|

BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM |

| << BRANCH ACCOUNTING |

| STOCK AND DEBTORS SYSTEM >> |

Advance

Financial Accounting

(FIN-611)

VU

LESSON

#13

BRANCH

ACCOUNTING - STOCK AND DEBTOR

SYSTEM

Stock

and Debtors system is generally

used when the goods are

sent to the branch at

pro-forma

invoice price and the size

of the branch is large. Under

this system, the

branch

maintains a few central accounts to

exercise greater control

over the branch

stock

and other related expenses.

These accounts usually

are:

1.

Branch

Stock Account

2.

Branch

Debtors Account

3.

Branch

Expenses Account

4.

Branch

Adjustment Account

5.

Goods

Sent to Branch

Account

6.

Branch

Stock Reserve Account

Branch

Stock Account

This

account is on the pattern of a

stock account. The account

helps the Head Office

in

maintaining

an effective control over

the Branch Stock and tells

about shortage and

surplus

in the branch stock because

of the difference between

the pro-forma invoice

price

and the selling

price.

Unlike

traditional accounting practice,

branch stock a/c is always

maintained on the

selling

price or pro-forma invoice

price. Selling price is used

to record the goods

sold

by

the branch to its customer

and goods returned by the

branch customers. Rest of

the

information

(even opening and closing

balances) in branch stock a/c is

recorded at

pro-forma

invoice price.

Branch

Debtors Account

Branch

debtors' a/c is maintained in the

traditional manner to record

transactions in

between

branch and its credit

customers.

Branch

Expense Account

The

purpose of maintaining this

account is nothing but the

compile all branch

expenses

at one place. This will

include all types of expenses

i.e. cash based

expenses

and

receivables based

expenses.

Branch

Adjustment Account

Branch

adjustment a/c replaces the

branch income statement

(profit & loss a/c).

This

is

the account in which all expenses and

losses are closed along with

the margin that is

a

difference between cost and

the selling price. This

difference is split into two; one

is

termed

as "surplus" that comes from the

branch stock a/c representing

the difference

between

selling price and pro-forma

invoice price, the second is

termed as "loading"

that

represents the difference

between pro-forma invoice

price and cost. This

loading

is

calculated on opening and closing

stock balances and also on

the net of the

goods

sent

branch.

60

Advance

Financial Accounting

(FIN-611)

VU

Goods

Sent to Branch Account

This

is a supporting account, which is

maintained to show second effects of

the goods

sent

to branch and the goods

returned from branch at pro-forma

invoice price.

Although

the goods sent to and

returned form the branch

should be adjusted in

the

purchases

a/c of the head office, but as we know

that the branch stock a/c is

not

maintained

at cost price, therefore,

second effect of goods sent

to and returned from

branch

is not recorded directly into the

purchases a/c instead this

second effect is

recorded

into the goods sent to

branch a/c which after adjustment of

the loading is

finally

closed into the purchases

a/c.

Branch

Stock Reserve

Account

This

is contra to branch stock

account. In this account

opening and closing balance

of

loading

on branch stock is

maintained.

