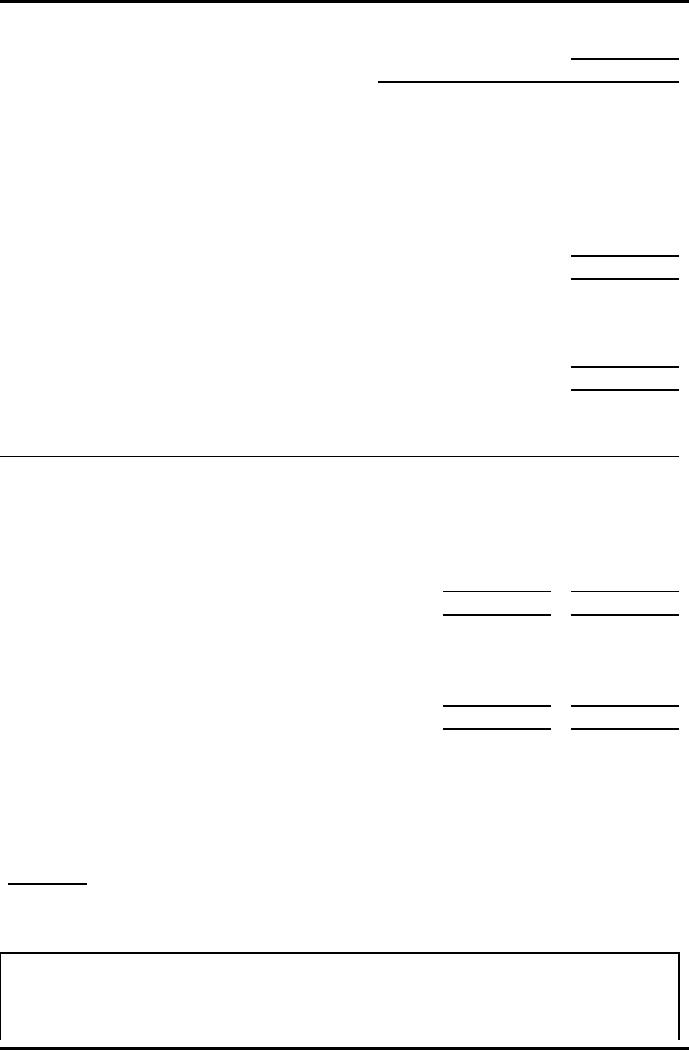

196

Advance

Financial Accounting

(FIN-611)

VU

Post

acquisition of the subsidiary

company

50

600

Consolidated

Balance Sheet

As at 31

December 2008

Rs

Fixed

Assets

1,400

Goodwill

100

Current

Assets

600

2,100

Share

Capital

1,200

Reserves

600

Current

Liabilities

300

2,100

Example

- [ Case iv ] Goodwill Impairment,

Pre-acquisition

Reserves

Balance

Sheet as on 31st December

2008

P

S

Rs

Rs

Fixed

Assets

1,000

400

Investment

in S.

500

Current

Assets

400

200

1,900

600

Share

Capital

1,200

300

Reserves

550

150

Current

Liabilities

150

150

1,900

600

The

Parent Co. (P) acquired

100% shares of the

Subsidiary Co. (S) on 1st

January

2008 when

the reserves of the company

were worth Rs100. Goodwill,

has been

impaired

by Rs. 20

Prepare

the Consolidated Balance

Sheet as at

31/12/2008.

Required:

Solution

- [ Case iv ]

Analysis

of Equity of Subsidiary

Company

Pre-

Post-

acquisition

acquisition

Rs

Rs

197

Advance

Financial Accounting

(FIN-611)

