|

Perfect Competition:Effect of Excise Tax on Monopolist |

| << Perfect Competition:Total, Marginal, and Average Revenue |

| Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power >> |

Microeconomics

ECO402

VU

Lesson

31

A

Rule of Thumb for

Pricing

We want to

translate the condition that

marginal revenue should

equal marginal cost

into

a

rule of thumb that can be

more easily applied in

practice.

This can be

demonstrated using the

following steps:

ΔR

Δ

(

PQ

)

1

. MR

=

=

ΔQ

ΔQ

⎛

Q

⎞⎛ Δ

P

⎞

ΔP

=

P

+

P

⎜

⎟⎜

⎟

2

. MR

=

P

+

Q

P

⎠⎜ Δ

Q

⎟

ΔQ

⎝

⎝

⎠

=

⎛ P

⎞⎛ Δ

Q

⎞

⎜

Q

⎟⎜

ΔP

⎟

3.

E

d

⎝

⎠⎝

⎠

)(

)

(

1

Q

Δ P

=

4.

Δ Q

P

E

d

⎛

⎞

1

=

P

+P

⎜

5.

M

R

⎟

⎝ E

⎠

d

6

.

is

maximized

@

MR =

MC

⎡ 1 ⎤

1

P

+

P⎢

=-

⎥

⎣ED ⎦

ED

MC

P =

1

+

(1

E D )

1

7.

-

=

the markup over MC as a

percentage of price

(P-MC)/P

E d

8.

The

markup should equal the

inverse of the elasticity of

demand.

MC

9.

P

=

()

1

1+

Ed

Assume

Ed = -4

MC

= 9

9

9

P=

=

=

$12

(

)

.75

1+ 1

-4

Monopoly

pricing compared to perfect

competition pricing:

Monopoly

P

> MC

Perfect

Competition

P

= MC

Monopoly

pricing compared to perfect

competition pricing:

146

Microeconomics

ECO402

VU

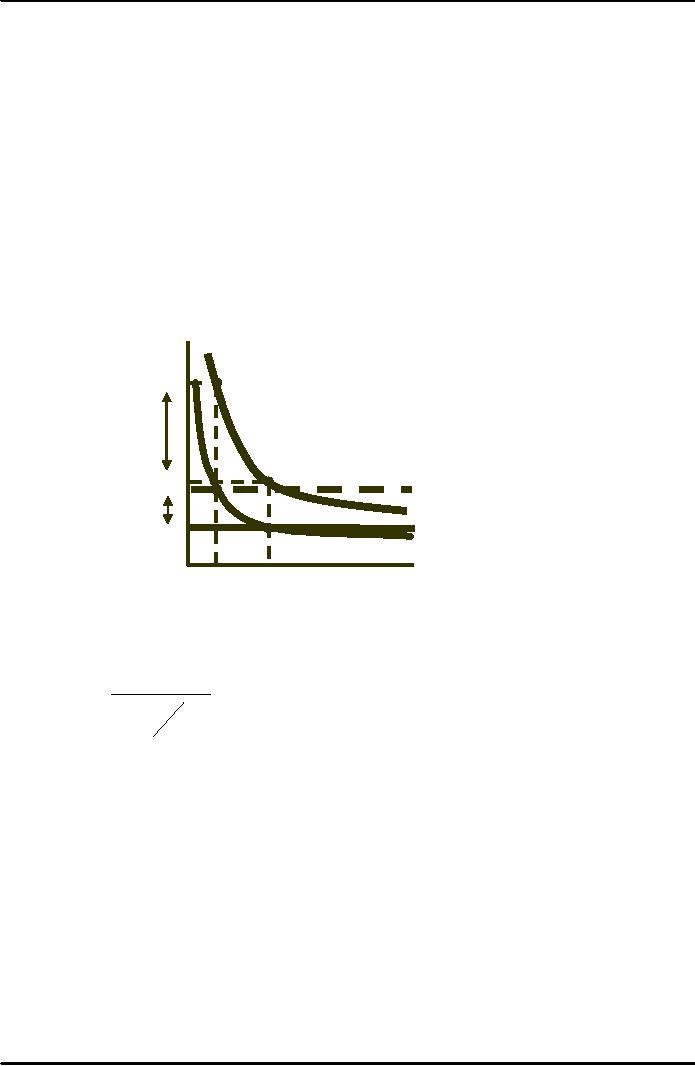

The more

elastic the demand the

closer price is to marginal

cost.

If Ed is a

large negative number, price

is close to marginal cost

and vice versa.

A

Monopolist's Pricing

The

Monopolist's Output

Decision

Price of

Medicine A = $3.50/daily

dose

Price of

Medicine B and Medicine C =

$1.50 - $2.25/daily

dose

MC of Medicine A = 30 - 40

cents/daily dose

♦The

Monopolist's Output Decision

MC

.

35

P =

=

=

1+

[ E

]

1

+

[ -

1

.1]

1

1

D

MC

.

35

=

=

$ 3 .

89

1

+

(-

.

91

)

.

