|

Project

Management MGMT627

VU

LESSON

40

COST

MANAGEMENT AND CONTROL IN

PROJECTS

BROAD

CONTENTS

Cost

Management

Cost

Control

Management

Cost and Control System

(MCCS)

Understanding

Control

Operating

Cycle

Cost

Account Codes

Budgets

40.1

Cost

Management:

It

is widely used in business

today and is the process

whereby companies use cost

accounting to

report

or control various costs of

doing business. Cost

Management generally

describes

approach

and activities of managers in short range

and long range planning and

cost decisions

that

incorporate value for

customer and lower costs of

product and services.

Manager

make decisions on amount and kind of material

used, changes of plant

processes,

changes

in product designs and information

from accounting system helps

managers make such

decisions,

but information and accounting

system not "cost management"

project cost

management

broad focus includes continuous

control of costs. Planning and

cost is usually

linked

with revenue and profit

planning.

In

the context of

project:

Cost

management involves overall

planning, co-ordination, and control

and reporting of all

cost-related

aspects from "project

initiation" to "operation and

maintenance".

Process

of identifying all costs

associated with investment,

making informed choices

about

options

that will deliver best

"value for money" and

managing those costs

throughout life of

project.

Techniques (value management)

help to improve value and

reduce costs.

40.2

Cost

Control:

Cost

control is equally important to

all companies, regardless of

size. Small companies

generally

have tighter monetary controls,

mainly because of the risk

with the failure of as

little

as

one project, but with less

sophisticated control techniques. Large

companies may have the

luxury

to spread project losses

over several projects, whereas the small

company may have few

projects.

Cost

control is not only

"monitoring" of costs and recording

perhaps massive quantities of

data,

but

also analyzing of the data in

order to take corrective

action before it is too

late. Cost control

should

be performed by all personnel who

incur costs, not merely the

project office. Cost

control

implies good cost

management, which must

include:

·

Cost

estimating

·

Cost

accounting

·

Project

cash flow

·

Company

cash flow

·

Direct

labor costing

·

Overhead

rate costing

·

Others,

such as incentives, penalties, and

profit-sharing

308

Project

Management MGMT627

VU

40.3

Management

Cost and Control System

(MCCS):

Cost

control is actually a subsystem of the

Management

Cost and Control System

(MCCS)

rather

than a complete system per se.

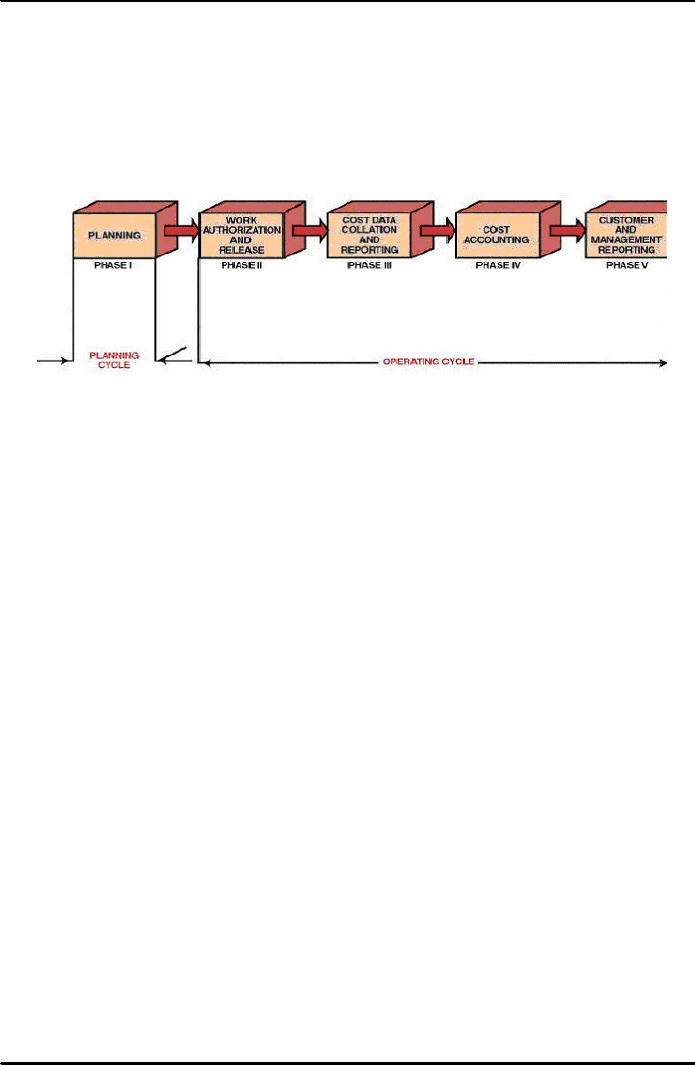

This is shown in Figure

40.1,

where

the Management Cost

and

Control System (MCCS) is

represented as a two cycle

process: a planning cycle

and an

operating

cycle. The operating cycle

is what is commonly referred to as the

cost control system.

Failure

of a cost control system to accurately

describe the true status of a

project does not

necessarily

imply that the cost control

system is at fault. Any cost

control system is only

as

good

as the original plan against which

performance will be measured. It is more common

for

the

plan to be at fault than the

control system.

Figure

40.1: Phases

of a Management Cost and

Control System

Therefore,

the designing of a company's planning

system must take into

account the cost

control

system

as well. For

this reason, it is common for the

planning cycle to be referred to

as

planning

and control, whereas the

operating cycle is referred to as

cost and control.

Note

that the planning and

control system selected must

be able to satisfy management's

needs

and

requirements in order that they

can accurately project the status

toward objective

completion.

