|

Cost

& Management Accounting

(MGT-402)

VU

LESSON#

9

ECONOMIC

ORDERING QUANTITY

Economic

order quantity refers to

that number (quantity)

ordered in a single purchase so

that the

accumulated

costs of ordering and carrying

costs are at the minimum

level.

In

other words, the quantity

that is ordered at one time

should be so, which will

minimize the total

of

(i) Cost of placing orders

and receiving the goods, and

(ii) cost of storing the

goods as well as

interest

on the capital invested.

The

economic order quantity can be determined

by the following simple

formula:

EOQ

=

2xRUxOC

UC

x CC%

Where;

EOQ

=

Economic

Order Quantity.

RU

=

Annually

Required Units.

OC

=

Ordering

Costs for one order.

UC

=

Inventory

Unit Cost.

CC

=

Carrying

Cost as %age of Unit

Cost.

This

formula is based on three

assumptions:

1.

Price will remain constant

throughout the year and

quantity discount is not

involved.

2.

Pattern of consumption, variable

ordering costs per order

and variable inventory

carrying

charge

per unit per annum

will remain the same

throughout, and

3.

EOQ will be delivered each time

the stock balance is just

reduced to nil.

The

Economic Order Quantity can

be determined by applying the formula as

under:

Suppose;

the

Annual

consumption is

80,000

units,

Cost

to place one order is

Rs.

1,200

Cost

per unit is

Rs.

50

Carrying

cost is

6%

of Unit cost

EOQ

=

2xRUxOC

UC

x CC%

EOQ

=

2

x 80,000 x 1,200

50x6%

EOQ

=

8,000

As

stated above this formula

holds good if changes in

price are not likely in

the near future

and

consumption

is regular. Otherwise, placing orders

according to this formula

may become

expensive.

Carrying

cost of inventory consists of

(i) the costs of physical

storage such as cost of

space,

handling

and upkeep expenses, insurance,

cost of obsolescence, etc.,

and (ii) interest on

capital

invested

(the opportunity cost of the

capital blocked up). All

these costs are expressed in

%age of

the

cost per unit.

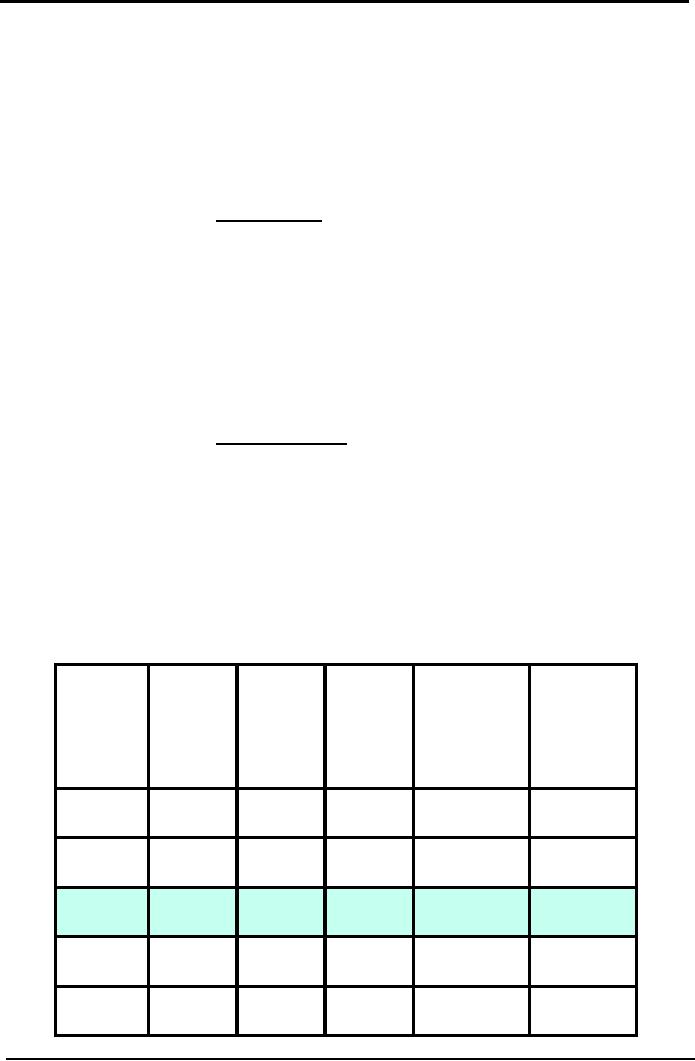

Table

of EOQ

Economic

order quantity can also be

proved through a table, by calculating

total cost at

different

order

quantities.

