|

GROUP ACCOUNTS: Profit & Loss |

| << GROUP ACCOUNTS: Pre-acquistion Profits, Dividends |

| GROUP ACCOUNTS: Minority Interest, Inter Co. >> |

Advance

Financial Accounting

(FIN-611)

VU

LESSON

# 42

GROUP

ACCOUNTS

Profit

& Loss

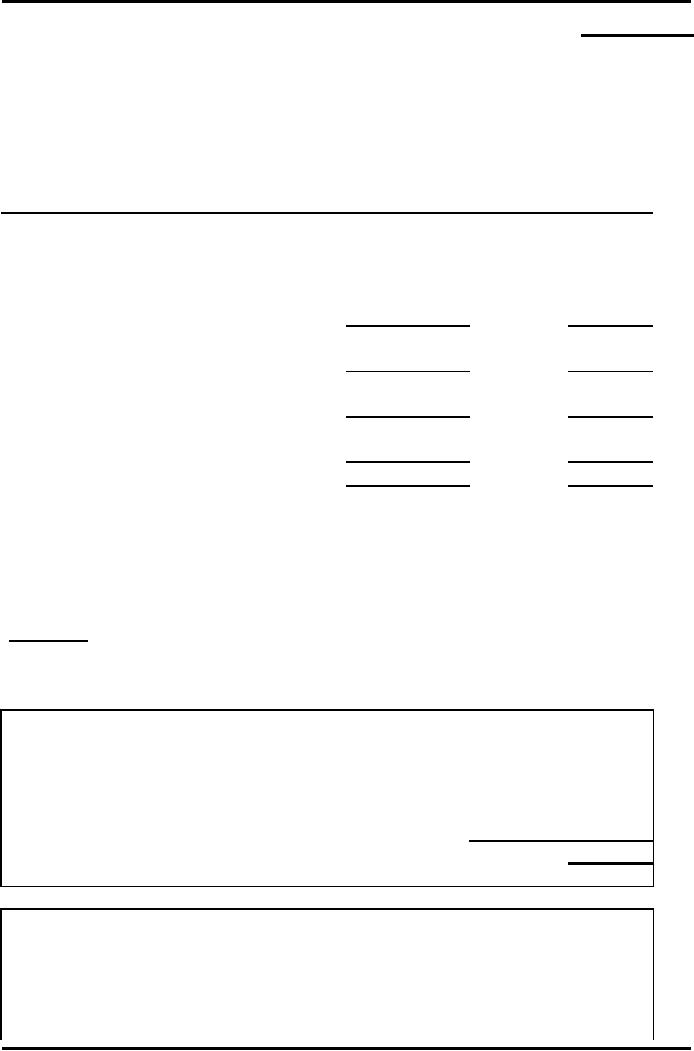

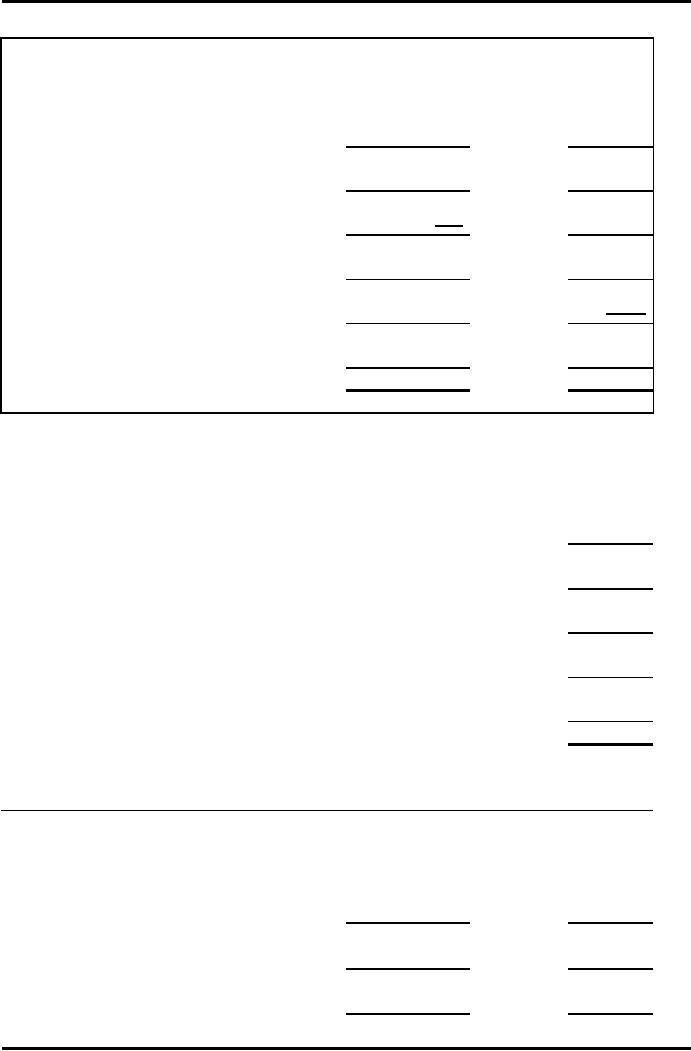

Example

- [ Case i ] Simple

Consolidation

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

7,500

4,000

(2,900)

Cost

of Goods Sold

(4,500)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Income

Tax

(480)

(200)

Net

Profit after Tax

720

300

Retained

Profits b/f

1,000

450

750

Retained

Profits c/f