09

♦Price

of $3.50 is consistent with

"the rule of thumb

pricing"

Shifts

in Demand

In perfect

competition, the market

supply curve is determined by

marginal cost.

For a monopoly,

output is determined by marginal

cost and the shape of

the demand

curve.

Shift

in Demand Leads to Change in

Price but Same

Output

MC

$/Q

P1

P2

D2

D1

MR2

MR1

Quantity

Q1=

Q2

MC

$/Q

P1 =

P2

D2

MR2

D

MR1

Q1

Q

Quantity

147

Microeconomics

ECO402

VU

Monopoly

Observations

Shifts in

demand usually cause a

change in both price and

quantity.

A monopolistic

market has no supply

curve.

Monopolist may

supply many different

quantities at the same

price.

Monopolist may

supply the same quantity at

different prices.

The

Effect of a Tax

Under monopoly

price can sometimes rise by

more

than

the amount of the

tax.

To

determine the impact of a

tax:

t = specific

tax

MC = MC + t

MR = MC + t : optimal

production decision

Effect

of Excise Tax on

Monopolist

$/Q

Increase

in P:

P0 to

P1 >

increase in

tax

P1

ΔP

P0

MC

+ tax

D

= AR

t

MC

MR

Q0

Q1

Quantity

Question

Suppose: Ed =

-2

How much

would the price

change?

Answer

MC

P=

1+ ⎛ 1

⎞

⎜ E

⎟

⎝

⎠

d

If

E

d = - 2 →

P

= 2

MC

If

MC

increases

to MC

+

t

Δ

P

= 2 (

MC

+

t

) = 2

MC

+ 2

t

Price

increases

by

twice

the

tax.

What

would happen to

profits?

148

Table of Contents:

- ECONOMICS:Themes of Microeconomics, Theories and Models

- Economics: Another Perspective, Factors of Production

- REAL VERSUS NOMINAL PRICES:SUPPLY AND DEMAND, The Demand Curve

- Changes in Market Equilibrium:Market for College Education

- Elasticities of supply and demand:The Demand for Gasoline

- Consumer Behavior:Consumer Preferences, Indifference curves

- CONSUMER PREFERENCES:Budget Constraints, Consumer Choice

- Note it is repeated:Consumer Preferences, Revealed Preferences

- MARGINAL UTILITY AND CONSUMER CHOICE:COST-OF-LIVING INDEXES

- Review of Consumer Equilibrium:INDIVIDUAL DEMAND, An Inferior Good

- Income & Substitution Effects:Determining the Market Demand Curve

- The Aggregate Demand For Wheat:NETWORK EXTERNALITIES

- Describing Risk:Unequal Probability Outcomes

- PREFERENCES TOWARD RISK:Risk Premium, Indifference Curve

- PREFERENCES TOWARD RISK:Reducing Risk, The Demand for Risky Assets

- The Technology of Production:Production Function for Food

- Production with Two Variable Inputs:Returns to Scale

- Measuring Cost: Which Costs Matter?:Cost in the Short Run

- A Firms Short-Run Costs ($):The Effect of Effluent Fees on Firms Input Choices

- Cost in the Long Run:Long-Run Cost with Economies & Diseconomies of Scale

- Production with Two Outputs--Economies of Scope:Cubic Cost Function

- Perfectly Competitive Markets:Choosing Output in Short Run

- A Competitive Firm Incurring Losses:Industry Supply in Short Run

- Elasticity of Market Supply:Producer Surplus for a Market

- Elasticity of Market Supply:Long-Run Competitive Equilibrium

- Elasticity of Market Supply:The Industrys Long-Run Supply Curve

- Elasticity of Market Supply:Welfare loss if price is held below market-clearing level

- Price Supports:Supply Restrictions, Import Quotas and Tariffs

- The Sugar Quota:The Impact of a Tax or Subsidy, Subsidy

- Perfect Competition:Total, Marginal, and Average Revenue

- Perfect Competition:Effect of Excise Tax on Monopolist

- Monopoly:Elasticity of Demand and Price Markup, Sources of Monopoly Power

- The Social Costs of Monopoly Power:Price Regulation, Monopsony

- Monopsony Power:Pricing With Market Power, Capturing Consumer Surplus

- Monopsony Power:THE ECONOMICS OF COUPONS AND REBATES

- Airline Fares:Elasticities of Demand for Air Travel, The Two-Part Tariff

- Bundling:Consumption Decisions When Products are Bundled

- Bundling:Mixed Versus Pure Bundling, Effects of Advertising

- MONOPOLISTIC COMPETITION:Monopolistic Competition in the Market for Colas and Coffee

- OLIGOPOLY:Duopoly Example, Price Competition

- Competition Versus Collusion:The Prisoners Dilemma, Implications of the Prisoners

- COMPETITIVE FACTOR MARKETS:Marginal Revenue Product

- Competitive Factor Markets:The Demand for Jet Fuel

- Equilibrium in a Competitive Factor Market:Labor Market Equilibrium

- Factor Markets with Monopoly Power:Monopoly Power of Sellers of Labor