56

Cost

& Management Accounting

(MGT-402)

VU

Following

is a table that is showing

total cost at five different

order quantities, assuming that

the

annual

requirement of the units to be consumed

remains the same. Here

the total cost

comprises

of

ordering cost and carrying

cost.

Total

Ordering cost

Ordering

cost is arrived by multiplying the

number of orders in a year

with the cost

per

order. Number of order is

calculated by dividing annually required

units by the

order

quantity.

Step

I:

Required

Units = Number of

orders

Order

Quantity

Step

II: Number of orders x Cost

per order

Total

Carrying Cost

Carrying

cost is arrived by multiplying the

average ordering quantity

with the

carrying

cost per unit. Average

ordering quantity is calculated by

dividing the

ordering

quantity by 2. (It

is assumed that half of the ordering

quantity is always kept into

the

store,

this is the reason the ordering quantity

is divided by 2)

Step

I:

Ordering

Quantity = Average ordering

quantity

2

Step

II: Carrying cost per unit =

Unit Cost x CC %age

Step

III:

Average

ordering quantity x Carrying cost

per unit

Applying

these steps at different presumed

order quantities (inclusive of

the

Economic

Order Quantity) we can

develop a table.

Required

Number of Total Total

Carrying

Total

cost

Order

Cost

Quantity

Units

orders

Ordering

Avg

Order qty x

Cost

Number

of

Rs.3

orders

x

Rs.

1,200

20,000

80,000

4

4,800

30,000

34,800

10,000

80,000

8

9,600

15,000

24,600

8,000

80,000

10

12,000

12,000

24,000

5,000

80,000

16

19,200

7,500

26,700

4,000

80,000

20

24,000

6,000

30,000

57

Cost

& Management Accounting

(MGT-402)

VU

The

above table shows that

8,000 is the economic order

quantity because at this

point total

cost

is the minimum. At this

point total ordering cost is

equal to the total carrying

cost.

If

the order quantity is

increased it will although

result in reducing the total

ordering cost but

at

the same time more

carrying cost will be

incurred to store the

inventory.

Whereas

if the order quantity is

decreased it will although

result in reducing the total

carrying

cost

but at the same time

more ordering cost will be

incurred as the number of

orders will

increase.