1,720

The

Parent Co. (P) acquired

100% equity of the Subsidary

Co. (S) on 1st

January

2008 for

Rs.1,700 when S's paid up

share capital was Rs.1,250

& it's reserves

were

worth Rs.450. (Assume all reserves

comprise only of Retained

Profits).

Prepare

the Consolidated Income

Statement for the

year

ended 31/12/2008.

Required:

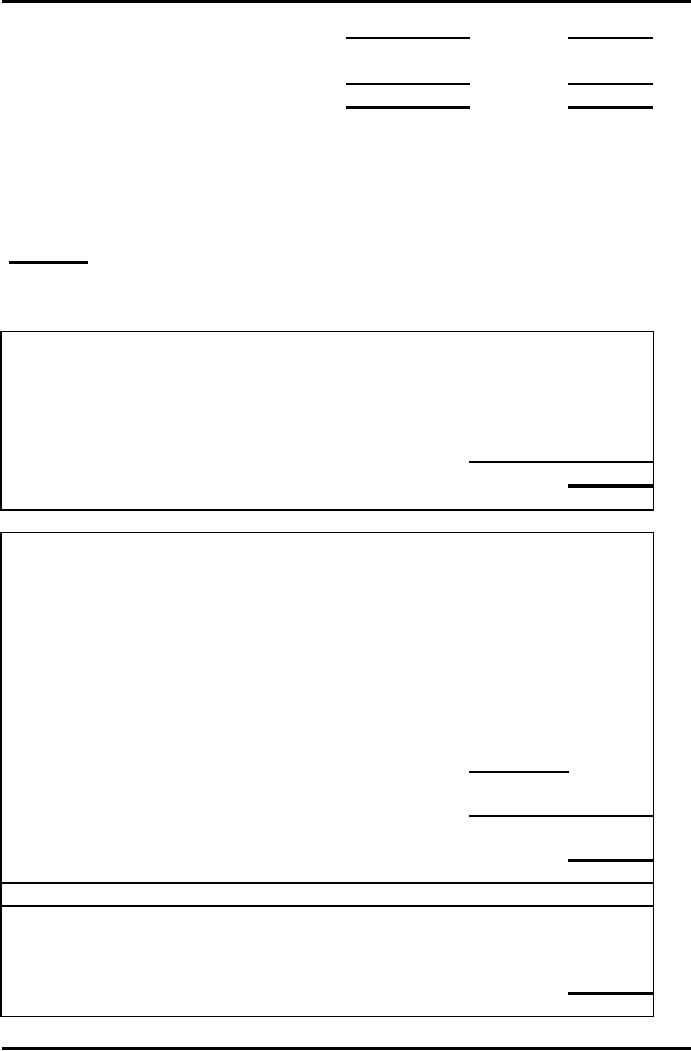

Solution

- [ Case i ]

Computation

of Goodwill

Rs.

Rs.

Cost of

Acquisition

1,700

Ordinary

Share Capital of S

1,250

Pre-acquisition

Retained Profits of

S

450

0

Goodwill

1,700

Computation

of opening balance of Group's Retained

Profits

Rs.