VU

Share

Capital of subsidiary

company

300

Reserves

of subsidiary company

100

50

400

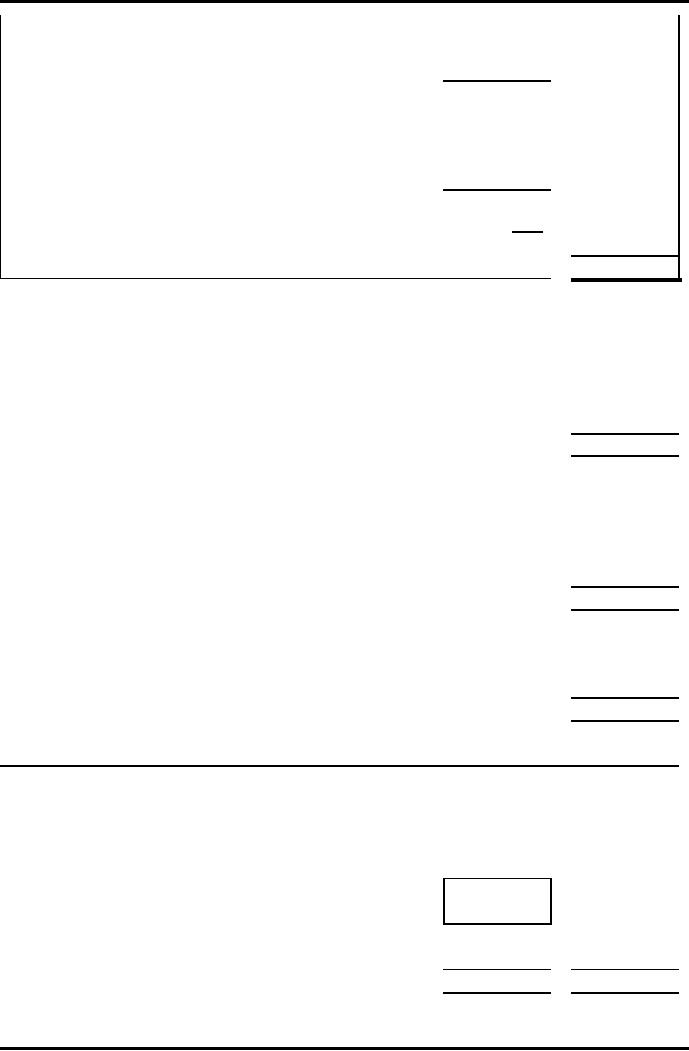

Calculation

of

Goodwill

Cost of

Investment

500

Pre

acquisition owners' equity of the

subsidiary company

(400)

100

(20)

80

Goodwill

Calculation

of

Group

Reserves

All

reserves of parent

company

550

Post

acquisition of the subsidiary

company

50

(20)

Impairment

loss of good

580

Consolidated

Balance Sheet

As at 31

December 2008

Rs

Fixed

Assets

1,400

Goodwill

80

Current

Assets

600

2,080

Share

Capital

1,200

Reserves

580

Current

Liabilities

300

2,080

Example

- [ Case v ] Impairment of Goodwill,

Inter Co. Dividends &

Loans

Balance

Sheet as on 31st December

2008

P

S

Rs

Rs

Fixed

Assets

1,000

600

Investment

in S

500

Dividend

Receivable

100

Other

Current Assets

300

Current

Assets

400

200

Loan

to S

200

800

2,100

Share

Capital

1,200

300

198

Advance

Financial Accounting

(FIN-611)