The purpose of any

management cost and control

system is to establish policies,

procedures,

and techniques that can be used in the

day-to-day management and control

of

projects

and programs. The planning and control

system must, therefore,

provide information

that:

·

Gives

a picture of true work

progress

·

Will

relate cost and schedule

performance

·

Identifies

potential problems with respect to

their sources.

·

Provides

information to project managers

with a practical level of

summarization

·

Demonstrates

that the milestones are valid,

timely, and auditable

The

planning and control system, in

addition to being a tool by

which objectives can be

defined

that

is hierarchy

of objectives and

organization

accountability, exists as a

tool to develop

planning,

measure progress, and control

change. As a tool for

planning, the system must be

able

to:

·

Plan

and schedule work

·

Identify

those indicators that will

be used for

measurement

·

Establish

direct labor budgets

·

Establish

overhead budgets

·

Identify

management reserve

The

project budget that is the

final result of the planning

cycle of the MCCS must

be

reasonable,

attainable, and based on contractually

negotiated costs and the statement of

work.

The

basis for the budget is

historical cost, best

estimates, or industrial engineering

standards.

309

Project

Management MGMT627

VU

The

budget must identify planned

manpower requirements, contract-allocated funds,

and

management

reserve. Establishing budgets requires

that the planner fully understand

the

meaning

of standards.

We

should know that there are

two categories of standards. Performance

results standards are

quantitative

measurements and include such items as

quality of work, quantity of

work, cost of

work,

and time-to-complete. Process standards

are qualitative, including personnel,

functional,

and

physical factors relationships.

Standards

are advantageous in that

they provide a means for

unity, a basis for effective

control,

and

an incentive for others. The disadvantage

of standards is that performance is often

frozen,

and

employees are quite often

unable to adjust to the differences. As a

tool for measuring

progress

and controlling change, the systems

must be able to:

·

Measure

resources consumed

·

Measure

status and

accomplishments

·

Compare

measurements to projections and

standards

·

Provide

the basis for diagnosis and

re-planning

In

using the Management Cost

and Control System (MCCS),

the following

guidelines

usually

apply:

·

The

level of detail is specified by the

project manager with

approval by top

management.

·

Centralized

authority and control over

each project are the

responsibility of the project

management

division.

·

For

large projects, the project manager

may be supported by a project team

for utilization of

the

Management Cost and Control

System (MCCS).

Almost

all project planning and control

systems have identifiable design

requirements.

These

include:

·

A common

framework from which to

integrate time, cost, and

technical performance

·

Ability

to track progress of significant

parameters

·

Quick

response

·

Capability

for end-value

prediction

·

Accurate

and appropriate data for

decision making by each

level of management

·

Full

exception reporting with

problem analysis capability

·

Immediate

quantitative evaluation of alternative

solutions

Management

Cost and Control System

(MCCS) planning activities

include:

·

Contract

receipt (if

applicable)

·

Work

authorization for project

planning

·

Work

breakdown structure (WBS)

·

Subdivided

work description

·

Schedules

·

Planning

charts

·

Budgets

Management

Cost and Control System

(MCCS) planning charts are

worksheets used to create

the

budget. These charts include

planned labor in hours and material

dollars. Management

Cost

and

Control System (MCCS)

planning is accomplished in one of these

ways:

·

One

level below the lowest level

of the Work Breakdown Structure

(WBS)

·

At

the lowest management

level

·

By

cost element or cost

account

310

Project

Management MGMT627

VU

Even

with a fully developed

planning and control system,

there are numerous benefits and

costs.

The

appropriate system must consider a

cost-benefit analysis, and include such

items as:

·

Project

benefits:

o

Planning

and control techniques facilitate:

--

Derivation of output specifications

(project objectives)

--

Delineation of required activities

(work)

--

Coordination and communication between

organizational units

--

Determination of type, amount,

and timing of necessary

resources

--

Recognition of high-risk elements and

assessment of uncertainties

--

Suggestions of alternative courses of

action

--

Realization of effect of resource

level changes on schedule and

output

performance

--

Measurement and reporting of genuine

progress

--

Identification of potential

problems

--

Basis for problem solving,

decision making, and corrective

action

--

Assurance of coupling between planning

and control

·

Project

cost:

o

Planning

and control techniques

require:

--

New forms (new systems) of

information from additional

sources and

incremental

processing (managerial time, computer

expense, etc.)

--

Additional personnel or smaller span of

control to free managerial

time for

planning

and control tasks (increased

overhead)

--

Training in use of techniques (time

and materials)

A

well-disciplined Management Cost and

Control System (MCCS) will

produce the

following

results:

·

Policies

and procedures that will

minimize the ability to distort

reporting

·

Strong

management emphasis on meeting

commitments

·

Weekly

team meetings with a formalized

agenda, action items, and minutes.

·

Top-management

periodic review of the technical

and financial status

·

Simplified

internal audit for checking

compliance with

procedures

Furthermore,

for Management Cost and

Control System (MCCS) to be

effective, both the

scheduling

and budgeting systems must be

disciplines and formal in order to

prevent

inadvertent

or arbitrary budget or schedule

changes. This does not

mean

that the baseline

budget

and

schedule, once established, is static or

inflexible. Rather, it means

that changes must be

controlled

and result only from

deliberate management actions.

Disciplined

use of Management Cost and

Control System (MCCS) is designed to

put pressure

on

the project manager to perform

exceptionally good project

planning so that changes

will be

minimized.

As an example, government subcontractors

may not:

·

Make

retroactive changes to budgets or

costs for work that

has been completed.