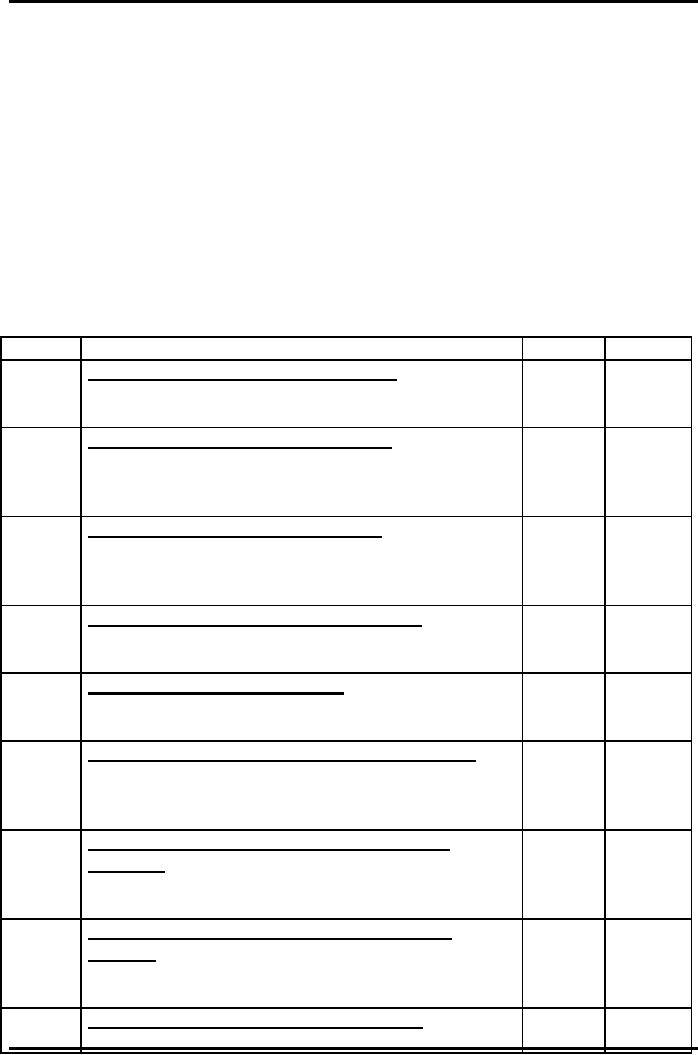

ACCOUNTING

ENTRIES IN THE BOOKS OF

HEAD

OFFICE

Sr

no.

JOURNAL

ENTRIES

Debit

Credit

For

Goods Sent to Branch (at

Invoice)

Branch

Stock Account (Dr)

xxx

(1)

Goods

Sent To Branch Account

(Cr)

xxx

For

Goods Sold At Branch On

Credit

Branch

Debtors Account (Dr)

(At

xxx

(2)

Selling

Price)

xxx

Branch

Stock Account (Cr)

For

Goods Sold At Branch For

Cash

Branch

Cash Account (Dr)

(At

xxx

(3)

Selling

Price)

xxx

Branch

Stock Account (Cr)

For

Cash Received From Branch

Debtors

Branch

Cash Account (Dr)

xxx

(4)

Branch

Debtors Account (Cr)

xxx

For

Goods Returned by

Branch

Branch

Stock Account (Dr)

xxx

(5)

Branch

Debtors Account (Cr)

xxx

For

Goods Returned by Branch To

Head Office

Goods

Sent To Branch Account

(Dr)

xxx

(6)

(At

Invoice)

xxx

Branch

Stock Account (Cr)

For

Cash Sent By Head Office to

Branch For

Expenses

xxx

(7)

Branch

Expenses Account (Dr)

xxx

Cash

Account (Cr)

For

Bad Debts/ discount Allowed

To Branch

Debtors

xxx

(8)

Branch

Debtors Account (Dr)

xxx

Branch

Debtors Account (Cr)

For

Shortage/ Shrinkage in Branch

Stock

(9)

Branch

Adjustment Account

(Dr)

xxx

61

Advance

Financial Accounting

(FIN-611)

VU

Branch

Stock Account

xxx

(Cr)

For

Surplus In Branch

Stock

Branch

Stock Account (Dr)

xxx

(10)

Branch

Adjustment Account

(Cr)

xxx

For

Closing Branch Expenses Account

Into Branch

Adjustment

Account

xxx

(11)

Branch

Adjustment Account

(Dr)

xxx

Branch

Expenses Account (Cr)

For

Transfer of Opening Stock

Reserve (Loading)

Into

The Branch Adjustment

Account

Branch

Stock Reserve Account (Dr)

(with

loading

xxx

(12)

of

opening

Branch

Adjustment Account

(Cr)

xxx

For

Creating Stock Reserve on

Closing Balance of

Stock

(Loading on Closing

Stock)

(13)

Branch

Adjustment Account

(Dr)

xxx

Branch

Stock Reserve (Cr)

xxx

For

Loading on Net Amount of

Goods Sent to

Branch

xxx

(14)

Goods

Sent to Branch Account

(Dr)

xxx

Branch

Adjustment Account

(Cr)

For

Closing Goods Sent To Branch

Account Into

Purchase

Account

(15)

Goods

Sent To Branch Account

(Dr)

xxx

Purchases

Account (Cr)

xxx

For

Closing the Branch

Adjustment Account

Into

Profit

& Loss Account

Branch

Adjustment Account (Dr)

(with the

(16)

xxx

amount

of profit on branch)

Profit

& Loss Account

(Cr)