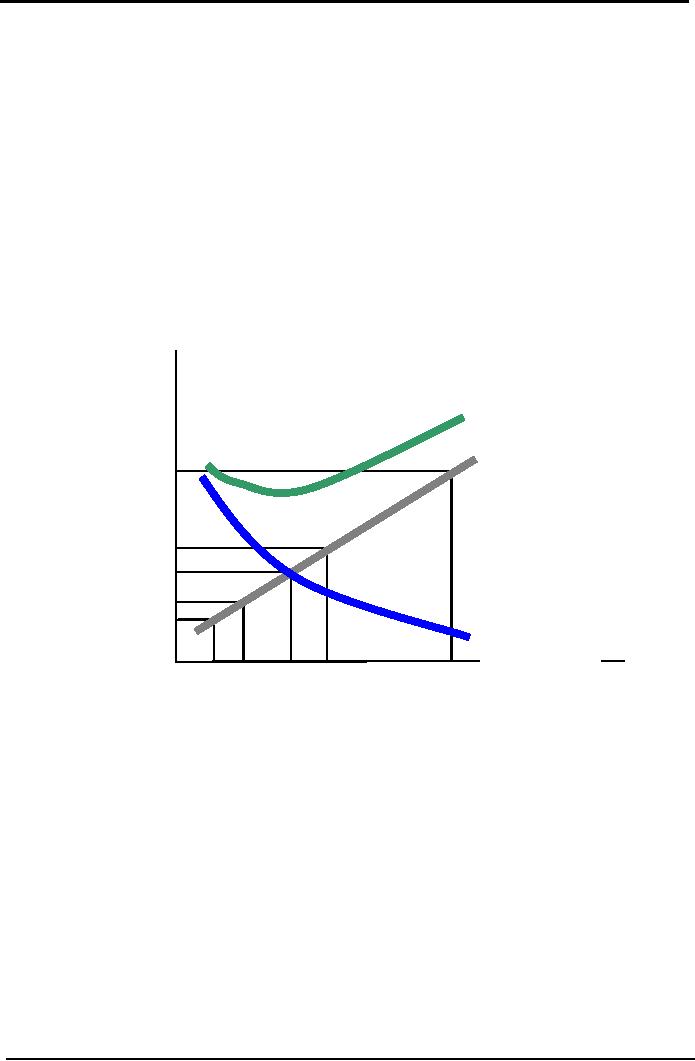

EOQ

Graph

Economic

order quantity can also be

determined through a graph. Here the

above

information

is plotted in a graph for total

ordering cost, total carrying

cost and total cost

at

different

ordering quantities.

The

point at which the line of

total ordering cost

intersects with the total

carrying cost is the

EOQ.

At this point the line of

total cost will give a bend

that shows the minimum

cost.

COSTS

(000)

Total

Cost

36

30

Total

Carrying

Cost

24

18

12

6

Total

Ordering

Cost

4

8

10

20

5

ORDER

SIZE (Q) (000)

In

the above graph line of

total carrying cost intersects

line of total ordering cost

at 8,000 order

quantities,

where both of the costs are

Rs. 12,000. At this order

quantity the total cost is

Rs. 24,000

which

is the minimum most.

If

the order quantity is

increased or decreased the

total cost will be more

than the cost at

EOQ.

This

is also evident from the

above graph.

PROBLEMS

Q.

1

From

the following data, you

are required to determine the Economic

Order Quantity.

Annual

usage

8,000

units

Cost

per unit

Rs.

30

Ordering

cost

Rs.

7 per order

Storage

and carrying cost as percentage of

average inventory holding

15%

58

Cost

& Management Accounting

(MGT-402)

VU

Q.

2

What

is Economic Order Quantity

(EOQ)? Should the quantity

ordered be always equal to

EOQ?

Calculate

EOQ from the

following:

(a)

RU

600

units

{b)

Ordering

cost

Rs,

12 per order

(c)

Carrying cost

20%

(d)

Price

per unit

Rs.

20.

Q.

3

Annual

requirement of Glass Limited is

100,000 units of product

10mm glass. Per unit

cost of the

product

is Rs. 10 and cost for

each new order is Rs.

100. Carrying cost is

50%.

Required:

Calculate

EOQ by table and by graph.

MULTIPLE

CHOICE QUESTIONS

Q.

1

The

demand for a product is

12,500 units for a three

month period. Each unit of product

has a

purchase

price of Rs.15 and ordering

costs are Rs.20 per

order placed.

The

annual holding cost of one

unit of product is 10% of its

purchase price.

What

is the Economic Order

Quantity (to the nearest

unit)?

A

1,577

B

1,816

C

1,866

D

1,155

Q.

2

A

company determines its order

quantity for a raw material by using

the Economic Order

Quantity

(EOQ)

model.

What

would be the effects of a decrease in

the cost of ordering a batch

of raw material on the

ordering

quantity and

the total

carrying cost?

Ordering

quantity

Total

carrying cost

A

Higher

Lower

B

Higher

Higher

C

Lower

Higher

D

Lower

Lower

Q.

3

A

company uses the Economic

Order Quantity (EOQ) model

to establish reorder quantities.

The

following information relates to

the forthcoming period:

Order

costs

Rs.25

per order

Carrying

costs

10%

of purchase price

Annual

demand

20,000

units

Purchase

price

Rs.40

per unit

EOQ

500

units

What

are the total annual

costs of stock (i.e. the

total purchase cost plus

total order cost

plus

total

holding cost)?

A

Rs.

22,000

B

Rs.

33,500

C

Rs.