·

Re-budget

work-in-progress activities

·

Transfer

work or budget independently of

each other

·

Reopen

closed work packages

In

some industries, the Management

Cost and Control System

(MCCS) must be used on

all

contracts

of $2 million or more, including firm

fixed-price efforts. The

fundamental test of

whether

to use the MCCS is to determine

whether the contracts have established

end-item

deliverables,

either hardware or computer software,

that must be accomplished

through

measurable

efforts.

311

Project

Management MGMT627

VU

Currently,

two new programs are

being used by the government and

industry in conjunction

with

the Management Cost and Control

System (MCCS) as an attempt to improve

effectiveness

in

cost control. The zero-base

budgeting program was established to

provide better

estimating

techniques

for the verification portion of

control. The design-to-cost program

assists the

decision-making

part of the control process by

identifying a decision-making framework

from

which

re-planning can take

place.

40.4

Understanding

Control:

Effective

management of a program during the

operating cycle requires that a

well-organized

cost

and control system be designed,

developed, and implemented so that

immediate feedback

can

be obtained, whereby the up-to-date

usage or resources can be

compared to target

objectives

established

during the planning cycle.

The requirements for an effective

control system (for

both

cost and schedule/performance) should

include:

·

Thorough

planning of the work to be performed to

complete the project

·

Good

estimating of time, labor, and

costs

·

Clear

communication of the scope of required

tasks

·

A

disciplined budget and authorization of

expenditures

·

Timely

accounting of physical progress and

cost expenditures

·

Periodic

re-estimation of time and cost to

complete remaining work

·

Frequent,

periodic comparison of actual progress and

expenditures to schedules and

budgets,

both at the time of comparison and at

project completion

It

is essential that the management

must compare the time, cost,

and performance of the

program

to the budgeted time, cost, and performance,

not independently but in an

integrated

manner.

Being within one's budget at

the proper time serves no

useful purpose if performance is

only

75 percent. Likewise, having a production

line turn out exactly

200 items, when

planned,

loses

its significance if a 50 percent cost

overrun is incurred.

All

three resource parameters (time,

cost, and performance) must be analyzed

as a group, or else

we

might ''win the battle but

lose the war." The use of

the expression "management cost and

control

system" is vague in that the implication is

made that only costs

are controlled. This

is

not

true-- an effective control

system monitors schedule and

performance as well as costs by

setting

budgets, measuring expenditures against budgets and

identifying variances, assuring

that

the

expenditures are proper, and

taking corrective action

when required.

Previously,

we defined the Work Breakdown Structure

(WBS) as the element that acts as

the

source

from which all costs and

controls must emanate. The

Work Breakdown Structure

(WBS)

is

the total project broken

down into successively lower

levels until the desired control

levels

are

established. The Work Breakdown Structure

(WBS) therefore serves as the

tool from which

performance

can be subdivided into

objectives and sub-objectives. As work

progresses, the

WBS

provides the framework on which

costs, time, and schedule/performance can

be compared

against

the budget for each level of

the WBS.

The

first purpose of control

therefore becomes a verification

process accomplished by the

comparison

of actual performance to date with the

predetermined plans and standards set

forth

in

the planning phase. The comparison

serves to verify

that:

·

The

objectives have been successfully translated

into performance standards.

·

The

performance standards are, in fact, a

reliable representation of program

activities and

events.

·

Meaningful

budgets have been established such

that actual versus planned

comparisons can

be

made.

312

Project

Management MGMT627

VU

In

other words, the comparison verifies that

the correct standards were selected, and

that they

are

properly used. The second

purpose of control is that of

decision making. Three

useful

reports

are required by management in

order to make effective and

timely decisions:

·

The

project plan, schedule, and

budget prepared during the planning

phase.

·

A

detailed comparison between resources expended to

data and those predetermined.

This

includes

an estimate of the work remaining and the

impact on activity

completion.

·

A

projection of resources to be expended

through program

completion.

Afterwards,

these reports are then

supplied to both the managers

and the doers. Three

useful

results

arise through the use of

these three reports, generated during a

thorough decision-making

stage

of control:

·

Feedback

to management, the planners, and the

doers.

·

Identification

of any major deviations from

the current program plan,

schedule, or budget.

·

The

opportunity to initiate contingency

planning early enough that

cost, performance, and

time

requirements can undergo corrected action

without loss of

resources.