xxx

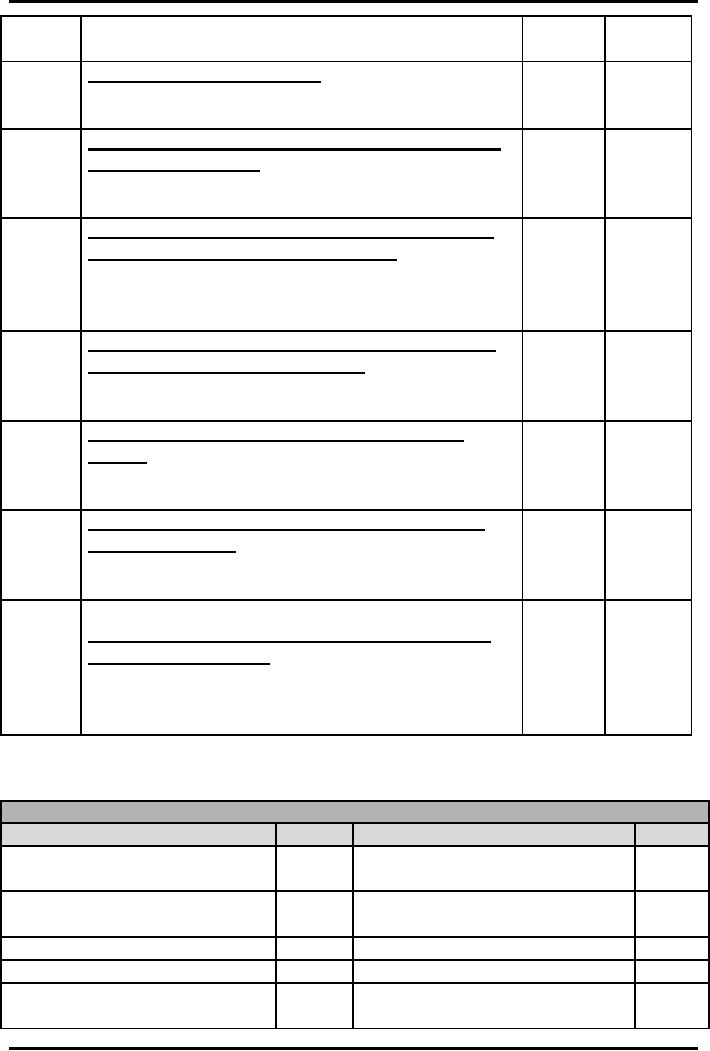

LEDGER

ACCOUNTS

IN THE MAIN

LEDGER OF HEAD OFFICE

BRANCH

STOCK ACCOUNT

Particulars

Debit

Particulars

Credit

Balance

Brought Forward (At

******

Branch

Debtors (Credit

Sales)

Jef

(2)

Invoice)

(Selling

Price)

Goods

Sent to Branch (At

Jef (1)

Branch

Cash (Cash

Sales)(Selling

Jef(3)

Invoice)

Price)

Branch

Debtors (Sales

Return)

Jef

(5)

Goods

Sent to Branch

(Return)

Jef(6)

Branch

Adjustment (Surplus)

Jef

(10) Branch Adjustment

(Shortage)

Jef(9)

Balance

Carried Forward (At

******

Invoice)

62

Advance

Financial Accounting

(FIN-611)

VU

GOODS

SENT TO BRANCH ACCOUNT

Particulars

Debit

Particulars

Credit

Branch

Stock (Credit Sales)

Jef(6)

Branch

Stock (Goods Sent) (At

Jef(1)

Invoice)

Branch

Adjustment (Loading)

Jef(14)

Purchases

(Balancing Figure)

Jef(15)

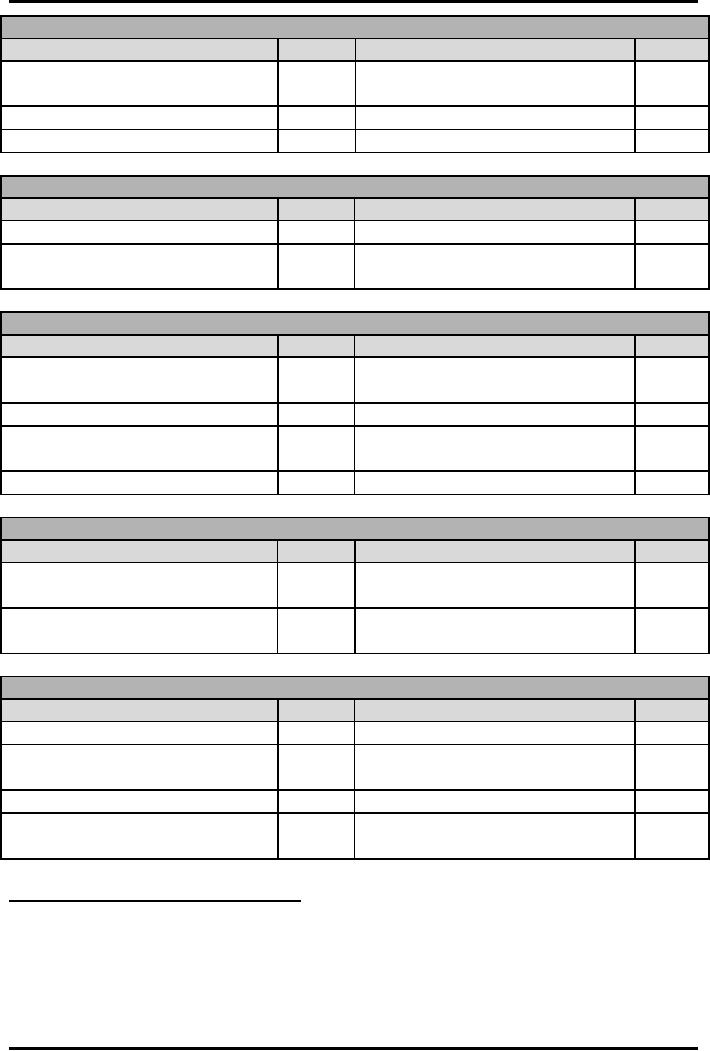

BRANCH

EXPENESE ACCOUNT

Particulars

Debit

Particulars

Credit

Cash

(Expense)