802,000

D

Rs.

803,000

59

Table of Contents:

- COST CLASSIFICATION AND COST BEHAVIOR INTRODUCTION:COST CLASSIFICATION,

- IMPORTANT TERMINOLOGIES:Cost Center, Profit Centre, Differential Cost or Incremental cost

- FINANCIAL STATEMENTS:Inventory, Direct Material Consumed, Total Factory Cost

- FINANCIAL STATEMENTS:Adjustment in the Entire Production, Adjustment in the Income Statement

- PROBLEMS IN PREPARATION OF FINANCIAL STATEMENTS:Gross Profit Margin Rate, Net Profit Ratio

- MORE ABOUT PREPARATION OF FINANCIAL STATEMENTS:Conversion Cost

- MATERIAL:Inventory, Perpetual Inventory System, Weighted Average Method (W.Avg)

- CONTROL OVER MATERIAL:Order Level, Maximum Stock Level, Danger Level

- ECONOMIC ORDERING QUANTITY:EOQ Graph, PROBLEMS

- ACCOUNTING FOR LOSSES:Spoiled output, Accounting treatment, Inventory Turnover Ratio

- LABOR:Direct Labor Cost, Mechanical Methods, MAKING PAYMENTS TO EMPLOYEES

- PAYROLL AND INCENTIVES:Systems of Wages, Premium Plans

- PIECE RATE BASE PREMIUM PLANS:Suitability of Piece Rate System, GROUP BONUS SYSTEMS

- LABOR TURNOVER AND LABOR EFFICIENCY RATIOS & FACTORY OVERHEAD COST

- ALLOCATION AND APPORTIONMENT OF FOH COST

- FACTORY OVERHEAD COST:Marketing, Research and development

- FACTORY OVERHEAD COST:Spending Variance, Capacity/Volume Variance

- JOB ORDER COSTING SYSTEM:Direct Materials, Direct Labor, Factory Overhead

- PROCESS COSTING SYSTEM:Data Collection, Cost of Completed Output

- PROCESS COSTING SYSTEM:Cost of Production Report, Quantity Schedule

- PROCESS COSTING SYSTEM:Normal Loss at the End of Process

- PROCESS COSTING SYSTEM:PRACTICE QUESTION

- PROCESS COSTING SYSTEM:Partially-processed units, Equivalent units

- PROCESS COSTING SYSTEM:Weighted average method, Cost of Production Report

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Accounting for joint products

- COSTING/VALUATION OF JOINT AND BY PRODUCTS:Problems of common costs

- MARGINAL AND ABSORPTION COSTING:Contribution Margin, Marginal cost per unit

- MARGINAL AND ABSORPTION COSTING:Contribution and profit

- COST VOLUME PROFIT ANALYSIS:Contribution Margin Approach & CVP Analysis

- COST VOLUME PROFIT ANALYSIS:Target Contribution Margin

- BREAK EVEN ANALYSIS MARGIN OF SAFETY:Margin of Safety (MOS), Using Budget profit

- BREAKEVEN ANALYSIS CHARTS AND GRAPHS:Usefulness of charts

- WHAT IS A BUDGET?:Budgetary control, Making a Forecast, Preparing budgets

- Production & Sales Budget:Rolling budget, Sales budget

- Production & Sales Budget:Illustration 1, Production budget

- FLEXIBLE BUDGET:Capacity and volume, Theoretical Capacity

- FLEXIBLE BUDGET:ANALYSIS OF COST BEHAVIOR, Fixed Expenses

- TYPES OF BUDGET:Format of Cash Budget,

- Complex Cash Budget & Flexible Budget:Comparing actual with original budget

- FLEXIBLE & ZERO BASE BUDGETING:Efficiency Ratio, Performance budgeting

- DECISION MAKING IN MANAGEMENT ACCOUNTING:Spare capacity costs, Sunk cost

- DECISION MAKING:Size of fund, Income statement

- DECISION MAKING:Avoidable Costs, Non-Relevant Variable Costs, Absorbed Overhead

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS

- DECISION MAKING CHOICE OF PRODUCT (PRODUCT MIX) DECISIONS:MAKE OR BUY DECISIONS