·

These

reports, if properly prepared, provide

management with the

opportunity to minimize

downstream

changes by making proper corrections

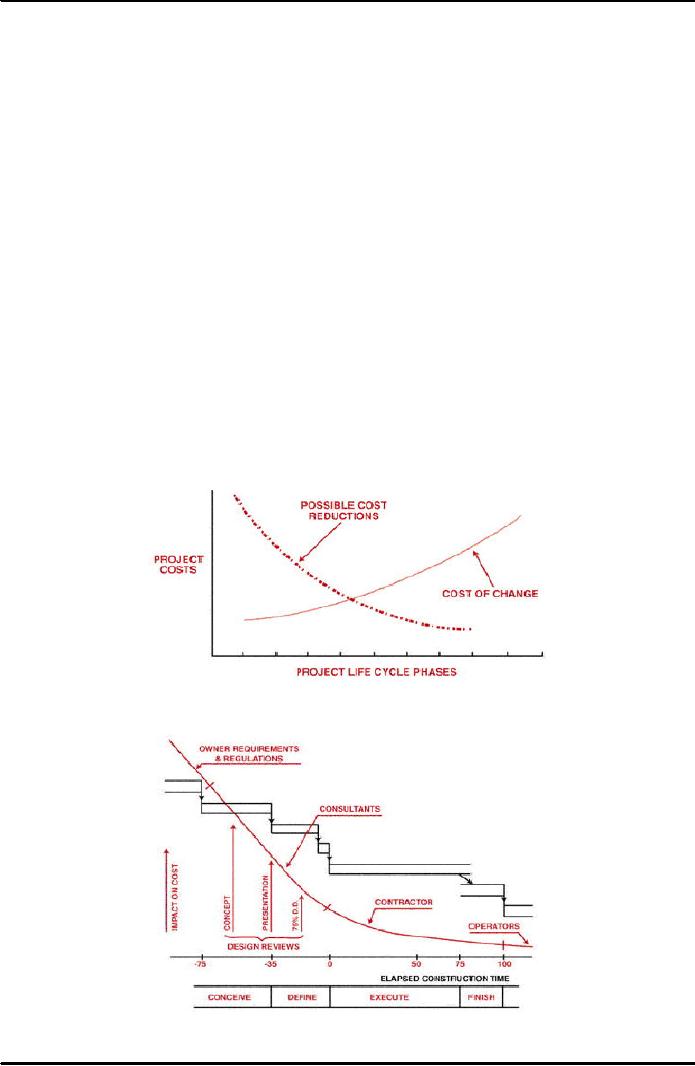

here and now. As shown in Figures

40.2

and

40.3, possible cost reductions are

usually available more readily in the

early project

phases,

but are reduced as we go

further into the project

life-cycle phases. Downstream the

cost

for changes could easily

exceed the original cost of the

project. This is an example

of

the

"iceberg" syndrome, where problems become

evident too late in the

project to be solved

easily,

resulting in a very high

cost to correct them.

Figure

40.2: Cost

Reduction Analysis

Figure

40.3: Ability to Influence

Cost

313

Project

Management MGMT627

VU

40.5

Operating

Cycle:

The

Management Cost and Control

System (MCCS) takes on paramount

importance during the

operating

cycle of the project. The

operating cycle is composed of

four phases:

·

Work

authorization and release (phase

II)

·

Cost

data collection and reporting

(phase III)

·

Cost

analysis (phase IV)

·

Reporting:

customer and management (phase

V)

These

four phases, when combined

with the planning cycle

(phase

I), constitute

a closed system

network

that forms the basis for the

management cost and control

system.

Phase

II is

considered as work release. After

planning is completed and a contract is

received,

work

is authorized via a work

description document. The work

description, or project

work

authorization

form, is a contract that contains the

narrative description, organization,

and time

frame

for each

Work

Breakdown Structure (WBS) level.

This multipurpose form is

used to

release

the contract, authorize planning, record

detail description of the work

outlined in the

Work

Breakdown Structure (WBS), and release

work to the functional

departments.

Note

that the contract services may

require a work description

form to release the contract.

The

contractual

work description form sets

forth general contractual requirements and

authorizes

program

management to proceed.

Program

management may then issue a

subdivided work description

form to the functional

units

so

that work can begin.

The subdivided work

description may also be

issued through the

combined

efforts of the project team, and

may be revised or amended

when either the scope

of

time

frame changes. The

subdivided work description

generally is not used for

efforts longer

than

ninety days and must be

"tracked" as if a project in itself.

This subdivided work

description

form

sets forth contractual requirements and

planning guidelines for the

applicable performing

organizations.

Also,

the subdivided work description

package established during the proposal

and updated

after

negotiations by the program team is

incrementally released by program

management to the

work

control centers in manufacturing

engineering, publications, and program

management as

the

authority for release of

work orders to the performing

organizations. The subdivided

work

description

specifies how contractual requirements

are to be accomplished, the

functional

organizations

involved, and their specific

responsibilities, and authorizes the expenditure

of

resources

within a particular time

frame.

The

work control center assigns

a work order number to the subdivided

work description

form,

if

no additional instructions are

required, and releases the document to

the performing

organizations.

If additional instructions are

required, the work control

center can prepare a more

detailed

work release document (shop traveler,

tool order, work order

release), assign the

applicable

work order number, and

release it to the performing

organization.

In

addition to this, a work

order number is required for

all in-house direct and indirect

charging.

The

work order number also

serves as a cross-reference number for

automatic assignment of the

indentured

work breakdown structure number to labor

and material data records in

the

computer.

In

case of small companies, they can

avoid this additional

paperwork cost by going

directly

from an awarded contract to a single

work order, which may be

the only work

order

needed for the entire

contract.

314

Project

Management MGMT627

VU

40.6

Cost

Account Codes:

It

must be noted that since

project managers control

resources through the line

managers rather

than

directly, project managers end up

controlling direct labor

costs by opening and

closing

work

orders. Work orders define the

charge numbers for each

cost account. By definition, a

cost

account

is an identified level at a natural

intersection point of the work

breakdown structure and

the

Organizational

Breakdown Structure (OBS)

at

which functional responsibility

for the work

is

assigned, and actual direct

labor, material, and other

direct costs are compared

with actual

work

performed for management

control purposes.