Rs.

Total

amount of opening balance of

retained

profits

of P Co

1,000

Post

acquisition part in opening balance of

retained profits of

S

Co

220

Advance

Financial Accounting

(FIN-611)

VU

opening

balance of

retained

profits of S

Co

450

pre-acquisition

retained

profits

-450

0

Opening

balance of Group's

Retained

Profits

b/f

1,000

Consolidated

Income Statement

For

the year ended 31st December

2008

Rs.

Sales

11,500

Cost of

Goods Sold

(7,400)

Gross

Profit

4,100

Operating

Expenses

(2,400)

Operating

Profit

1,700

Income

Tax

(680)

Net

Profit after Tax

1,020

Retained

Profits b/f

1,000

Retained

Profits c/f

2,020

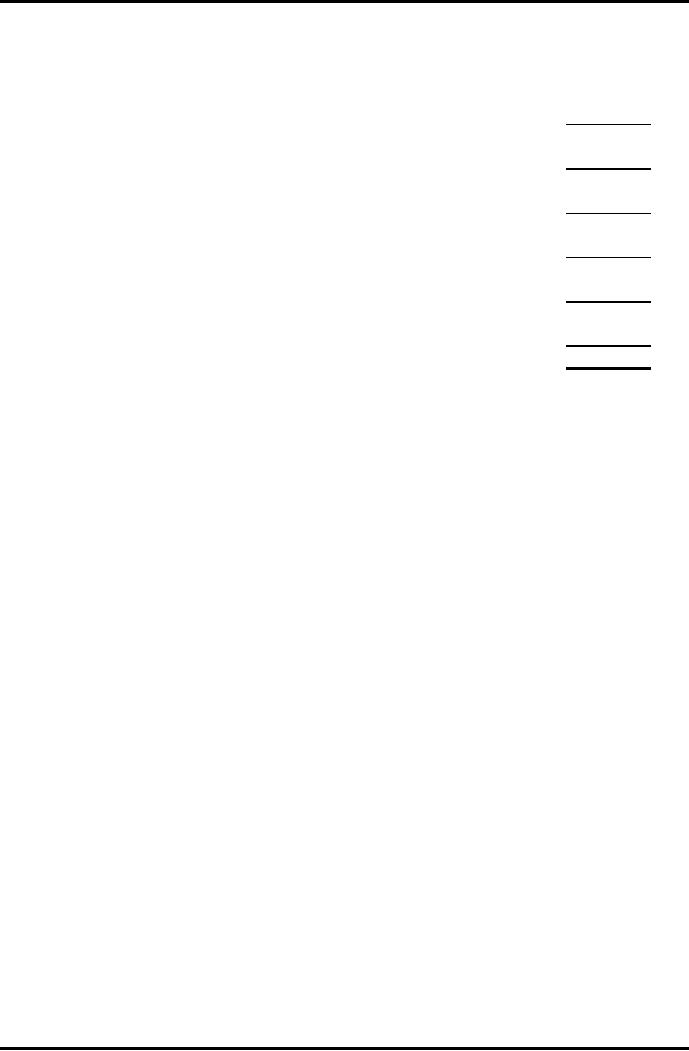

Example

- [ Case ii ] Post acquisition opening

balance of retained

profits

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

7,500

4,000

Cost

of Goods Sold

(4,500)

(2,900)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Income

Tax

(480)

(200)