VU

Reserves

700

150

Loan

from P

200

Dividend

Payable

100

Other

Current Liabilities

50

Current

Liabilities

200

150

2,100

800

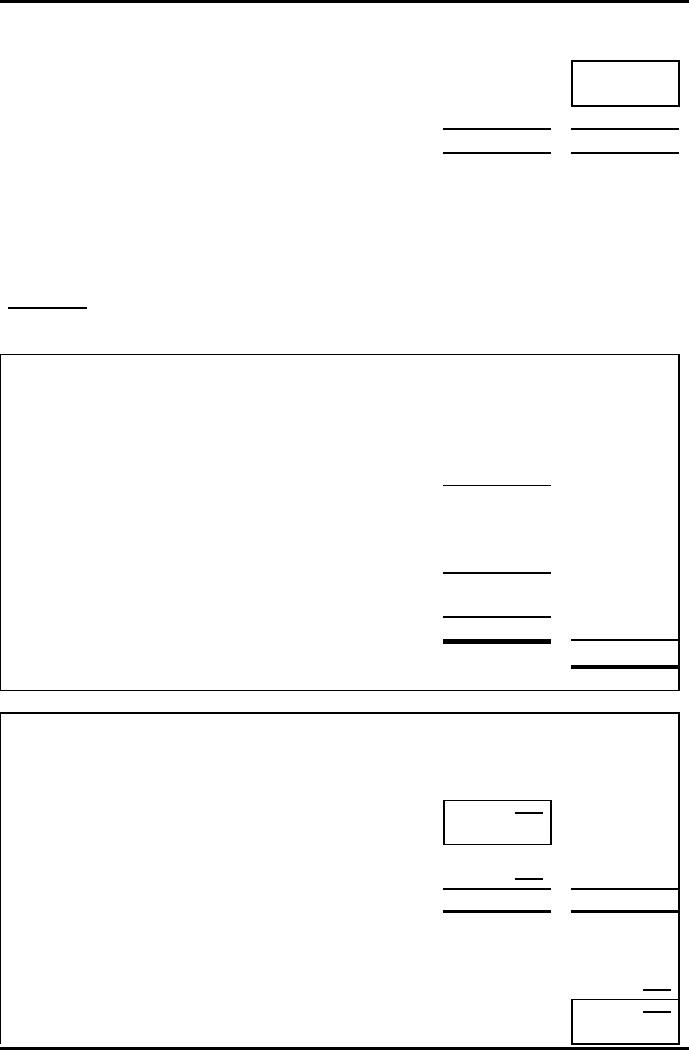

The

Parent Co. (P) acquired

100% shares of the

Subsidiary Co. (S) on 1st

January

2007 when

the reserves of the company

were worth Rs70. Goodwill has

been

impaired

by Rs. 52

Prepare

the Consolidated Balance

Sheet as at

31/12/2008.

Required:

Solution

- [ Case v ]

Analysis

of Equity

Pre

Post

Rs

Rs

S

Share

Capital

300

Reserves

70

80

370

P

Investment

500

Reserves

700

Goodwill

130

Impairment

of Goodwill

(52)

(52)

78

Group

Goodwill

Group

Reserves

728

P

S

Rs

Rs

Fixed

Assets

1,000

600

Investment

in S

500

Dividend

Receivable

100

Other

Current Assets

300

Current

Assets

400

200

Loan to

S

200

2,100

800

Share

Capital

1,200

300

Reserves

700

150

Loan

from P

200

Dividend

Payable

100

Other

Current Liabilities

50

199

Advance

Financial Accounting

(FIN-611)

VU

Current

Liabilities

200

150

2,100

800

Consolidated

Balance Sheet

As at 31

December 2008

Rs

Fixed

Assets

1,600

Goodwill

78

Current

Assets

500

2,178

Share

Capital

1,200

Reserves

728

Current

Liabilities

250

2,178

200

Table of Contents:

- ACCOUNTING FOR INCOMPLETE RECORDS

- PRACTICING ACCOUNTING FOR INCOMPLETE RECORDS

- CONVERSION OF SINGLE ENTRY IN DOUBLE ENTRY ACCOUNTING SYSTEM

- SINGLE ENTRY CALCULATION OF MISSING INFORMATION

- SINGLE ENTRY CALCULATION OF MARKUP AND MARGIN

- ACCOUNTING SYSTEM IN NON-PROFIT ORGANIZATIONS

- NON-PROFIT ORGANIZATIONS

- PREPARATION OF FINANCIAL STATEMENTS OF NON-PROFIT ORGANIZATIONS FROM INCOMPLETE RECORDS

- DEPARTMENTAL ACCOUNTS 1

- DEPARTMENTAL ACCOUNTS 2

- BRANCH ACCOUNTING SYSTEMS

- BRANCH ACCOUNTING

- BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM

- STOCK AND DEBTORS SYSTEM

- INDEPENDENT BRANCH

- BRANCH ACCOUNTING 1

- BRANCH ACCOUNTING 2

- ESSENTIALS OF PARTNERSHIP

- Partnership Accounts Changes in partnership firm

- COMPANY ACCOUNTS 1

- COMPANY ACCOUNTS 2

- Problems Solving

- COMPANY ACCOUNTS

- RETURNS ON FINANCIAL SOURCES

- IASBS FRAMEWORK

- ELEMENTS OF FINANCIAL STATEMENTS

- EVENTS AFTER THE BALANCE SHEET DATE

- PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 1

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 2

- BORROWING COST

- EXCESS OF THE CARRYING AMOUNT OF THE QUALIFYING ASSET OVER RECOVERABLE AMOUNT

- EARNINGS PER SHARE

- Earnings per Share

- DILUTED EARNINGS PER SHARE

- GROUP ACCOUNTS

- Pre-acquisition Reserves

- GROUP ACCOUNTS: Minority Interest

- GROUP ACCOUNTS: Inter Company Trading (P to S)

- GROUP ACCOUNTS: Fair Value Adjustments

- GROUP ACCOUNTS: Pre-acquistion Profits, Dividends

- GROUP ACCOUNTS: Profit & Loss

- GROUP ACCOUNTS: Minority Interest, Inter Co.

- GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit)

- Comprehensive Workings in Group Accounts Consolidated Balance Sheet