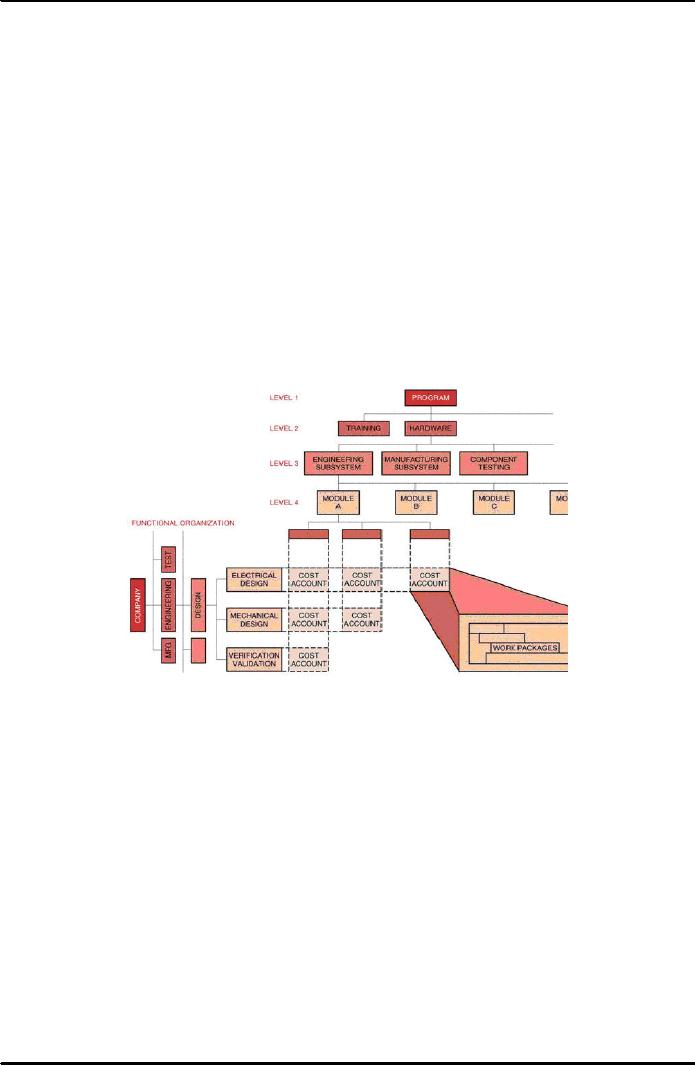

Cost

accounts are the focal point

of the Management Cost and Control

System (MCCS) and

may

comprise several work packages, as shown in

Figure 40.4. Work packages

are detailed

short

span job or material items

identified for the accomplishment of

required work. To

illustrate

this, consider the cost account

code breakdown shown in Figure

40.5 and the work

authorization

form shown in Figure 40.6.

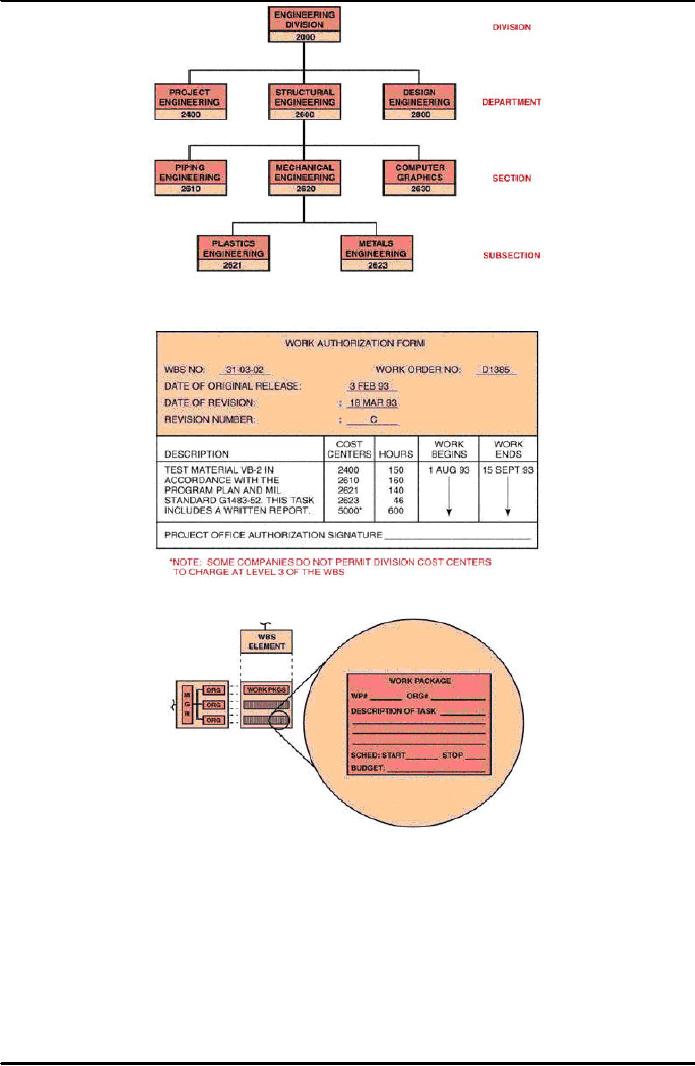

The work authorization form

specifically identifies the

cost

centers that are "open"

for this charge number, the

man-hours available for each

cost

center,

and the operational time period

for the charge number.

Because the exact dates of

operation

are completely defined, the

charge number can be assigned

perhaps as much as a

year

in

advance of the work-begin date. This

can be shown pictorially, as in Figure

40.7.

Figure

40.4: Cost

Account Intersection

If

the man-hours are assigned to cost

center 2400, then any

24xx cost center can

use this charge

number.

If the work authorization

form specifies cost center

2610, then any 261x

cost center

can

use the charge

number.

However,

if cost center 2623 is

specified, then no lower

cost accounts exist, and

this is the only

cost

center that can use

this work order charge

number. In other words, if a charge

number is

opened

up at the department level, then the department

manager has the right to

subdivide the

assigned

man-hours among the various sections and

subsections.

Company

policy usually identifies the permissible

cost center levels that

can be assigned in the

work

authorization form. These

permissible levels are

related to the work

breakdown structure

level.

For example, cost center

5000 (i.e., divisional) can

be assigned at the project level of

the

work

breakdown structure, but only department,

sectional, or sub-sectional cost accounts

can be

assigned

at the task level of the work

breakdown structure.

315

Project

Management MGMT627

VU

Figure

40.5: Cost

Account Code Breakdown

Figure

40.6: Work

Authorization Form

Figure

40.7: Planning

and Budgeting Describe, Plan, and

Schedule the Work

If

a cost center needs

additional time or additional man-hours,

then a cost account change

notice

form

must be initiated, usually by the

requesting cost center, and approved by the

project office.