Net

Profit after Tax

720

300

Retained

Profits b/f

1,000

450

Retained

Profits c/f

1,720

750

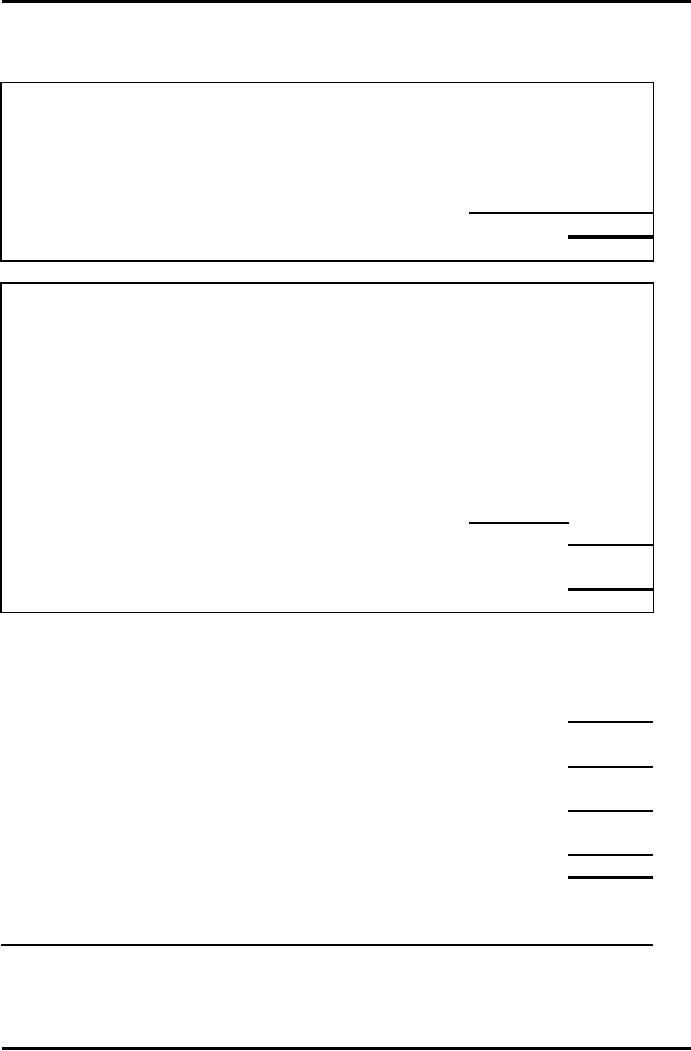

The

Parent Co. (P) acquired

100% equity of the Subsidary

Co. (S) on 1st

January

2007 for

Rs.1,700 when S's paid up

share capital was Rs.1,250

& it's reserves

were

worth Rs.150. (Assume all reserves

comprise only of Retained

Profits).

Prepare

the Consolidated Income

Statement for the

Required:

year

ended 31/12/2008.

221

Advance

Financial Accounting

(FIN-611)

VU

Solution

- [ Case ii ]

Computation

of Goodwill

Rs.

Rs.

Cost of

Acquisition

1,700

Ordinary

Share Capital of S

1,250

Pre-acquisition

Retained Profits of

(1,400)

S

150

300

Computation

of opening balance of Group's Retained

Profits

Rs.

Rs.