Jef(7)

Branch

Adjust (Closing)

Jef(11)

Branch

Debtors

(Discount

Jef(8)

Allowed +

Bad Debts)

BRANCH

DEBTORS ACCOUNT

Particulars

Debit

Particulars

Credit

Opening

Balance

Brought

******

Cash

Received

Jef(4)

Forward

Branch

Stock (Credit Sales)

Jef(2)

Branch

Stock (Sales Return)

Jef(5)

Branch

Expense (Bad Debts +

Jef(8)

Discount

Allowed)

Balance

Brought Forward

******

STOCK

RESERVE ACCOUNT

Particulars

Debit

Particulars

Credit

Branch

Adjustment (Transfer of

Jef(12)

Opening

Stock Reserve Brought

******

Opening

Balance)

Forward

Closing

Stock Reserve Balance

******

Branch

Adjustment (Closing

Jef(13)

c/f

Loading)

BRANCH

ADJUSTMENT ACCOUNT

Particulars

Debit

Particulars

Credit

Branch

Stock (Shortage)

Jef

(9)

Branch

Stock (Surplus)

Jef(10)

Branch

Expense (Closed)

Jef

(11)

Branch

Stock Reserve

(Opening

Jef(12)

Balance)

Branch

Stock Reserve

(Closing)

Jef

(13)

Goods

Sent to Branch

(Loading)

Jef(14)

Profit

&

Loss

Account

Jef (16)

(Balancing

Figure)

Note:

(Jef = Journal Entry

Reference)

63

Table of Contents:

- ACCOUNTING FOR INCOMPLETE RECORDS

- PRACTICING ACCOUNTING FOR INCOMPLETE RECORDS

- CONVERSION OF SINGLE ENTRY IN DOUBLE ENTRY ACCOUNTING SYSTEM

- SINGLE ENTRY CALCULATION OF MISSING INFORMATION

- SINGLE ENTRY CALCULATION OF MARKUP AND MARGIN

- ACCOUNTING SYSTEM IN NON-PROFIT ORGANIZATIONS

- NON-PROFIT ORGANIZATIONS

- PREPARATION OF FINANCIAL STATEMENTS OF NON-PROFIT ORGANIZATIONS FROM INCOMPLETE RECORDS

- DEPARTMENTAL ACCOUNTS 1

- DEPARTMENTAL ACCOUNTS 2

- BRANCH ACCOUNTING SYSTEMS

- BRANCH ACCOUNTING

- BRANCH ACCOUNTING - STOCK AND DEBTOR SYSTEM

- STOCK AND DEBTORS SYSTEM

- INDEPENDENT BRANCH

- BRANCH ACCOUNTING 1

- BRANCH ACCOUNTING 2

- ESSENTIALS OF PARTNERSHIP

- Partnership Accounts Changes in partnership firm

- COMPANY ACCOUNTS 1

- COMPANY ACCOUNTS 2

- Problems Solving

- COMPANY ACCOUNTS

- RETURNS ON FINANCIAL SOURCES

- IASBS FRAMEWORK

- ELEMENTS OF FINANCIAL STATEMENTS

- EVENTS AFTER THE BALANCE SHEET DATE

- PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 1

- ACCOUNTING POLICIES, CHANGES IN ACCOUNTING ESTIMATES AND ERRORS 2

- BORROWING COST

- EXCESS OF THE CARRYING AMOUNT OF THE QUALIFYING ASSET OVER RECOVERABLE AMOUNT

- EARNINGS PER SHARE

- Earnings per Share

- DILUTED EARNINGS PER SHARE

- GROUP ACCOUNTS

- Pre-acquisition Reserves

- GROUP ACCOUNTS: Minority Interest

- GROUP ACCOUNTS: Inter Company Trading (P to S)

- GROUP ACCOUNTS: Fair Value Adjustments

- GROUP ACCOUNTS: Pre-acquistion Profits, Dividends

- GROUP ACCOUNTS: Profit & Loss

- GROUP ACCOUNTS: Minority Interest, Inter Co.

- GROUP ACCOUNTS: Inter Co. Trading (when there is unrealized profit)

- Comprehensive Workings in Group Accounts Consolidated Balance Sheet