The

following Figure 40.8 shows

a typical cost account

change notice form.

316

Project

Management MGMT627

VU

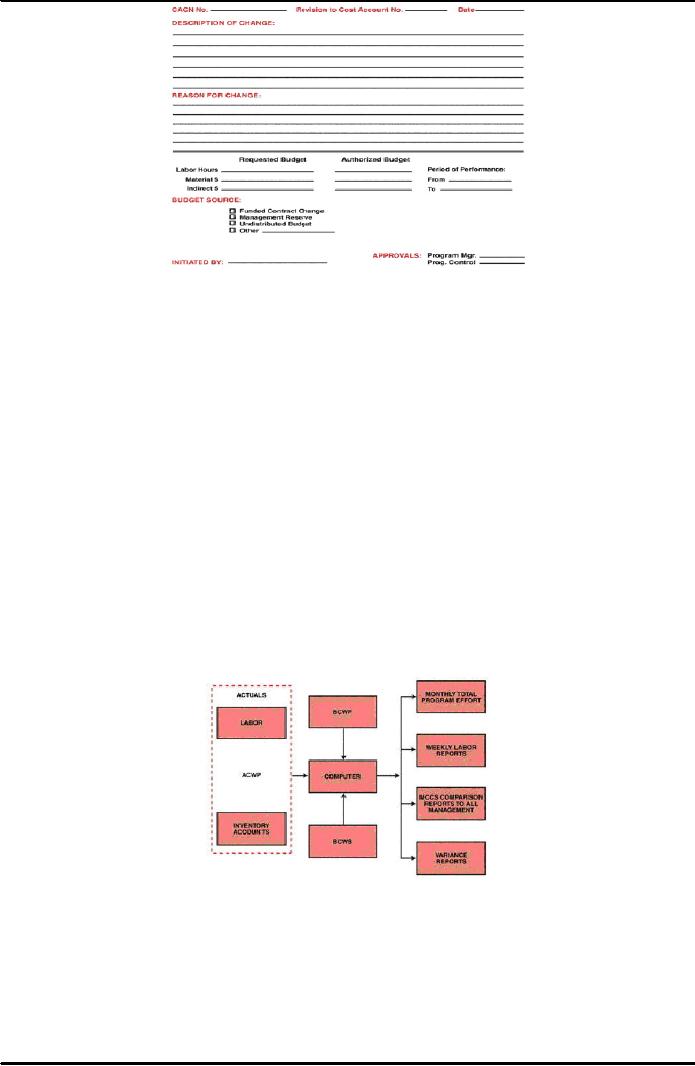

Figure

40.8: Cost

Account Change Notice

(CACN)

Almost

all large companies have computerized

cost control and reporting

systems. Small

companies

have manual or partially computerized systems.

The major difficulty in

using the

cost

account code breakdown and the

work authorization form

(shown in Figures 40.5 and

40.6)

is

related to whether the employees fill

out time cards, and

frequency with which the

time cards

are

filled out.

Project-driven

organizations fill out time

cards at least once a week,

and the cards are

inputted

to

a computerized system. Nonproject-driven

organizations fill out time

cards on a monthly

basis,

with computerization depending on the

size of the company.

Cost

data collection and reporting

constitute the second phase of the

operating cycle of the

Management

Cost and Control System

(MCCS). Actual

cost for work performed

(ACWP) and

the

budgeted

cost for work performed

(BCWP) for

each contract or in-house project

are

accumulated

in detailed cost accounts by

cost center and cost element, and

reported in

accordance

with the flow charts shown in

Figure 40.9. These detailed

elements, for both

actual

costs

incurred and the budgeted cost for

work performed, are usually

printed out monthly for

all

levels

of the work breakdown structure. In

addition, weekly supplemental direct

labor reports

can

be printed showing the actual labor

charge incurred, and can be

compared to the predicted

efforts.

Figure

40.9: Cost

Data Collection and Reporting Flow

Chart

The

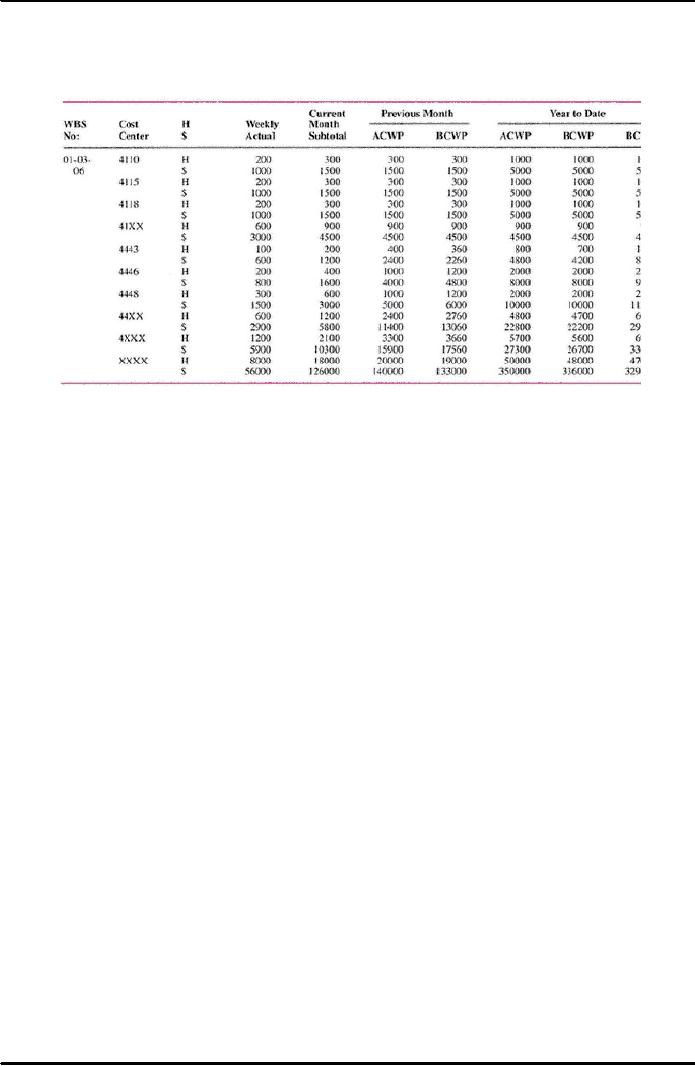

following Table 40.1 shows a

typical weekly labor report.