Total

amount of opening balance of

retained

profits

of P Co

1,000

Post

acquisition part in opening balance of

retained profits of

S

Co

opening

balance of

retained

profits of S

Co

450

pre-acquisition

retained

profits

-150

300

Opening

balance of Group's

Retained

Profits

b/f

1,300

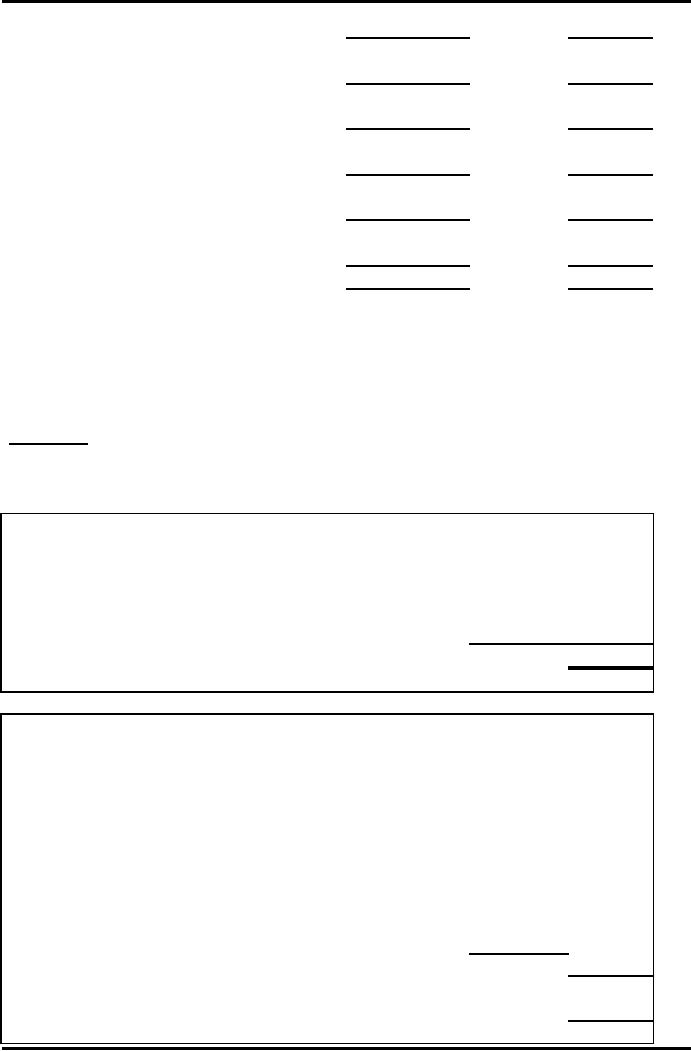

Consolidated

Income Statement

For

the year ended 31st December

2008

Rs.

Sales

11,500

Cost of

Goods Sold

(7,400)

Gross

Profit

4,100

Operating

Expenses

(2,400)

Operating

Profit

1,700

Income

Tax

(680)

Net

Profit after Tax

1,020

Retained

Profits b/f

1,300

Retained

Profits c/f

2,320

Example

- [ Case iii ] Inter Co.

Dvidends

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

7,500

4,000

222

Advance

Financial Accounting

(FIN-611)

VU

Cost

of Goods Sold

(4,500)

(2,900)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Dividend

Income

125

500

Net

Profit before Tax

1,325

Income

Tax

(530)

(200)

Net

Profit after Tax

795

300

Dividend

Paid

(250)

(125)

545

175

Retained

Profits b/f

1,000

450

Retained

Profits c/f

1,545

625

The

Parent Co. (P) acquired

100% equity of the Subsidary

Co. (S) on 1st

January

2006 for

Rs.1,700 when S's paid up

share capital was Rs.1,250

& it's reserves

were

worth Rs.50. (Assume all reserves

comprise only of Retained

Profits).

Prepare

the Consolidated Income

Statement for the

year

ended 31/12/2008.

Required:

Solution

- [ Case iii ]

Computation

of Goodwill

Rs.

Rs.

Cost of

Acquisition

1,700

Ordinary

Share Capital of S

1,250

Pre-acquisition

Retained Profits of

S

50

(1,300)

400

Computation

of opening balance of Group's Retained

Profits

Rs.

Rs.

Total

amount of opening balance of

retained

profits

of P Co

1,000

Post

acquisition part in opening balance of

retained profits of

S

Co

opening

balance of

retained

profits of S

Co

450

pre-acquisition

retained

profits

-50

400

Opening

balance of Group's

Retained

Profits

b/f

1,400

223

Advance

Financial Accounting

(FIN-611)

VU

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

Sales

7,500

4,000

Cost of

Goods Sold

(4,500)

(2,900)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Dividend

Income

125

Net

Profit before Tax

1,325

500

Income

Tax

(530)

(200)

Net

Profit after Tax

795

300

Dividend

Paid

(250)

(125)

545

175

Retained

Profits b/f

1,000

450

Retained

Profits c/f

1,545

625

Consolidated

Income Statement

For

the year ended 31st December

2008

Rs.

Sales

11,500

Cost of

Goods Sold

(7,400)

Gross

Profit

4,100

Operating

Expenses

(2,400)

Operating

Profit

1,700

Income

Tax

(730)

Net

Profit after Tax

970

Dividend

Paid

(250)

720

Retained

Profits b/f

1,400

Retained

Profits c/f

2,120

Example

- [ Case iv ] Minority

Interest

Income

Statement for the year ended

31st December 2008

P

S

Rs.

Rs.

4,000

Sales

7,500

Cost

of Goods Sold

(4,500)

(2,900)

Gross

Profit

3,000

1,100

Operating

Expenses

(1,800)

(600)

Operating

Profit

1,200

500

Income

Tax

(480)

(200)

Net

Profit after Tax

720

300

224

Advance

Financial Accounting

(FIN-611)

VU

Dividend

Paid

(200)

520

300

Retained

Profits b/f

1,000

450

Retained

Profits c/f

1,520

750

The

Parent Co. (P) acquired

80% equity of the Subsidary

Co. (S) on 1st

January

2006 for

Rs.1,700 when S's paid up

share capital was Rs.1,250

& it's reserves

were

worth Rs.50. (Assume all reserves

comprise only of Retained

Profits).