The first column identifies

the

Work

Breakdown Structure (WBS) number. If more

than one work order were

assigned to this

Work

Breakdown Structure (WBS) element, then

the work order number would

appear under

the

WBS number. This procedure

would be repeated for all

work orders under the same

WBS

number.

The second column contains the

cost centers charging to

this WBS element (and

possibly

work order numbers). Cost Center

41xx represents department 41 and is a

rollup of

Cost

Centers 4110, 4115, and

4118. Cost Center 4xxx

represents the entire division

and is a

317

Project

Management MGMT627

VU

rollup

of all 4000-level departments.

Cost Center xxxx represents the

total for all

divisions

charging

to this Work Breakdown Structure

(WBS) element. The weekly

labor reports must

list

all

cost centers authorized to

charge to this WBS element,

whether or not they have

incurred

any

costs over the last reporting

period.

Table

40.1: Weekly

Labor Report

Note

that most weekly labor

reports provide current month subtotals

and previous month

totals.

Although

these also appear on the

detailed monthly report,

they are included in the

weekly

report

for a quick and dirty comparison.

Year-to-date totals are

usually not on the weekly

report

unless

the users request them for an

immediate comparison to the estimate

at completion (EAC)

and

the work order

release.

Weekly

labor output is a vital tool

for members of the program

office in that these reports

can

indicate

trends in cost and performance in

sufficient time for

contingency plans to be

established

and implemented. If these reports are

not available, then cost and

labor overruns

would

not be apparent until the following

month when the detailed

monthly labor, cost,

and

materials

output was obtained. In

Table 40.1, Cost Center 4110

has spent its entire

budget. The

work

appears to be completed on schedule. The

responsible program office team

may wish to

eliminate

this cost center's authority

to continue charging to this

Work Breakdown Structure

(WBS)

element by issuing a new SWD or

work order canceling this

department's efforts.

Cost

Center

4115 appears to be only

halfway through.

If

time is becoming short, then

Cost Center 4115 must add

resources in order to

meet

requirements.

Cost Center 4443 appears to be

heading for an overrun. This

could also indicate a

management

reserve. In this case the responsible

program team member feels

that the work can

be

accomplished in fewer hours.

Work

order releases are used to

authorize certain cost

centers to begin charging

their time to a

specific

cost reporting element. Work

orders specify hours, not

dollars. The hours indicate

the

''targets"

that the program office

would like to have the department shoot

for. If the program

office

wished to be more specific and "compel"

the departments to live within

these hours, then

the

budgeted

cost for work scheduled

(BCWS) should

be changed to reflect the reduced

hours.

Four

categories of cost data are

normally accumulated:

·

Labor

·

Material

·

Other

direct charges

·

Overhead

318

Project

Management MGMT627

VU

We

know that the project

managers can maintain

reasonable control over

labor, material, and

other

direct charges.

On

the other hand, overhead costs are

calculated yearly or monthly and applied

retroactively to

all

applicable programs. Management reserves

are often used to counterbalance the

effects of

adverse

changes in overhead rates.

40.7

Budgets:

The

project budget, which is the

final result of the planning

cycle of the Management Cost

and

Control

System (MCCS), must be

reasonable,

attainable, and

based on:

·

Contractually

negotiated costs, and

·

The

statement of work

The

basis for the budget

is:

·

Historical

cost,

·

Best

estimates, or

·

Industrial

engineering standards

The

budget must identify:

·

Planned

manpower requirements,

·

Contract

allocated funds, and

·

Management

reserve.

All

budgets must be traceable through the

budget "log," which

includes:

·

Distributed

budget

·

Management

reserve

·

Undistributed

budget

·

Contract

changes

It

is important to note that the

management reserve is the dollar amount

established by the

project

office to budget for all

categories of unforeseen problems and contingencies

resulting in

out-of-scope

work to the performers. Management

reserve should be used for

tasks or dollars,

such

as rate changes, and not to cover up bad

planning estimates or budget

overruns. When a

significant

change occurs in the rate structure, the

total performance budget should be

adjusted.

In

addition to the "normal" performance

budget and the management reserve

budget, there also

exists

the following:

·

Undistributed

budget,

which is that budget

associated with contract changes where

time

constraints

prevent the necessary planning to

incorporate the change into the

performance

budget.

(This effort may be

time-constrained.)

·

Unallocated

budget,

which represents a logical

grouping of contract tasks

that have

not

yet been identified and/or

authorized.

Variance:

A

variance is defined as any

schedule, technical performance, or cost

deviation from a

specific

plan.

Variances are used by all

levels of management to verify the

budgeting system and the

scheduling

system. The budgeting and

scheduling system variance

must be compared

together

because:

·

The

cost variance compares

deviations only from the

budget and does not provide

a

measure

of comparison between work scheduled and

work accomplished.

319

Project

Management MGMT627

VU

·

The

scheduling variance provides a comparison

between planned and actual performance

but

does not include

costs.

There

are two primary methods of

measurement:

·

Measurable

efforts: Discrete

increments of work with a definable

schedule for

accomplishment,

whose completion produces

tangible results.

·

Level

of effort: Work

that does not lend

itself to subdivision into discrete

scheduled

increments

of work, such as project support and

project control.

Variances

are used on both types of

measurement:

In

order to calculate variances we must

define the three basic variances for

budgeting and actual

costs

for work scheduled and

performed. Archibald defines these

variables:

·

Budgeted

cost for work scheduled

(BCWS) is the budgeted amount of cost for

work

scheduled

to be accomplished plus the amount or level of

effort or apportioned

effort

scheduled

to be accomplished in a given time

period.

·

Budget

cost for work performed

(BCWP) is the budgeted amount of cost for

completed

work,

plus budgeted for level of

effort or apportioned effort

activity completed within a

given

time period. This is

sometimes referred to as "earned

value."

·

Actual

cost for work performed

(ACWP) is the amount reported as actually

expended in

completing

the work accomplished within a given

time period.

320

Table of Contents:

- INTRODUCTION TO PROJECT MANAGEMENT:Broad Contents, Functions of Management

- CONCEPTS, DEFINITIONS AND NATURE OF PROJECTS:Why Projects are initiated?, Project Participants

- CONCEPTS OF PROJECT MANAGEMENT:THE PROJECT MANAGEMENT SYSTEM, Managerial Skills

- PROJECT MANAGEMENT METHODOLOGIES AND ORGANIZATIONAL STRUCTURES:Systems, Programs, and Projects

- PROJECT LIFE CYCLES:Conceptual Phase, Implementation Phase, Engineering Project

- THE PROJECT MANAGER:Team Building Skills, Conflict Resolution Skills, Organizing

- THE PROJECT MANAGER (CONTD.):Project Champions, Project Authority Breakdown

- PROJECT CONCEPTION AND PROJECT FEASIBILITY:Feasibility Analysis

- PROJECT FEASIBILITY (CONTD.):Scope of Feasibility Analysis, Project Impacts

- PROJECT FEASIBILITY (CONTD.):Operations and Production, Sales and Marketing

- PROJECT SELECTION:Modeling, The Operating Necessity, The Competitive Necessity

- PROJECT SELECTION (CONTD.):Payback Period, Internal Rate of Return (IRR)

- PROJECT PROPOSAL:Preparation for Future Proposal, Proposal Effort

- PROJECT PROPOSAL (CONTD.):Background on the Opportunity, Costs, Resources Required

- PROJECT PLANNING:Planning of Execution, Operations, Installation and Use

- PROJECT PLANNING (CONTD.):Outside Clients, Quality Control Planning

- PROJECT PLANNING (CONTD.):Elements of a Project Plan, Potential Problems

- PROJECT PLANNING (CONTD.):Sorting Out Project, Project Mission, Categories of Planning

- PROJECT PLANNING (CONTD.):Identifying Strategic Project Variables, Competitive Resources

- PROJECT PLANNING (CONTD.):Responsibilities of Key Players, Line manager will define

- PROJECT PLANNING (CONTD.):The Statement of Work (Sow)

- WORK BREAKDOWN STRUCTURE:Characteristics of Work Package

- WORK BREAKDOWN STRUCTURE:Why Do Plans Fail?

- SCHEDULES AND CHARTS:Master Production Scheduling, Program Plan

- TOTAL PROJECT PLANNING:Management Control, Project Fast-Tracking

- PROJECT SCOPE MANAGEMENT:Why is Scope Important?, Scope Management Plan

- PROJECT SCOPE MANAGEMENT:Project Scope Definition, Scope Change Control

- NETWORK SCHEDULING TECHNIQUES:Historical Evolution of Networks, Dummy Activities

- NETWORK SCHEDULING TECHNIQUES:Slack Time Calculation, Network Re-planning

- NETWORK SCHEDULING TECHNIQUES:Total PERT/CPM Planning, PERT/CPM Problem Areas

- PRICING AND ESTIMATION:GLOBAL PRICING STRATEGIES, TYPES OF ESTIMATES

- PRICING AND ESTIMATION (CONTD.):LABOR DISTRIBUTIONS, OVERHEAD RATES

- PRICING AND ESTIMATION (CONTD.):MATERIALS/SUPPORT COSTS, PRICING OUT THE WORK

- QUALITY IN PROJECT MANAGEMENT:Value-Based Perspective, Customer-Driven Quality

- QUALITY IN PROJECT MANAGEMENT (CONTD.):Total Quality Management

- PRINCIPLES OF TOTAL QUALITY:EMPOWERMENT, COST OF QUALITY

- CUSTOMER FOCUSED PROJECT MANAGEMENT:Threshold Attributes

- QUALITY IMPROVEMENT TOOLS:Data Tables, Identify the problem, Random method

- PROJECT EFFECTIVENESS THROUGH ENHANCED PRODUCTIVITY:Messages of Productivity, Productivity Improvement

- COST MANAGEMENT AND CONTROL IN PROJECTS:Project benefits, Understanding Control

- COST MANAGEMENT AND CONTROL IN PROJECTS:Variance, Depreciation

- PROJECT MANAGEMENT THROUGH LEADERSHIP:The Tasks of Leadership, The Job of a Leader

- COMMUNICATION IN THE PROJECT MANAGEMENT:Cost of Correspondence, CHANNEL

- PROJECT RISK MANAGEMENT:Components of Risk, Categories of Risk, Risk Planning

- PROJECT PROCUREMENT, CONTRACT MANAGEMENT, AND ETHICS IN PROJECT MANAGEMENT:Procurement Cycles