Prepare

the Consolidated Income

Statement for the

Required:

year

ended 31/12/2008.

Solution

- [ Case iv ]

Computation

of Goodwill

Rs.

Rs.

Cost of

Acquisition

1,700

Ordinary

Share Capital of S

80%

of Rs.1,250

1,000

Pre-acquisition

Retained Profits of

S

80%

of Rs.50

40

(1,040)

80%

of Rs. 1300

660

Computation

of opening balance of Group's Retained

Profits

Rs.

Rs.

Total

amount of opening balance of

retained

1,000

profits

of P Co

Post

acquisition part in opening balance of

retained profits of

S

Co

opening

balance of

retained

profits of S

Co

450

pre-acquisition

retained

profits

-50

to the

extent of

400

320

H%

i.e.80%

Opening

balance of Group's

Retained

Profits

b/f

1,320

Computation

of Minority Interest

Rs.

Profits

after tax of S Co. to the

extent of

MI%

20%

of Rs.300

60

225

Advance

Financial Accounting

(FIN-611)

VU

Consolidated

Income Statement

For

the year ended 31st December

2008

Rs.

Rs.

Sales

11,500

Cost of

Goods Sold

(7,400)

Gross

Profit

4,100

Operating

Expenses

-2,400

Operating

Profit

1,700

Income

Tax

(680)

Net

Profit after Tax

1,020

Minority

Interest

(60)

960

Dividend

Paid

(200)

760

Retained

Profits b/f

1,320

Retained

Profits c/f

2,080

226

Table of Contents:

- ACCOUNTING FOR INCOMPLETE RECORDS

- PRACTICING ACCOUNTING FOR INCOMPLETE RECORDS

- CONVERSION OF SINGLE ENTRY IN DOUBLE ENTRY ACCOUNTING SYSTEM

- SINGLE ENTRY CALCULATION OF MISSING INFORMATION

- SINGLE ENTRY CALCULATION OF MARKUP AND MARGIN

- ACCOUNTING SYSTEM IN NON-PROFIT ORGANIZATIONS

- NON-PROFIT ORGANIZATIONS

- PREPARATION OF FINANCIAL STATEMENTS OF NON-PROFIT ORGANIZATIONS FROM INCOMPLETE RECORDS

- DEPARTMENTAL ACCOUNTS 1

- DEPARTMENTAL ACCOUNTS 2

- BRANCH ACCOUNTING SYSTEMS

- BRANCH ACCOUNTING

- BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM

- STOCK AND DEBTORS SYSTEM

- INDEPENDENT BRANCH

- BRANCH ACCOUNTING 1

- BRANCH ACCOUNTING 2

- ESSENTIALS OF PARTNERSHIP

- Partnership Accounts Changes in partnership firm

- COMPANY ACCOUNTS 1

- COMPANY ACCOUNTS 2

- Problems Solving

- COMPANY ACCOUNTS

- RETURNS ON FINANCIAL SOURCES

- IASBS FRAMEWORK

- ELEMENTS OF FINANCIAL STATEMENTS

- EVENTS AFTER THE BALANCE SHEET DATE

- PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 1

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 2

- BORROWING COST

- EXCESS OF THE CARRYING AMOUNT OF THE QUALIFYING ASSET OVER RECOVERABLE AMOUNT

- EARNINGS PER SHARE

- Earnings per Share

- DILUTED EARNINGS PER SHARE

- GROUP ACCOUNTS

- Pre-acquisition Reserves

- GROUP ACCOUNTS: Minority Interest

- GROUP ACCOUNTS: Inter Company Trading (P to S)

- GROUP ACCOUNTS: Fair Value Adjustments

- GROUP ACCOUNTS: Pre-acquistion Profits, Dividends

- GROUP ACCOUNTS: Profit & Loss

- GROUP ACCOUNTS: Minority Interest, Inter Co.

- GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit)

- Comprehensive Workings in Group Accounts Consolidated Balance Sheet